A lot of business owners in Dubai arrive at the same point from different directions. One has a banker asking for cleaner forecasts before discussing funding. Another receives an approach from a buyer and has no idea whether the offer is fair. A third is growing quickly, but cash is tighter each month because growth is eating working capital.

That's usually when corporate finance stops being theoretical.

The issue isn't whether the business is “doing well” in a general sense. The issue is whether the owner can make a high-stakes decision with enough structure, enough evidence, and enough negotiating power. In Dubai, that matters even more because transactions often involve cross-border shareholders, free zone or mainland considerations, lender scrutiny, and counterparties who move fast when they sense weakness.

When Your Business Reaches a Financial Crossroads

Most businesses don't seek corporate finance advice because they like advisory work. They seek it because a decision has become too important to handle casually.

A common example is an owner who planned to expand through a new facility, a new product line, or a market-entry push, only to realise the question isn't “Can we grow?” but “What's the least risky way to fund growth without damaging control, liquidity, or valuation?” Another example is a founder who gets an unsolicited acquisition approach and suddenly needs answers on value, deal structure, tax implications, diligence exposure, and timing.

The moments that usually trigger advisory work

In practice, I see a few triggers come up repeatedly:

- Capital pressure: The business needs funding, but the owner doesn't know whether debt, equity, or a hybrid structure fits the cash profile.

- Shareholder change: One partner wants to exit, a family business is preparing succession, or a new investor wants in.

- Transaction interest: A buyer, strategic investor, or private party approaches the company before the seller is prepared.

- Early signs of stress: Margins tighten, covenant conversations get uncomfortable, and forecasting starts to feel defensive rather than useful.

Practical rule: If the decision will affect ownership, lender relationships, or the company's sale value, routine accounting isn't enough.

That's one reason the market is substantial. The UAE corporate finance advisory market is estimated at USD 1.5 billion, with demand driven by foreign investment, real estate activity, and mergers and acquisitions in Dubai and Abu Dhabi, according to Ken Research's UAE corporate finance advisory market overview. The same source notes that client demand comes from corporates, financial institutions, government entities, private equity firms, family-owned businesses, and startups.

Why this matters for a Dubai investor

Dubai isn't a market where only large corporates need this support. New investors, owner-managed SMEs, venture-backed firms, and long-established family businesses all hit decision points where financial structure becomes strategic.

Before you even start those discussions, it helps to get your internal fundamentals in order. A practical starting point is this CFO's guide to firm finances, especially if your current challenge is deciding whether the problem is growth funding, operating cash flow, or balance-sheet pressure.

Corporate finance advisory in Dubai is best understood as support for those moments when one decision can improve value or lock in a bad outcome for years.

What Is Corporate Finance Advisory Really

Corporate finance advisory is easiest to understand if you separate it from the finance work most companies already know.

Your accountant records what happened. Your finance manager helps run the month. Your auditor tests whether reporting is fairly presented. A corporate finance advisor works on the decisions that change the shape of the business.

Think of the advisor as a financial architect

An architect doesn't inspect a completed building. They design how it should stand, how it should function, and how different parts need to work together. That's the better analogy for corporate finance advisory in Dubai.

The advisor's job is to help answer questions such as:

- Should the company raise debt, equity, or both?

- Is this acquisition target worth pursuing?

- What is the business likely to be worth in a real negotiation?

- How should management present earnings, debt, and working capital before a sale or fundraise?

- Is refinancing better than a recapitalisation or structured exit?

That's different from bookkeeping, VAT filing, payroll processing, or annual audit support. Those services matter, but they are not the same discipline.

Why the distinction matters in Dubai

Dubai's company base keeps widening. The UAE issued 18,958 new economic licences in the first quarter of 2024, bringing the total number of registered economic licences to 1.03 million nationwide, and the Dubai Chamber of Commerce registered 59,000 new member companies in the first half of 2024, as noted in this UAE corporate finance strategy market summary. That volume tells you something important. More businesses are reaching the stage where strategic finance questions show up much earlier.

A newly formed business may not need sell-side M&A advice on day one. But it may need help building a funding story, setting shareholder economics, or preparing a lender-ready model. An established company may have proper accounts but still be poorly prepared for investor diligence.

What advisory is not

A lot of confusion comes from firms buying the wrong service.

- It isn't compliance work: Filing returns and maintaining statutory records won't tell you how to structure a capital raise.

- It isn't generic strategy consulting: Broad business recommendations are not the same as transaction-ready financial analysis.

- It isn't just for distress: Healthy companies use advisory support before expansion, before acquisitions, and before shareholder events.

A business can be profitable and still be unprepared for capital. Investors and lenders look for clarity, not just growth.

If your model depends on subscriptions or contracted income, understanding what buyers and investors consider durable revenue can sharpen your positioning. This explainer on what is recurring revenue is useful because recurring income often changes how outsiders assess stability, forecasting quality, and deal attractiveness.

In practical terms, corporate finance advisory Dubai engagements are about preparing for scrutiny, shaping options, and improving negotiating position before the market prices your business for you.

Key Advisory Services and Their Deliverables

When owners ask what an advisor does, the wrong answer is a vague list of services. The better answer is to show what work gets done and what lands on the client's desk.

In the UAE, advisory teams handle merger and acquisition execution, private placement, alternative financing procurement, and due diligence, and that work can extend into working-capital analysis, EBITDA normalization, true-debt assessment, and forecast testing to create value-enhancing transactions, according to Deloitte Middle East's financial advisory description.

The services that matter most in live situations

Some mandates are outward-facing. They help you approach lenders, investors, or buyers. Others are inward-facing. They help management understand what the company will look like under diligence.

That distinction matters because many weak transactions fail before negotiations become serious. The business isn't ready. Revenue recognition is messy, debt-like items are hidden in the balance sheet, forecasts don't reconcile, and management can't explain working-capital swings cleanly.

Buyers rarely walk away because a business has no issues. They walk away because management can't explain the issues.

Corporate Finance Advisory Services and Typical Deliverables

| Service | Primary Goal | Key Deliverables |

|---|---|---|

| M&A advisory | Buy, sell, or merge on better terms | target or buyer list, valuation view, information pack, deal positioning, negotiation support, transaction coordination |

| Valuation advisory | Establish defensible value for a transaction or shareholder event | valuation report, assumptions schedule, sensitivity analysis, management discussion points |

| Capital raising | Secure debt, equity, or alternative financing | financial model, investor or lender materials, funding strategy, outreach list, support on term sheet discussions |

| Due diligence preparation | Reduce surprises before external review | data room checklist, quality of earnings support, EBITDA adjustments schedule, working-capital review |

| Debt and refinancing advisory | Improve liquidity structure and lender terms | lender pack, covenant review, refinancing options, cash flow scenarios, negotiation support |

| Restructuring support | Stabilise a pressured business and preserve options | short-term cash plan, stakeholder mapping, restructuring proposals, turnaround priorities |

What good deliverables look like

A real deliverable is usable in a negotiation. It isn't a slide deck full of broad observations.

For example, in a sell-side assignment, the value often comes from preparing the business for challenge. That means normalising EBITDA where owner-specific or non-recurring items distort earnings, identifying true debt that a buyer will likely treat as debt-like in a completion mechanism, and testing forecasts hard enough that management won't collapse under diligence questions.

In fundraising, a strong deliverable set should also connect to banking readiness. If you're opening or restructuring your operating setup around new financing, practical infrastructure matters too, including the banking side. This overview of a business banking account in the UAE is relevant because capital strategy often fails on execution details, not just on modelling.

What works and what doesn't

- Works: Starting preparation before outreach, especially for a sale or refinancing.

- Works: Building one data set that management, lenders, and investors can all reconcile.

- Doesn't work: Sending investors unaudited or poorly explained numbers and hoping the story carries the round.

- Doesn't work: Treating due diligence as an administrative exercise rather than a pricing exercise.

A capable advisor doesn't just “introduce capital”. They help turn a business into something financeable, defensible, and easier to transact.

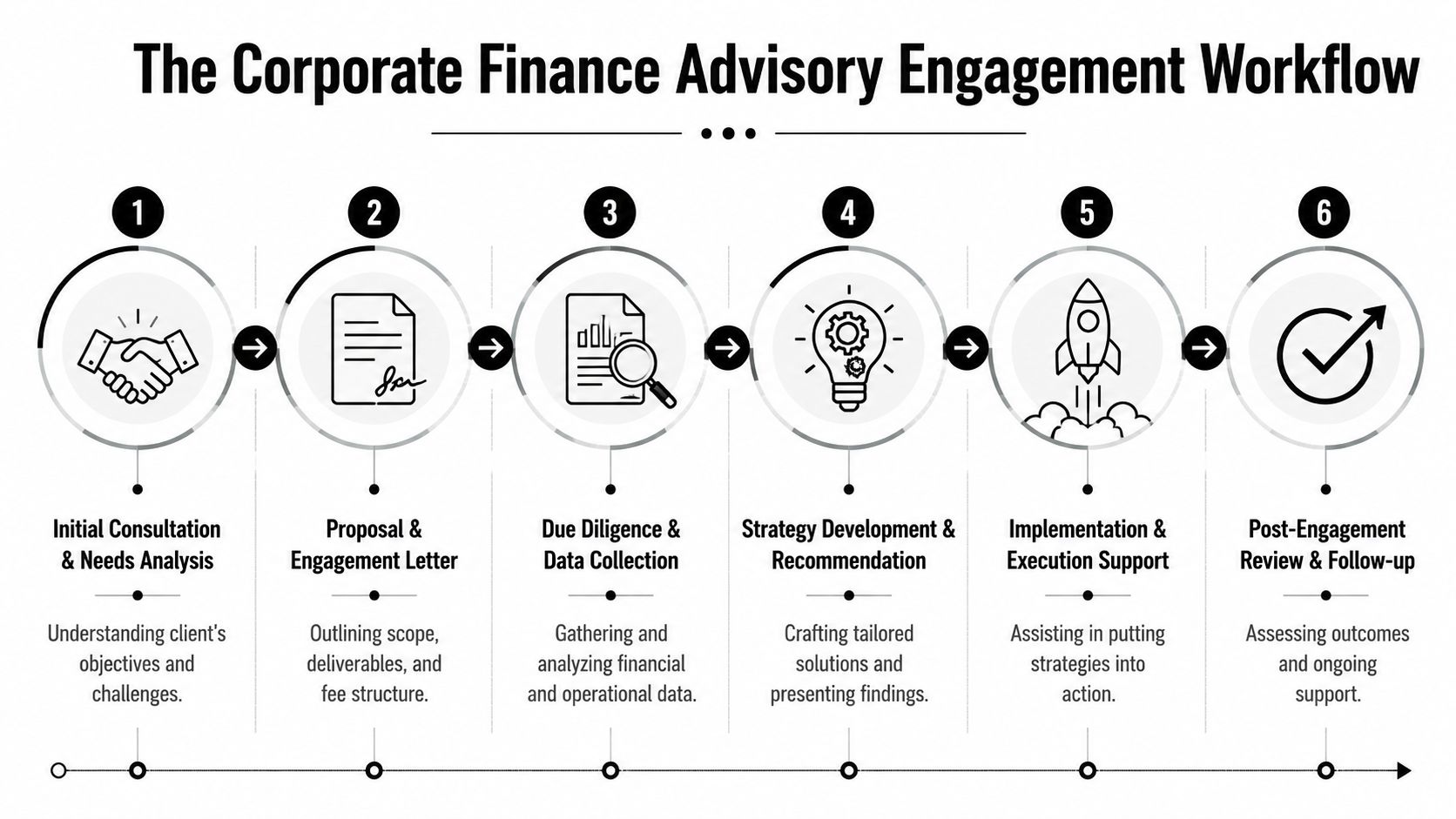

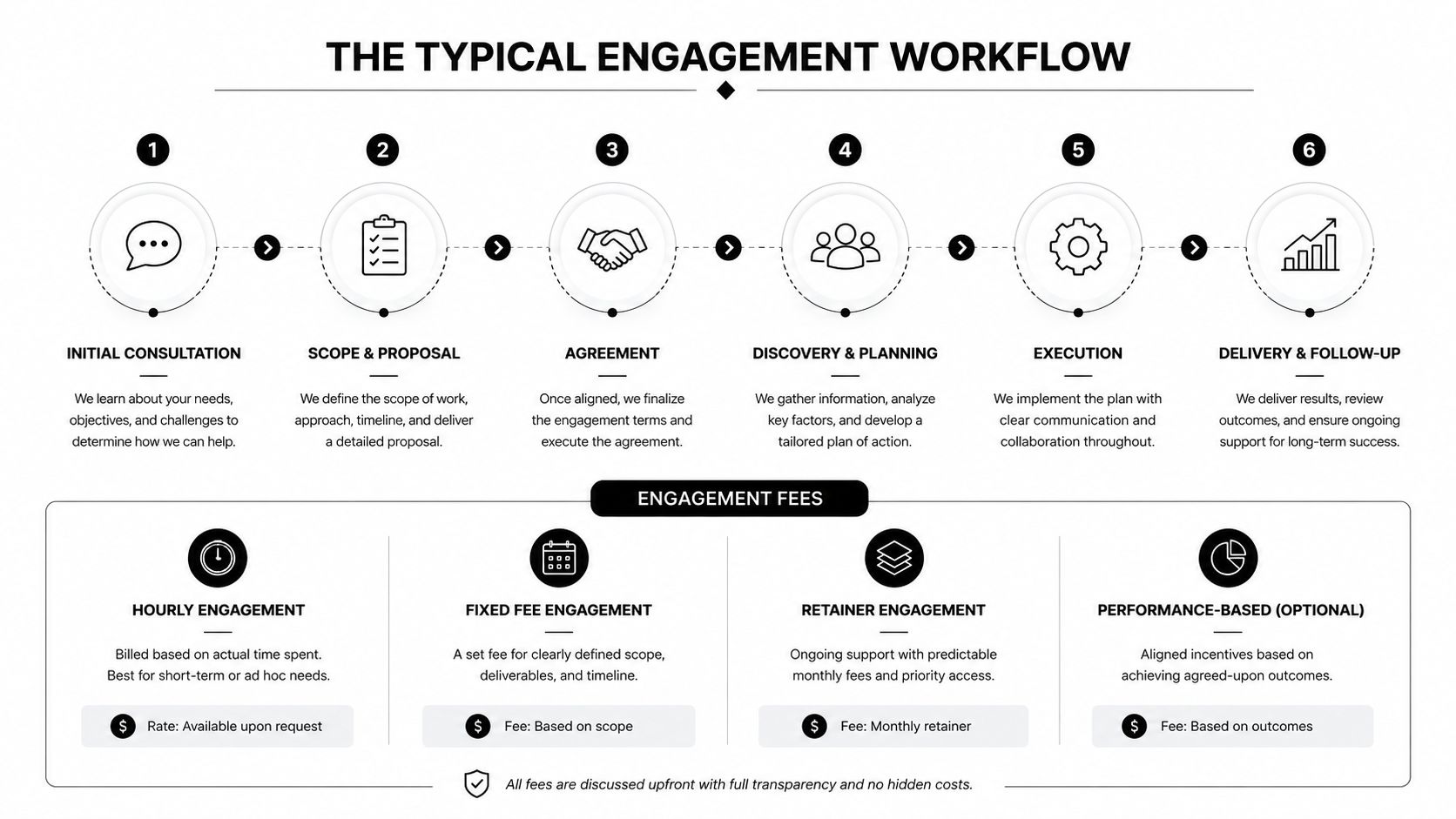

The Typical Engagement Workflow and Fees

Most owners are less worried about the theory than the process. They want to know what happens after the first call, how much management time is required, and when fees start to accrue.

A sound corporate finance advisory engagement follows a fairly disciplined pattern. The exact scope changes by mandate, but the shape is usually similar.

Phase one through phase three

The process usually begins with diagnosis, not pitching.

Initial discussion

The advisor tests the actual mandate. Sometimes the client asks for fundraising help, but the deeper issue is poor working-capital discipline or a weak lender package.Scope and engagement letter

Sensible clients should slow down and read the engagement letter carefully. It should state the mandate, exclusions, deliverables, fee basis, confidentiality terms, and whether the advisor is engaged for analysis only or also for execution.Information gathering and review

Management accounts, historic financials, debt documents, customer concentration, forecasts, shareholder arrangements, and legal structure all come under review. This stage often exposes gaps that need fixing before the mandate can move forward properly.

Phase four through close

Once the information base is stable, the work becomes more strategic and more external.

- Strategy design: The advisor defines the funding or transaction route, key messages, valuation framing, and likely friction points.

- Market engagement: This may involve approaching lenders, investors, or buyers in a controlled process.

- Negotiation support: Offers are compared, problem areas are challenged, and the client gets help with commercial trade-offs.

- Closing support: Final diligence requests, document alignment, financial clarifications, and completion mechanics are handled through to signing and close.

The best engagements feel orderly from the client side, even when the transaction itself is messy behind the scenes.

How fees are usually structured

Fee structures vary, but the logic is straightforward.

| Fee model | Where it fits | What to watch |

|---|---|---|

| Retainer | Early-stage analysis, preparation, restructuring, or ongoing support | Check what hours or workstreams are included |

| Success fee | Capital raising, M&A, or refinancing where completion is the goal | Define what counts as success and when payment triggers |

| Hybrid | Most execution mandates | Make sure the balance between retainer and success fee reflects actual work, not just optimism |

A retainer works when the mandate involves significant preparation or uncertain timing. A success fee aligns interests in execution, but clients should read the definitions carefully. If funding is raised in tranches, if a deal changes shape, or if a counterparty introduced by the client completes the transaction, the fee language matters.

Where clients make avoidable mistakes

The biggest mistakes are procedural.

- They under-resource the process: Management delays responses, and momentum disappears.

- They hide weak spots: Issues always come out later, usually at a worse moment.

- They compare advisors only on headline fee: Cheap mandates can become expensive if they fail or drag on.

- They don't assign a single internal owner: Without one decision-maker, the data flow becomes chaotic.

Good workflow discipline saves time. Beyond this, it protects value when negotiations tighten.

Navigating Dubai's Financial Regulatory Maze

Every transaction in Dubai sits inside a legal and regulatory framework, even when the commercial parties are moving informally at first. That framework affects what can be sold, who can invest, how diligence is conducted, how money moves, and which approvals may be needed.

Structure matters before the transaction starts

A mainland company, a DIFC entity, an ADGM structure, and a free zone operating company don't present the same issues. Share transfer mechanics, governing law preferences, licensing boundaries, and documentation expectations can differ in ways that change transaction design.

That's why good advisory work in Dubai isn't just financial modelling. It involves coordinating with legal counsel, tax specialists, and compliance teams so the commercial structure doesn't collapse under regulatory review.

One practical example is tax and reporting readiness. Even where the core issue is a sale, recapitalisation, or refinancing, weak indirect tax housekeeping can create diligence friction. If your records need tightening, this guide to VAT services in Dubai is relevant because tax compliance problems often surface during transaction review, not before it.

The practical issues owners often underestimate

In live mandates, several themes show up repeatedly:

- AML and source-of-funds checks: Counterparties, banks, and regulated advisers will scrutinise ownership and transaction rationale.

- Beneficial ownership clarity: If shareholders, nominees, or holding structures are unclear, timelines stretch quickly.

- Licensing alignment: The entity's commercial activity and transaction purpose should make sense together.

- Approval pathways: Certain structures or stakeholders may require formal consent or staged approvals.

A business owner doesn't need to master every regulation personally. But they do need to understand that incomplete documents, inconsistent records, and unclear ownership narratives strengthen the other side's position.

Why timing matters more after 2024

Public advisory material in Dubai increasingly points to refinancing, debt restructuring, and strategic M&A support as active areas of demand, and it also highlights an important point: engaging an advisor before liquidity stress becomes visible is often the smarter move for UAE business owners, as discussed by FinAdvise Consultants on corporate finance advisory.

That point is practical, not dramatic. Once lenders, suppliers, or potential buyers believe the company has run out of room, the owner loses flexibility. Terms worsen. Buyers frame offers opportunistically. Management starts reacting instead of choosing.

In Dubai, early advisory work often protects bargaining power more than it changes accounting.

The businesses that manage the maze best usually start while they still have options.

How to Choose the Right Dubai Finance Advisor

A recognised brand doesn't guarantee the right fit. In corporate finance advisory Dubai mandates, the team on your file matters more than the logo on the proposal.

Some firms are strong at lender negotiations but weak in founder-led exits. Some are excellent with institutional processes but less useful for owner-managed companies where records are imperfect and decisions move through family dynamics rather than formal boards. Others are credible in valuation work but not in live execution.

The questions worth asking in the first meeting

Skip broad questions like “Do you cover M&A?” Nearly everyone says yes. Ask questions that reveal operating style.

- Who will run the mandate? Ask for names, roles, and who attends negotiations.

- What type of client do you handle most often? Family business, sponsor-backed company, startup, SME, or corporate carve-out are very different environments.

- How do you prepare a business before outreach? You want process discipline, not just introductions.

- Where do transactions usually get stuck? Good advisors answer this quickly and specifically.

- How do you handle weak data or disputed adjustments? This exposes whether they can work in real-world conditions.

- What is outside your scope? A serious firm is clear about boundaries.

Boutique vs larger firm

This isn't a simple good-versus-bad choice.

| Type | Strengths | Trade-offs |

|---|---|---|

| Boutique advisor | senior attention, flexibility, often better for founder-led situations | narrower sector reach or less bench depth |

| Larger firm | broader specialist network, more formal process, stronger cross-border coordination | more layers, possible junior-heavy execution, less flexibility |

If you're a venture-backed company or software business, investor fit also matters. Founder teams often waste time speaking to advisors who don't understand how sector-specific fundraising works. For market mapping, a resource like this list of top software VCs in UAE can help frame better questions around investor targeting, though the advisor still needs to convert that into a financing strategy.

The quieter signals that matter

There are also softer tests that tell you a lot.

If an advisor spends the first meeting selling certainty, be careful. Good advisors talk early about assumptions, risks, and what must be validated.

Check whether they can work alongside your existing providers. In many mandates, transaction readiness depends on coordination with accountants and auditors. If you need to review the quality of your current assurance support, this list of auditing firms in the UAE can help benchmark what kind of finance ecosystem you're building around the business.

The right advisor is the one who can improve decision quality, challenge weak assumptions, and stay useful when the transaction becomes uncomfortable.

Accelerate Your Growth with Smart Classic Business Hub

A common Dubai entry story looks like this. An investor sets up a UAE entity, opens banking, starts hiring, then spots an acquisition target. The deal looks attractive, but basic questions slow everything down. Is the shareholding structure right for the transaction? Do the accounts stand up to diligence? Will the licensing and tax setup still work after the acquisition closes?

That is where an integrated adviser earns their place. Smart Classic Business Hub works across company formation, compliance support, VAT and accounting coordination, and corporate finance in the same operating context. For an investor, that matters because transaction planning does not sit in isolation. The setup choices made in month one often shape how much flexibility you have in month six.

I see this issue regularly in Dubai. One provider handles incorporation, another handles bookkeeping, and a third is brought in when funding or acquisition talks start. The handoffs create delays, duplicated work, and avoidable risk. A coordinated approach gives you a cleaner sequence and fewer surprises.

A practical scenario

Take an overseas investor planning to establish a local entity first, then acquire a smaller operating business later. If the initial structure is poorly chosen, the acquisition can trigger rework across banking, governance, and reporting. If the records are weak, due diligence becomes slower and negotiation becomes harder. If the shareholder setup is too rigid, options narrow at the point where flexibility matters most.

These are not abstract finance problems. They affect timing, deal cost, and bargaining position.

What good coordination looks like

- Set the structure early: choose the entity, ownership, and operating model based on the likely funding or acquisition path.

- Prepare records before scrutiny starts: clean bookkeeping, VAT treatment, and management reporting reduce friction during diligence.

- Align finance materials: forecasts, assumptions, and historic numbers should tell one coherent story.

- Engage before pressure builds: the best time to bring in advice is when you still have options on timing, counterparties, and deal shape.

Dubai rewards preparation. Businesses that execute well usually make a few key decisions early, then build the transaction around them instead of fixing preventable issues mid-process.

If you are assessing funding, restructuring, valuation, or an acquisition in the UAE, Smart Classic Business Hub can help you map the sequence of setup, compliance, and corporate finance decisions with fewer disconnects between workstreams.