You've got the trade licence. The company is registered. The stamped documents are sitting in your inbox, and for a moment it feels like the hard part is done.

Then the practical questions start. Where will client payments land? How will you pay your visa costs, software subscriptions, suppliers, or staff? What will you show a bank when it asks how the business works? In the UAE, that next move is usually a business banking account, and it's where many founders realise company formation and operational readiness are not the same thing.

A lot of new entrepreneurs assume the bank wants a document set. In reality, the bank wants a story it can verify. If your papers say one thing, your ownership chart suggests another, and your expected activity doesn't fit the licence, the application slows down quickly. If everything aligns, the process becomes far more manageable.

Your Next Step After Getting a UAE Trade License

A common pattern looks like this. A founder sets up a mainland or free zone company, receives the licence, rents a desk or office, and starts talking to customers. The business is legally formed, but money still has nowhere proper to go.

That gap matters more than most founders expect. A company without a functioning account struggles to collect revenue cleanly, prove commercial activity, and build the transaction history that banks and counterparties like to see. If you're at that stage, this practical overview of a bank account in Dubai helps frame what comes immediately after incorporation.

What founders usually realise first

The first issue isn't banking theory. It's operations.

- Incoming funds need a home: Clients usually expect to pay a company account in the business name, not a personal account.

- Expenses need traceability: Licence renewals, payroll, subscriptions, and supplier payments should be visible as business transactions.

- Your financial record starts now: The first months of account activity often shape how smoothly later compliance, accounting, and renewals go.

Open the account before cash starts moving in multiple directions. Cleaning up mixed transactions later is always harder.

Many founders wait because they think they need to “start trading first” and sort the bank later. In practice, the account is often what allows trading to happen properly. It becomes the operating rail for the business, not a formality after setup.

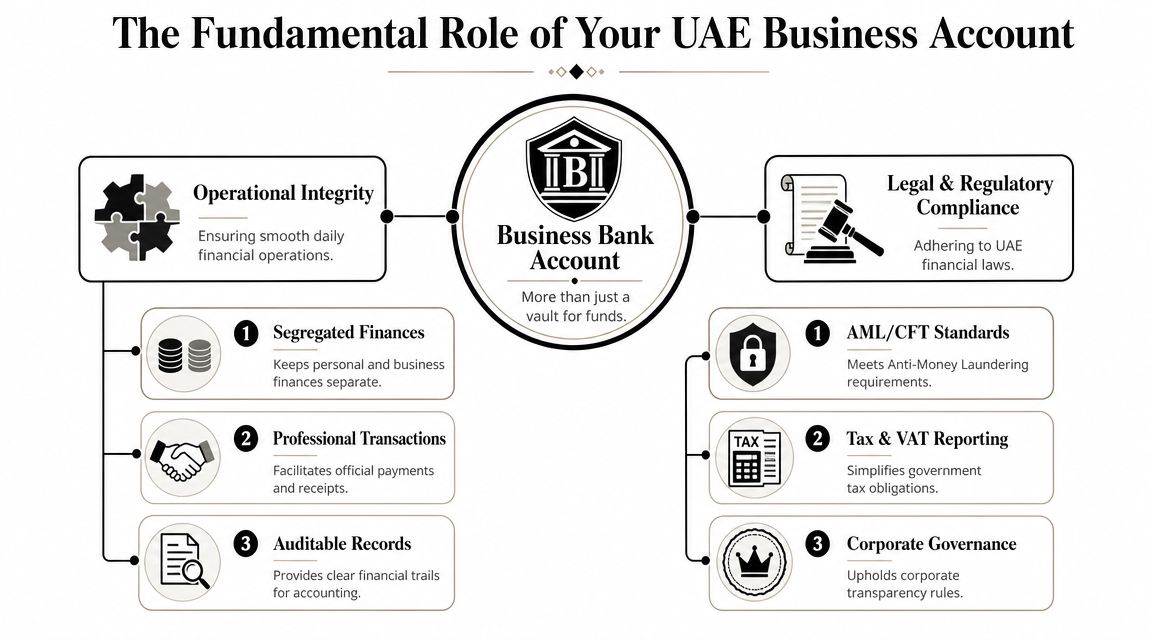

The Role of a Business Bank Account in the UAE

A business banking account in the UAE isn't just a place to store cash. It's the company's financial control centre. Think of it as a dedicated toolkit rather than a junk drawer. A personal account can hold money, but it isn't built to support company records, regulated payments, and a clean audit trail.

The UAE's private sector is dominated by small and medium-sized enterprises, which makes business banking the main channel for handling commercial activity. With VAT introduced in 2018, and with corporate tax compliance becoming more formalised, a dedicated account has become an important compliance tool for maintaining clear records for tax, audit, and licensing purposes, as outlined in the SBA guidance on opening a business bank account.

Why separation matters in practice

The simplest reason is clarity. When personal and business spending sit in the same account, every reconciliation becomes a manual exercise. That causes problems for bookkeeping, tax filing, internal control, and basic management reporting.

A separate account helps you manage:

- Operational cash flow: You can see what the business earns and spends without filtering out personal transfers.

- Payroll and supplier payments: These are easier to document when they move through a company account tied to the licensed entity.

- Bank reconciliation: Statements map more cleanly to invoices, contracts, and accounting entries.

- Regulatory reviews: If a bank or authority asks where funds came from, the trail is easier to prove.

Why the bank cares

Banks don't treat a business account like a simple retail product. They see it as part of the control framework around a legal entity. That's why even straightforward companies are asked questions about activity, ownership, and expected transaction behaviour.

A lot of founders focus only on fees or minimum balance. That matters, but so does fit. Some businesses want simplicity and low overhead, which is why founders often look at a zero balance business bank account in the UAE when their transaction profile is light and they don't need a heavy banking structure.

Practical rule: Your account should match how the company actually operates, not how you hope it will look on paper.

What a proper account supports

Below is the actual job description of a UAE business bank account.

| Function | What it supports |

|---|---|

| Commercial credibility | Receiving and making payments under the company name |

| Record integrity | Clean separation between owner spending and company activity |

| Compliance readiness | Better support for tax, audit, and licensing documentation |

| Financial management | Clearer cash position, budgeting, and reporting |

If you treat the account as only a banking product, the process feels unnecessarily strict. If you treat it as compliance infrastructure, the bank's questions make more sense.

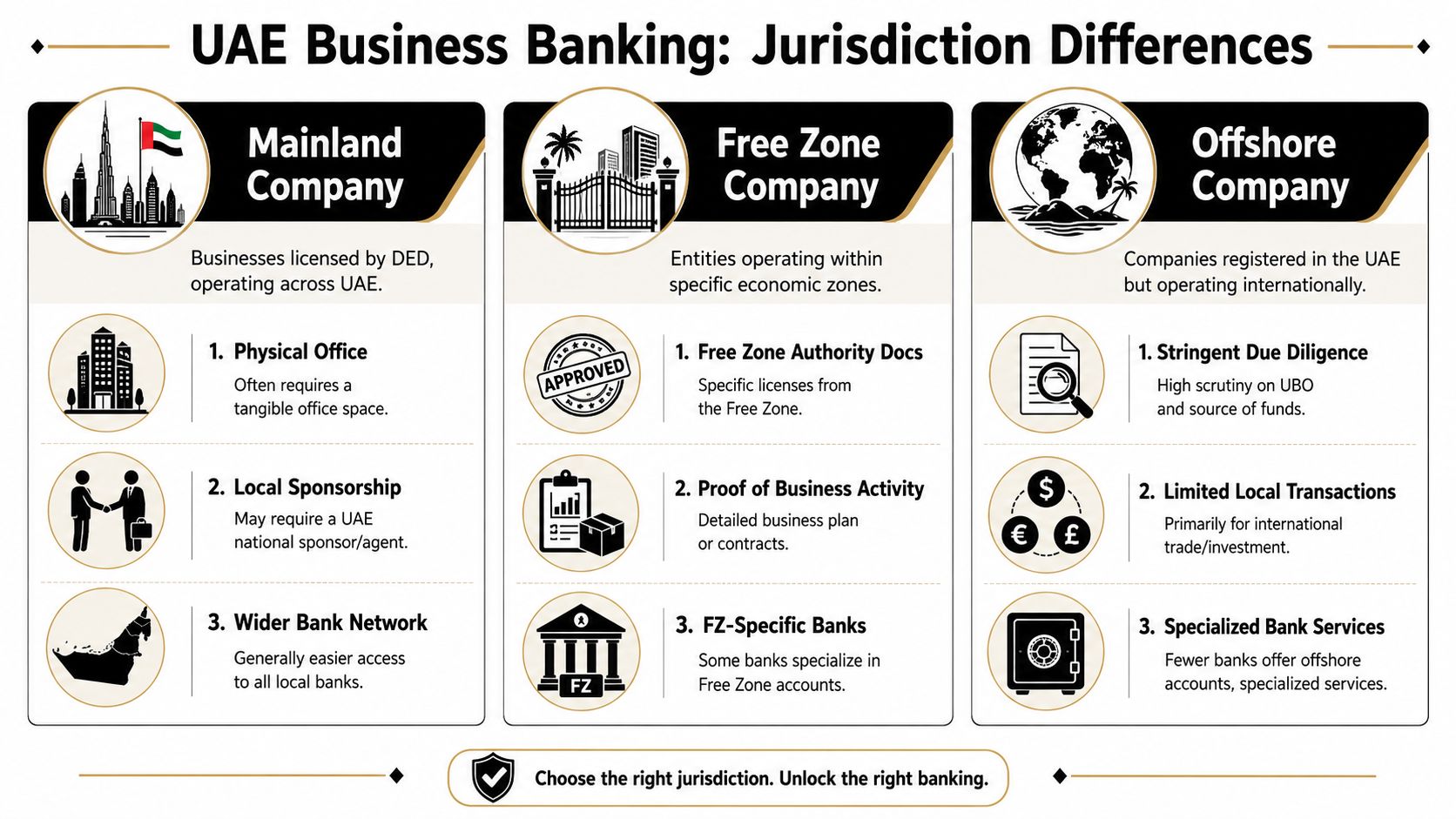

Banking Requirements Across UAE Jurisdictions

Banks don't look at every UAE company the same way. The jurisdiction shapes the risk review. A mainland company, a free zone entity, and an offshore structure can all be legitimate, but they present different questions around activity, control, and banking use.

Mainland companies

Mainland entities are often easier for banks to understand because the operating footprint is usually clearer. The company is licensed for UAE activity, and the business model often has an obvious domestic use case.

Banks still examine the basics closely:

- Office evidence: A physical address or workspace helps support operating substance.

- Licensed activity: The activity on the licence should line up with expected payments and counterparties.

- Shareholder clarity: Ownership and signing authority need to be straightforward and consistent.

For many founders, mainland banking feels more familiar because the bank can more easily connect the licence, address, and customer base.

Free zone companies

Free zone companies are common, practical, and often well suited to startups and international founders. But banks tend to ask sharper questions about how the company will operate outside the free zone paperwork.

The pressure points are usually these:

- Substance: Where is the business managed, and who is doing the work?

- Commercial proof: Contracts, invoices, website presence, and a credible business plan help.

- Transaction logic: The bank wants to understand why money will move through this UAE entity rather than another company in the group.

If you're forming in Ras Al Khaimah or already hold that structure, this overview of a RAK business account is useful for understanding jurisdiction-specific expectations.

Free zone companies don't fail because they are free zone companies. They run into delays when the paperwork is clean but the commercial narrative is thin.

Offshore companies

Offshore structures usually face the narrowest banking path. That doesn't mean impossible. It means the bank will want a stronger explanation of ownership, source of funds, and intended use of the account.

Here's a side-by-side view.

| Jurisdiction | What banks usually look for most closely | Common friction point |

|---|---|---|

| Mainland | Operating activity inside the UAE | Weak proof of real operations |

| Free zone | Substance and transaction rationale | Limited evidence of business activity |

| Offshore | UBO transparency and fund origin | Complex ownership chains |

What works across all three is consistency. If the licence, shareholder documents, signing powers, and expected activity tell the same story, the jurisdiction becomes easier for the bank to assess.

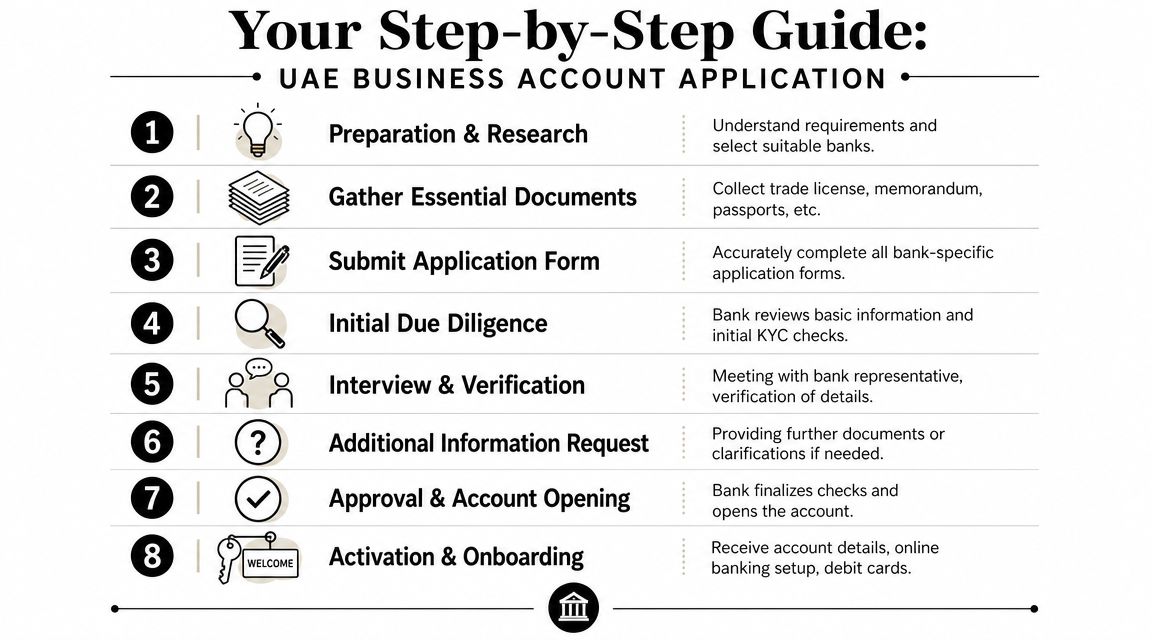

The Complete UAE Business Account Application Process

The UAE account opening process makes more sense when you stop treating it like a checklist and start treating it like a file review. The bank is trying to answer three questions. Who owns this business? What does it do? Where will the money come from and go to?

Under Federal Decree-Law No. 20 of 2018 on Anti-Money Laundering, banks must verify the customer, understand the business relationship, and apply ongoing monitoring. That's why requests for trade licences, UBO information, and proof of business activity are part of a stricter AML and KYC process, as explained in this overview of business account opening requirements.

Step one starts before the application form

The strongest applications are built before any form is submitted. Gather the standard documents, but also ask what each one proves.

- Trade licence: Confirms the entity exists and shows the licensed activity.

- MoA or AoA: Shows legal structure, shareholding, and internal authority.

- Passport and Emirates ID copies: Verify the identity of owners and authorised signatories.

- Shareholder register or ownership chart: Helps the bank trace control to the ultimate beneficial owner.

- Business activity evidence: Contracts, invoices, proposals, website material, or supplier relationships show that the company is real in commercial terms.

Your UBO story must be simple enough to follow

Often, founders get stuck. They submit the documents, but the documents don't explain the structure. If there's a holding company, nominee layer, overseas shareholder, or multiple investors, the bank needs a clear map.

A short cover note often helps. It should explain:

- who ultimately owns or controls the business

- how the company makes money

- what countries, clients, or suppliers are involved

- what level of account activity you reasonably expect

That note shouldn't be sales language. It should be factual and easy to verify.

If a compliance officer has to guess how the ownership chain works, the file slows down immediately.

The meeting with the bank matters more than founders expect

By the time you meet a relationship manager or onboarding officer, the bank may already have flagged gaps internally. The discussion is not only about introductions. It's often where the bank tests whether the person opening the account understands the company.

Be ready to answer practical questions:

- Why was this jurisdiction chosen?

- Who are the expected customers?

- Will the business handle local or cross-border payments?

- What is the source of initial funding?

- Who will operate the account day to day?

Founders with LLC structures may also find it useful to review a broader guide to opening an LLC bank account from Steingard Financial. It's not UAE-specific, but it helps frame how banks generally think about entity documentation and account authority.

What speeds up approval

A fast application usually has these qualities:

| What works | What causes delays |

|---|---|

| Matching names across all documents | Different spellings, outdated passports, inconsistent signatures |

| Clear ownership chart | Unexplained holding layers or unclear control |

| Evidence of actual business activity | Licence with no commercial narrative |

| Plausible transaction profile | Vague or unrealistic payment expectations |

The bank is not asking for a pile of papers. It's asking for a coherent business profile.

Overcoming Common Account Opening Hurdles

Most account problems in the UAE are not caused by fraud. They're caused by friction. The founder knows the business is legitimate, but the file in front of the bank still looks incomplete, inconsistent, or difficult to interpret.

Hurdle one: document mismatch

This is the most common issue I see. The trade licence shows one activity description, the website markets something broader, and the proposal deck describes something else again. None of that may be fatal on its own, but together it creates uncertainty.

Fix it by reviewing the file as a banker would:

- Check legal names carefully: The shareholder names should match across the licence, constitutional documents, passports, and application forms.

- Align business descriptions: Your website, invoice samples, and bank narrative should all describe the same core activity.

- Use one ownership chart: Don't submit different versions to different people in the process.

Hurdle two: unclear UBO structure

Banks need to identify who ultimately owns or controls the company. Problems start when founders submit only the immediate shareholder details without explaining who sits behind them.

If the structure is layered, provide:

- A simple chart: Show each layer from the UAE company up to the final beneficial owner.

- Supporting constitutional documents: Include the documents that support each ownership link.

- A short explanatory note: State who controls the entity and who will benefit economically.

A complicated structure can still be bankable. An unexplained structure usually isn't.

Hurdle three: the wrong account type

A common but often overlooked problem is choosing an account that doesn't fit the company's transaction profile. A low-volume consultancy may end up paying for features it won't use, while a trading business may choose a basic account and then struggle with operational needs. That mismatch affects cash flow and day-to-day efficiency, as discussed in this article on why account structure matters for business operations.

Use this quick lens before applying:

| Business type | Usually needs | Often doesn't need |

|---|---|---|

| Consultancy or solo service firm | Clean online banking, low-friction transfers, basic controls | Heavy trade features |

| Trading company | Cheque support, foreign currency handling, stronger cash management | Minimalist retail-style setup |

| Agency or growing SME | Multi-user access, payroll handling, solid reporting | Overbuilt structures with little operational benefit |

Hurdle four: poor transaction evidence

Some founders say, “We're new, so we have no activity yet.” Banks understand that. What they don't like is silence. If there are no invoices yet, provide signed proposals, draft agreements, supplier discussions, a business plan, or proof of operating spend.

When you start reconciling those transactions later, process quality matters. A practical external resource is this guide to bank statement automation, which shows how structured statement review can reduce manual checking when accounting volume starts to grow.

How to Compare UAE Banks and Account Features

Most founders compare banks by looking at fees first. That's understandable, but it's incomplete. The better question is whether the bank fits the way your company moves money.

The UAE banking market has shifted strongly towards digital usage. Mobile banking is widely used for core tasks, with 94% of mobile-banking users checking balances or transactions and 58% transferring money between accounts, according to ValuePenguin's banking statistics and trends. In the UAE business context, that behaviour has helped push online banking adoption, especially for startups and free zone companies that want faster, lower-friction servicing.

Build a scorecard before you choose

Use a short decision matrix instead of reacting to marketing language.

- Digital platform quality: Check whether approvals, transfers, statement access, and user permissions are easy to manage.

- Relationship support: Some businesses still need a human contact for exceptions, documentation, or operational issues.

- Currency and transfer needs: If you invoice internationally, the bank's handling of cross-border payments matters.

- Operational tools: Payroll support, cheque capability, and account access controls should fit your actual setup.

Traditional bank or digital-first option

This choice depends less on brand preference and more on transaction pattern.

A traditional bank often suits businesses that expect more documentation-heavy operations, need branch support, or may later request broader facilities. A digital-first option can work well for lean service companies that value quick access, simple interfaces, and low administrative friction.

Here's a practical comparison.

| Priority | Better fit may be |

|---|---|

| Fast setup and daily online use | Digital-first model |

| Complex operations and broader banking relationship | Traditional bank |

| Simple consultancy profile | Low-friction, fee-light account |

| Trade-heavy business | Bank with stronger operational tooling |

Don't choose the cheapest account. Choose the account that will still work when your first few clients, suppliers, and staff all hit the system at once.

One practical option founders often use during this stage is Smart Classic Business Hub, which supports company setup, compliance documentation, and banking preparation in the UAE. Used properly, that kind of support is less about “introductions” and more about packaging the file so the bank can understand it quickly.

Partner with Smart Classic for a Seamless Banking Experience

Opening a UAE business banking account is rarely difficult because the bank wants to be difficult. It's difficult because the bank has to defend every approval. Once you understand that, the process becomes far more logical.

What founders usually need is not another checklist. They need help turning their company documents into a clear application narrative. That means matching the licence to the business model, clarifying the ownership chain, preparing UBO support, and making sure expected account activity sounds commercially credible.

A consultant can also help you avoid avoidable mistakes, such as applying to the wrong bank category, presenting a weak explanation of foreign ownership, or submitting inconsistent paperwork from different stages of company formation. Those are the issues that consume time.

The strongest applications I see have three things in common:

- Consistency: every document points to the same ownership and activity story

- Context: the bank can understand why the entity exists and how it will be used

- Fit: the chosen account structure matches the company's real transaction pattern

If you're still at the stage where the process feels opaque, that's normal. The UAE banking environment rewards founders who prepare properly, answer directly, and treat compliance as part of doing business, not as an obstacle standing outside it.

If you want help preparing a bank-ready application, refining your ownership narrative, or matching your company profile to the right banking route, Smart Classic Business Hub can support the process from setup through compliance documentation and practical account-opening preparation.