A founder gets the trade licence issued, opens payroll files, lines up suppliers, then loses two or three weeks because the bank asks for more proof of activity, owner background, or expected transactions. That is a common UAE banking problem. The bank account decision affects operations early, not just finance later.

In the UAE, a business account touches supplier payments, staff salaries, VAT administration, card settlements, and sometimes the pace of visa and company setup work. Banks do not only review the trade licence. They also assess what the company does, who owns it, where funds come from, and whether the expected activity fits the account profile. If your legal setup is still being finalised, this guide also pairs well with choosing the right business structure.

Different businesses get very different treatment. A mainland contracting company, a free zone consultancy, an e-commerce seller, and a foreign-owned holding structure will not face the same onboarding path. Non-resident shareholders and newly formed companies usually face more questions, more document requests, and longer review times. If you are still preparing incorporation and account-opening documents, this practical guide to a bank account in Dubai helps set expectations.

This guide is not just a list of big bank names. It is a decision framework. The goal is to match each bank to the business profile it suits best, whether you are a startup that wants speed, an SME that needs branch support and credit options, or a foreign-owned company trying to clear compliance without unnecessary delays.

I have focused on the points that decide outcomes in practice. Eligibility, minimum balance pressure, digital usability, foreign-owner friction, and the documents each bank is likely to scrutinise first.

1. Wio Business

Wio Business suits founders who want banking to behave like modern software. If your business runs online, your team needs cards quickly, and you don’t want to structure your cash flow around branch visits, Wio is one of the cleaner options in the market.

It’s strongest for service businesses, agencies, small trading setups with straightforward flows, consultants, and early-stage startups that value speed over legacy banking extras. The experience is app-led, and that changes the day-to-day feel of the account. Approvals, user access, cards, and transfers tend to feel more operationally tidy than what many traditional SME accounts offer.

Where Wio works well

Wio’s practical strength is control. Teams can run daily banking from the app, issue virtual and physical cards, assign permissions, and work across multiple currencies including AED, USD, EUR, and GBP. For a founder who wants to separate spend authority without building a heavy finance function, that’s useful from day one.

The pricing model also appeals to businesses that prefer a fixed monthly cost over balance penalties. Some owners like that predictability because it removes the guessing game around fall-below fees. Others won’t. If your company keeps a healthy balance and barely uses the account’s advanced tools, a subscription can feel expensive compared with a basic relationship account at a conventional bank.

Practical rule: Choose Wio when speed, card controls, and multi-currency access matter more than cheque-heavy operations or complex trade instruments.

A lot of new founders also use Wio after getting clarity on the process for opening a bank account in Dubai, because the account setup conversation usually goes better when the licence activity and ownership story are already presented cleanly.

Where Wio can frustrate you

Wio isn’t the best fit for every UAE company. If your business still depends on cheques, frequent cash handling, or complex trade finance, you’ll feel the limits quickly. Traditional banks still do better with layered facilities, deeper branch support, and old-school operational requests that many established UAE businesses still rely on.

This is also where business profile matters. A digital bank may be efficient, but compliance will still look closely at foreign ownership, source of funds, and actual operating substance in the UAE. If your company is offshore in style but trying to present itself as an active local trading operation, Wio won’t solve that mismatch.

Best fit

- Digital-first startups: Founders who want quick controls, simple access management, and a modern interface.

- Lean SMEs: Companies that don’t want to hold large idle balances just to avoid account charges.

- Multi-currency operators: Businesses billing or paying in a few core currencies without needing full treasury support.

For many startups, Wio is easy to like. The trade-off is simple. It gives convenience and visibility, but it won’t replace a full-service bank if your business grows into heavy financing, structured trade, or high-touch relationship banking.

Visit Wio Business.

2. Mashreq NeoBiz

A common UAE founder scenario looks like this. The company is newly licensed, clients want to pay into a bank they already know, salaries may start soon, and the owner does not want a branch-heavy setup for basic transactions. Mashreq NeoBiz is often shortlisted at that point because it sits between a newer digital platform and a traditional SME bank account.

That position is its main strength. NeoBiz gives SMEs a digital onboarding path and practical day-to-day banking tools, while still carrying the credibility of a long-established local bank. For some businesses, that recognition helps with landlords, corporate customers, and finance teams that still prefer established UAE banking names on invoices and contracts.

The key trade-off with NeoBiz

NeoBiz usually makes more sense for companies with predictable balances than for startups still managing uneven cash flow. The account is built for routine operating use, especially local transfers and payroll-linked activity, but the balance requirement changes the calculation.

Mashreq’s plan structure means an average monthly balance of AED 50,000 is needed to avoid the fall-below fee. For a stable SME, that may be acceptable. For a new consultancy, agency, or trading company still collecting its first few invoices, it can feel expensive to park that amount just to keep the account efficient. If balance pressure is your main concern, compare it against Emirates NBD business account minimum balance requirements and lower-commitment alternatives before deciding.

The existing internal comparison on business account options with no minimum balance expectations in the UAE is useful here because founders often focus on the bank name first and the operating conditions second.

I see this mistake often. A founder picks NeoBiz for brand comfort, then realises a few months later that the company would have been better served by an account with less balance pressure and fewer maintenance conditions.

Who usually fits NeoBiz best

NeoBiz is a sensible choice for UAE businesses that need straightforward local banking and expect regular account activity from the start. It suits companies that want digital access but are not trying to optimise for the absolute lowest entry threshold.

It tends to fit:

- Service SMEs with steady monthly receipts: Agencies, consultancies, and operating businesses that can maintain the required balance without strain.

- Companies running payroll early: WPS support matters once staff salaries become part of monthly operations.

- Founders who want a recognised local bank: Useful when customers or counterparties are more comfortable dealing with established UAE institutions.

It is less attractive for founders in year one who need flexibility more than prestige. If receipts are inconsistent, or the business is still proving its model, the account can become something you manage around rather than something that supports growth.

Another point gets missed in simple ranking lists. Eligibility and account comfort are not the same thing. A company may qualify on paper, but foreign ownership structure, business activity, expected transaction pattern, and proof of genuine UAE operations still shape how smooth the review process will be.

Visit Mashreq NeoBiz.

3. Emirates NBD Business Banking

A common UAE founder scenario goes like this. The company opens an account that works for basic transfers, then six or twelve months later it needs stronger online banking, trade support, better FX handling, or a bank name that larger counterparties already recognise. That is where Emirates NBD usually enters the shortlist.

Emirates NBD suits businesses that want a bank they can stay with as operations become more demanding. The appeal is not low-friction entry alone. It is the range. A startup can begin with a simpler package, then add more structured banking support later without changing institutions and redoing the full relationship from scratch.

For many early-stage companies, the practical draw is the Connect package because it removes the monthly average balance requirement. That matters in the first operating months, especially for service firms, project-based businesses, and new trading entities where receipts can be irregular. Once volumes increase, the bank has a clearer path into higher-service arrangements, online banking tools, and trade-related capabilities than lighter digital-first options.

Foreign-owned companies often ask me whether Emirates NBD is realistic. In many cases, yes. The bank is open to international ownership structures, but approval still depends on how well the file is presented. Shareholder documents, proof of address, business activity, UAE presence, expected transaction pattern, and the commercial logic behind cross-border payments all matter. A foreign-owned free zone company with a clear operating story usually has a better experience than a paper-only structure with vague activity and no evidence of actual business in the UAE.

The main mistake is assuming a large bank means an easier approval process. Usually, it means more scrutiny once the ownership chain or payment flows become more complex. That is not a bad thing. It means founders should prepare properly before applying.

Another point matters here. Emirates NBD can be a strong long-term bank, but the right package still needs to match your current stage. Entry-level access and long-term suitability are not the same decision. If you choose a tier that looks good on paper but creates avoidable balance pressure, the account becomes an operational burden. If you want to compare thresholds before applying, review the Emirates NBD business account minimum balance requirements.

Best fit

- Startups that want a recognised UAE bank: Useful for founders who want credibility with clients, suppliers, and local counterparties from the start.

- SMEs likely to scale into trade, FX, or heavier transaction volumes: Better fit than entry-only banking options if the business model is expanding.

- Foreign-owned operating businesses with proper documentation: Strong candidate where the company can show real UAE activity and a clear payment profile.

Visit Emirates NBD Business Banking.

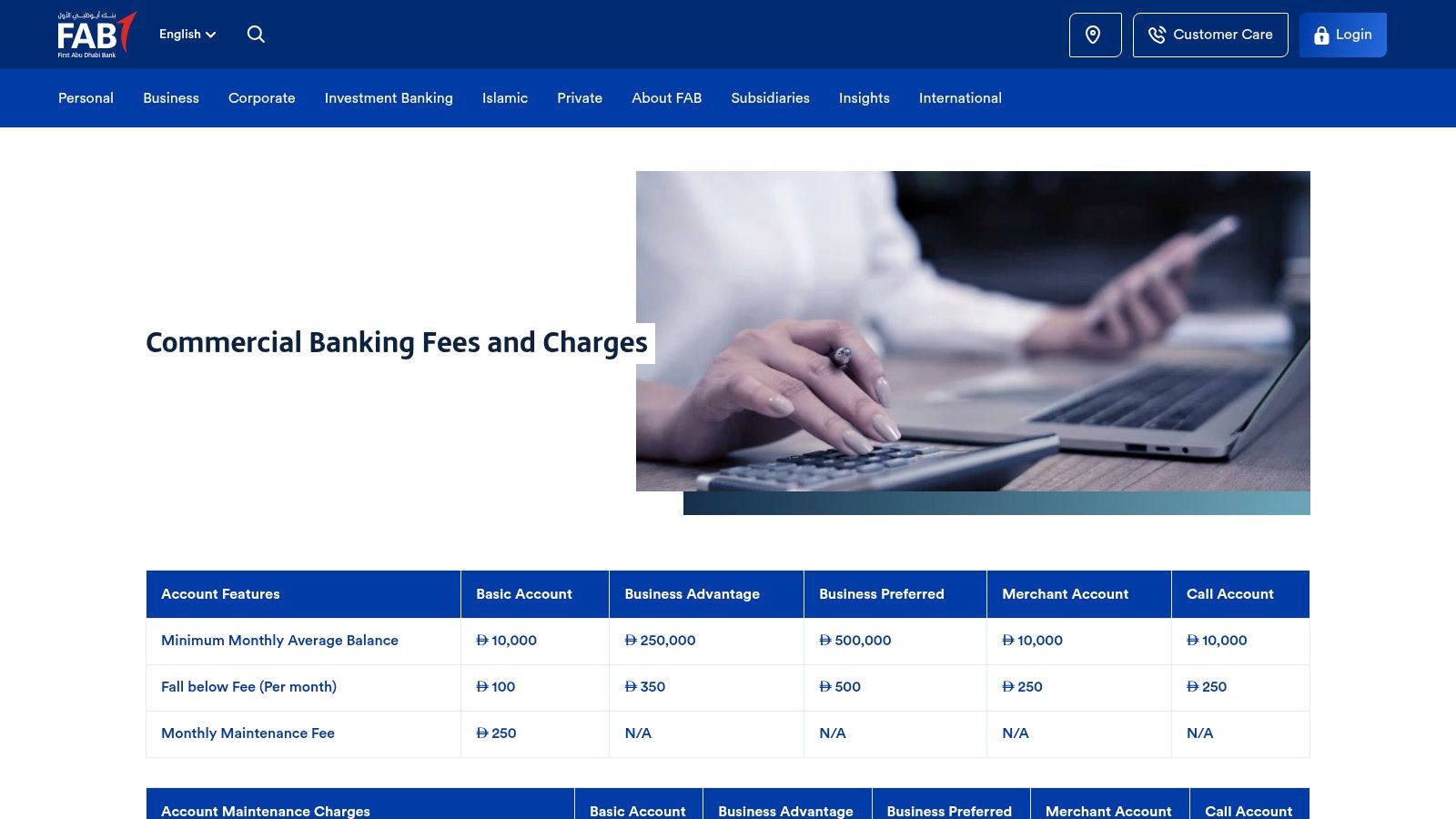

4. First Abu Dhabi Bank FAB

A company with stable monthly turnover, proper management accounts, and plans to add trade or card facilities will usually assess FAB very differently from a newly formed startup. That is the right way to judge this bank. FAB is strongest when the business already has shape, not when the founder is still trying to prove the model.

The bank appeals to owners who want structure. Its business banking setup is easier to assess than some competitors because the tiers, charges, and service ladder are visible early. For a finance manager or shareholder group, that matters. They can see the cost of the relationship, set balance expectations internally, and avoid surprises later.

FAB also makes more sense if the account is part of a wider banking plan. A business may start with day-to-day transactions, then need merchant acquiring, trade support, liquidity products, or borrowing. FAB suits that progression better than banks built mainly for simple entry-level account opening.

The trade-off is clear. FAB is not usually the bank I would put in front of a founder who wants the lightest possible onboarding process. It is more suitable for companies that can present a clean file from day one. That means a clear ownership chain, matching licence activity, sensible expected volumes, and documents that support the source of funds and the reason the UAE entity exists.

Balance requirements are another filter. In this article’s plan notes, Business Advantage is tied to AED 250,000 and Business Preferred to AED 500,000. Many SMEs can meet those thresholds, but they should still ask a basic question first. Does holding that much cash in the account improve operations enough to justify the cost of tying it up?

I also find that FAB works better for firms with a predictable operating profile. If the company has irregular inbound payments, a complicated group structure, or overseas counterparties that are hard to explain, review tends to become slower and more document-heavy. That does not mean rejection. It means more preparation is needed before the application goes in.

Post-corporate tax, that preparation matters even more. Banks are paying closer attention to whether the account profile, business activity, and supporting records line up properly. FAB tends to suit businesses that already keep orderly books and can explain their commercial rationale without gaps.

Best fit

- Established SMEs with stronger documentation: Better for businesses that can show real activity, clean ownership records, and consistent financial evidence.

- Companies planning to add banking products later: A practical choice if trade, merchant services, treasury, or credit may become relevant.

- Shareholder-led or finance-led businesses: Useful where published pricing, internal controls, and clearer banking governance matter.

Visit First Abu Dhabi Bank.

5. ADCB Business Choice Accounts

A trading company with steady monthly collections, a services firm that wants cleaner statements, and a foreign-owned SME trying to avoid vague package terms will not all choose the same bank for the same reason. ADCB earns its place here because the decision is usually clear early. If your business can maintain the required balance and you want a conventional UAE bank with readable package rules, ADCB is often a sensible fit.

That clarity is useful in practice.

ADCB’s Business Choice range is built in visible tiers. Silver, Gold, and Platinum give owners a straightforward way to judge whether the relationship makes financial sense before they start the paperwork. For SMEs that are tired of hearing broad promises and then discovering conditions later, that matters more than flashy positioning.

There is also an Islamic Business Choice version for companies that want Sharia-compliant banking but still prefer a familiar package structure. That widens ADCB’s appeal, especially for firms comparing conventional and Islamic options on process rather than branding.

The digital side is functional and predictable. You get phone, internet, and mobile banking, and the key product documents usually make the fee exposure easier to assess before account opening. I see this matter most for owner-managed businesses where the finance process is still lean and nobody has time to decode unclear charges after the fact.

A practical fit for finance-led SMEs

ADCB tends to suit businesses that care about control, documentation, and routine account use more than product novelty. If the company books transactions properly, files VAT on time, and wants statements and account activity to be easy to reconcile, ADCB is often a more comfortable choice than banks that sell a stronger digital story but create more cleanup work behind the scenes.

That trade-off is real. A bank can look cheaper on paper and still cost the business more if your accountant spends extra time fixing exports, matching unclear entries, or chasing missing detail.

For UAE SMEs under more scrutiny on tax records and source of funds, that operational neatness has value. ADCB is not the bank I would place first for a founder who wants fintech-style expense controls or rapid experimentation. I would place it higher for a company that wants a stable local banking relationship and fewer surprises in day-to-day administration.

Best fit

- Established SMEs with routine transaction patterns: Works well for businesses with predictable inflows, regular supplier payments, and basic treasury needs.

- Finance-conscious owner-managed companies: A practical option if statement clarity, reconciliation, and fee visibility matter more than advanced app features.

- Businesses choosing between conventional and Islamic structures: Useful where the company wants comparable package logic across both options.

Where ADCB is weaker

- Fall-below charges still need attention: The account only stays cost-effective if the balance discipline is realistic for the business.

- Less attractive for early-stage startups: Founders looking for faster setup, lighter entry criteria, or modern card tooling may find it conservative.

- Fewer obvious premium extras: It covers core banking well, but it does not stand out as the broadest ecosystem for complex expansion plans.

Visit ADCB Business Choice Accounts.

6. ADIB Abu Dhabi Islamic Bank Business Account Packages

ADIB is the practical answer when a founder wants Sharia-compliant business banking without being pushed into a niche or underdeveloped SME experience. The bank’s package structure is clearer than many people expect, and the availability of a no-minimum entry route makes it relevant to startups as well as more established businesses.

That point matters because some owners assume Islamic banking always means heavier onboarding or fewer digital options. In ADIB’s case, that’s too simplistic.

Why ADIB deserves a place on this list

ADIB’s package range gives different business types a usable entry point. Business One, Premium, Elite, and Business Connect create a ladder, not a single rigid product. Business Connect is particularly important because it offers a no-minimum-balance route for companies that need compliant banking access before they can justify tying up funds.

For startup founders and service firms, that flexibility can be the deciding factor. You get Sharia-compliant banking, digital management through ADIB Direct, and a published package framework rather than vague verbal guidance.

This is one of the better examples of a bank that works for both principle-led and practical decision-making. Some clients choose ADIB for faith-based reasons. Others choose it because the package logic works better for their stage.

What to watch before opening

The lower-balance reality can still bite. Monthly charges at modest balances may feel heavy if the company is still pre-revenue or only lightly active. That’s the part to assess thoroughly. A no-minimum route doesn’t automatically mean a low-cost route.

The higher packages also tend to reward stronger balances and more mature relationships. So ADIB is best chosen intentionally, not just because it appears to remove one barrier at the start.

Best fit

- Founders requiring Sharia-compliant banking: ADIB is one of the clearest mainstream options.

- Startups needing a lighter entry path: Business Connect can help where other banks insist on higher balances.

- SMEs that want digital access with Islamic banking: ADIB Direct keeps the account practical for day-to-day use.

"Choose the Islamic bank that matches your operating pattern, not only your preference label. The account still has to work every day."

ADIB is one of the good banks for business accounts when compliance is paramount but operational usability still matters. It won’t be the best answer for every foreign-owned structure or every high-volume trading company. But for many UAE SMEs, it strikes a workable balance between values, transparency, and utility.

Visit ADIB Business Account Packages.

7. HSBC UAE Business Banking

A common UAE banking scenario looks like this. The company is incorporated locally, but the money flow is not. One shareholder sits overseas, suppliers invoice in other jurisdictions, and customers may pay from outside the UAE. That is the point where HSBC usually enters the shortlist.

HSBC suits businesses that need an international banking setup, not just a local account with outward transfers. The difference shows up in day-to-day operations. Multi-country payment flows, group visibility, treasury coordination, and global banking familiarity all matter more here than app-first convenience.

Where HSBC stands apart

HSBC is usually stronger for UAE companies with regular cross-border activity, foreign ownership, or group reporting requirements. Its business banking structure is built around relationship tiers such as Standard, Ascend, and Vantage, with published tariff information that makes cost comparisons easier before you speak to a relationship manager.

HSBCnet is one of the main reasons established firms choose the bank. Finance teams that need tighter control over approvals, payment visibility, and international cash management will generally find more depth here than in startup-focused SME accounts.

That does not make HSBC the automatic best option. It makes it a better fit for a specific profile.

For foreign-owned entities, the primary issue is eligibility and documentation. HSBC will usually expect a cleaner file than lighter-entry SME banks. Clear shareholding records, a sensible business model, source-of-funds support, and a straightforward explanation of why the UAE entity needs the account all help.

Why some SMEs should still avoid it

HSBC can be the wrong choice for a young business with simple needs. If the company mainly needs local collections, payroll, card spending, and occasional transfers, the account may feel heavier than necessary.

Balance expectations are also a practical filter. The relationship tiers are aimed at businesses that can maintain more meaningful balances, not founders trying to keep banking costs low while the company is still proving revenue. That trade-off matters. A globally recognised bank name does not help much if the account economics are uncomfortable from month one.

The onboarding process can also be slower. International banks often ask more questions, not fewer.

Best fit

- Importers, exporters, and trading firms: Better suited to companies with regular overseas payments and receipts.

- Foreign-owned UAE entities: Useful where shareholders or parent companies prefer a bank with international familiarity.

- Mature SMEs with an active finance team: Stronger fit if the business will use HSBCnet, approval controls, and cross-border cash management tools.

A practical rule applies here. Choose HSBC because your operating model is international, not because the brand feels safer. In UAE business banking, global banks still apply strict compliance checks. Sometimes they apply them more tightly.

Visit HSBC UAE Business Banking.

Top 7 Business Bank Accounts Comparison

| Provider | 🔄 Onboarding & complexity | ⚡ Resource / Cost | 📊 Expected outcomes (impact) | 💡 Ideal use cases | ⭐ Key advantages |

|---|---|---|---|---|---|

| Wio Business | App-led, fully digital; very low setup complexity | Subscription pricing (e.g., AED 249/mo); predictable monthly fee | Fast access to multi‑currency accounts, virtual cards and basic transfers | Startups/SMEs needing rapid setup, virtual cards and predictable costs | Fast digital UX; predictable pricing; multi‑currency & card controls |

| Mashreq NeoBiz | Online SME onboarding with some legacy bank steps; moderate complexity | Competitive domestic transfer pricing; AED 50,000 avg monthly to avoid fall‑below fee | Cost‑efficient local payments and payroll (WPS) within an established bank | SMEs wanting WPS and low‑cost domestic operations with bank backing | Established bank support; clear KFS; competitive local fees |

| Emirates NBD Business Banking | Multiple packages (Connect for no‑min); moderate onboarding depending on tier | Tiered balances; fall‑below fees at non‑Connect tiers; scalable costs | Scalable suite (trade, FX, treasury) with easy upgrade path as business grows | Businesses planning to scale into trade finance, FX and treasury services | Comprehensive ecosystem; wide network; easy upgrade path |

| First Abu Dhabi Bank (FAB) | Formal onboarding and relationship management; longer than digital banks | Clear published minimums (e.g., AED 250k/500k) and predictable fee schedule | Access to merchant acquiring, loans and trade finance; budgeting certainty | SMEs expecting higher balances and needing broad product range | Transparent tariffs; natural upgrade path; broad product stack |

| ADCB – Business Choice Accounts | Conventional tiered onboarding; standard bank processes | Clear balance grid (Silver AED10k; Gold AED50k; Platinum AED100k); fall‑below fees | Predictable monthly charges; option for Islamic mirror product | Businesses wanting straightforward tiering and optional Sharia compliance | Clear balance/fee grid; conventional + Islamic options |

| ADIB – Business Account Packages | Multiple Sharia‑compliant packages; ADIB Direct enables digital management | Some packages have no‑min entry (Business Connect); monthly fees vary | Sharia‑compliant SME banking with digital access and upgrade routes | Entrepreneurs needing Islamic banking and a no‑minimum entry option | Sharia compliance + digital access; no‑min startup option |

| HSBC UAE – Business Banking | Tiered relationship onboarding; stricter for international services | Higher relationship minimums (e.g., AED100k–1,000k); HSBCnet fees apply | Strong cross‑border payments, treasury and global connectivity | Firms trading internationally or requiring a global bank partner | Global network; HSBCnet for treasury; transparent tariffs |

Navigate Banking with Confidence Your Next Step

Choosing the right business bank account in the UAE affects more than where your money sits. It changes how quickly you can start trading, how smoothly you can pay staff and suppliers, how well your records hold up under review, and how much friction you carry into your first year of operations.

That’s why I don’t advise founders to ask only, “Which bank is best?” The better question is, “Which bank fits this company as it exists today?” A digital startup with lean overhead usually needs speed, app controls, and low operational friction. A scaling SME may need stronger local credibility, better account structure, and access to trade or merchant services. A foreign-owned entity often needs a bank that can handle a more detailed compliance file without turning the process into a dead end.

The seven options above each solve a different problem. Wio works when banking needs to feel fast and controllable. Mashreq NeoBiz suits operators who want a recognised local bank with a more digital setup. Emirates NBD gives many businesses a strong runway from entry-level banking into larger facilities. FAB makes sense for structured SMEs that want a published path into deeper commercial banking. ADCB is excellent when clarity and accounting practicality matter more than flair. ADIB gives founders a serious Islamic banking route without making the account feel secondary. HSBC stands out for firms whose business is international from the beginning.

The hardest part usually isn’t choosing from the shortlist. It’s getting through onboarding cleanly. That’s where many good applications fail. Documents don’t match. The licence activity is too broad. The shareholder profile raises extra questions. The proof of address or operating rationale isn’t presented properly. For non-resident owners, this is even more common. In practice, the difference between an approved account and a delayed one is often preparation, not bank quality.

This is also why banking should be considered alongside the rest of your setup. Company formation, PRO support, VAT-compliant bookkeeping, tax residency planning, and even future liquidation all connect back to how the account is opened and maintained. If your records are weak after opening, reconciliation becomes painful later. It’s worth tightening that side early, especially if your finance team is still small. For businesses cleaning up their finance process, this primer on how to reconcile bank accounts is a useful operational companion.

Smart Classic Business Hub helps bridge that gap between “bank options on paper” and “a bank account opened.” The value isn’t just in handing you a list of banks. It’s in matching your business profile to the right institution, preparing the file the way compliance teams expect to see it, and reducing the back-and-forth that slows founders down.

If you’re setting up in the UAE, especially with foreign ownership, free zone activity, VAT exposure, or a more complex shareholder structure, getting support early usually saves time. It also gives you a better chance of opening the right account the first time instead of restarting the process after a rejection or long delay.

Smart Classic Business Hub supports founders, SMEs, and foreign investors with company formation, PRO services, VAT-compliant accounting, tax residency support, and practical bank account assistance across the UAE. If you want help choosing and opening the right business bank account for your company profile, speak with Smart Classic Business Hub.