You're probably in this position right now. You have a UAE business, a Singapore company or planned Singapore structure, and income is moving across borders through royalties, dividends, service fees, or investment returns. The commercial side is working. The tax paperwork isn't.

That gap is where people lose money.

A Singapore Certificate of Residence, often shortened to COR, is one of the few documents that can directly affect whether another country gives you treaty relief on cross-border income. If you run an international structure from Dubai, Abu Dhabi, or a UAE free zone, you should treat the tax residency certificate Singapore process as part of your operating model, not an afterthought.

Most online guides make this sound administrative. It isn't. A COR is closer to a tax passport. It proves to foreign tax authorities that you or your company is tax resident in Singapore for treaty purposes. Without it, your structure may still exist legally, but it may not get the treaty outcome you expected.

That matters even more for founders who split time between jurisdictions or use a Singapore holding or licensing company alongside UAE operations. If you're reviewing UAE personal tax planning considerations while also structuring international income, you need both sides aligned. And if you want broader cross-border context, these sophisticated tax reduction insights are useful because they frame tax efficiency as a systems issue, not a single-document exercise.

Your Gateway to Global Tax Efficiency

A UAE-based entrepreneur often chooses Singapore for credible banking, treaty access, investor familiarity, and legal certainty. Those are sensible reasons. But they only produce tax results if the tax position is defensible.

Take a common setup. A UAE principal owns or controls a Singapore entity that receives income from another country. The business owner assumes the treaty network will automatically reduce foreign withholding taxes. Then the foreign payer asks for a Certificate of Residence, and the file stalls. Suddenly the structure looks incomplete.

Why the COR matters in practice

A Singapore COR exists to prove tax residency for claims under Singapore's double-tax agreements. That's the practical point. It isn't a ceremonial letter. It's the document that supports reduced withholding tax treatment or other treaty relief when income crosses borders.

For UAE-based groups, that creates a simple rule. If your Singapore entity is expected to receive treaty benefits, you should plan for COR eligibility before the first payment hits the account.

A company can be perfectly incorporated and still fail the tax residency test that matters for treaty claims.

That's where many founders get caught. They spend time on incorporation, account opening, licences, and contracts. They spend far less time on governance records, decision-making location, and substance. Those are the items that decide whether the tax position survives review.

What the right mindset looks like

Treat the COR as part of transaction design, not post-transaction cleanup.

That means asking questions early:

- Where are strategic decisions made? If they're really made in the UAE or elsewhere, don't pretend Singapore is the centre.

- Who signs and who decides? Banks care about signatories. Tax authorities care about actual control.

- Why is Singapore in the structure? If the answer is treaty access, your operational facts need to support that answer.

The founders who get this right usually do one thing differently. They build governance around the intended tax outcome instead of hoping paperwork will fix weak facts later.

Who Qualifies for a Singapore Tax Residency Certificate

Eligibility is where theory ends. Singapore distinguishes clearly between individual tax residency and company tax residency, and the tests are not interchangeable.

Individuals qualify through physical presence

For individuals, the anchor rule is straightforward. IRAS states that a person is generally treated as tax resident if physically present in Singapore for at least 183 days in a calendar year, and that rule underpins individual COR applications for treaty claims under Singapore's tax treaties, as set out by IRAS on applying for an individual Certificate of Residence.

If you're a UAE-based founder who spends time in several countries, loose travel planning can lead to a tax problem. You can't claim Singapore individual residency by branding yourself “international”. IRAS looks at actual presence, and the day count is the foundation.

IRAS also distinguishes between foreign employees, self-employed persons, and Singapore Citizens or Permanent Residents in how COR applications are handled. That tells you something important. This is a formal process with category-specific handling, not a casual residency letter.

Companies qualify through control and management

For companies, Singapore uses a different test. Incorporation is not the decisive factor. IRAS ties company tax residency to control and management exercised in Singapore, and it gives the benchmark example that a company is a resident for YA 2025 if its control and management was exercised in Singapore throughout 2024, according to IRAS guidance on company tax residency and Certificates of Residence.

This is the rule UAE-based owners routinely underestimate.

If strategic decisions happen in Dubai, Abu Dhabi, London, or remotely by the founder while travelling, then a Singapore incorporation certificate won't rescue the tax claim. IRAS is testing where the company is directed at the strategic level.

The 2025 substance shift that many guides miss

This is where the conversation got sharper. Under updated guidance effective from calendar year 2025, foreign-owned investment holding companies seeking a COR must meet stricter substance tests. One example stated in the guidance is having at least one Singapore-based director in an executive role rather than a nominee, or at least one key employee in Singapore.

That change matters because it closes the gap between paper residency and operational reality. If your structure depends on a foreign-owned holding company in Singapore, you now need to show real local decision-making and business substance, not just formation documents and a registered address.

Practical rule: If your Singapore company has only nominee involvement, offshore decision-making, and no meaningful executive footprint in Singapore, assume the COR position is fragile.

Singapore tax residency criteria at a glance

| Criterion | Individuals | Companies |

|---|---|---|

| Core test | Physical presence in Singapore | Control and management exercised in Singapore |

| Main proof theme | Time spent in Singapore | Strategic decisions made in Singapore |

| Key practical issue | Tracking day count accurately | Documenting governance and local substance |

| UAE founder risk | Assuming travel flexibility still supports residency | Assuming incorporation alone creates residency |

| Current pressure point | Residency must align with actual presence | Foreign-owned holding structures face stricter substance expectations from 2025 |

If you compare Singapore with other jurisdictions founders consider, the same lesson keeps appearing. Rules may differ, but tax authorities increasingly ask where the core business mind sits. That's also why founders exploring a UK business for international entrepreneurs should resist copy-pasting one jurisdiction's logic into another. Residence tests are local, fact-driven, and unforgiving.

The Financial Benefits of Holding a Singapore COR

The commercial reason to get a COR is simple. It helps you defend treaty access when income crosses borders.

If your Singapore entity receives payments from abroad, foreign tax authorities or withholding agents may ask for proof that the recipient is resident in Singapore for treaty purposes. That's where the COR matters. It can support claims for reduced withholding tax rates or other relief under Singapore's tax treaties.

Cash preservation, not paperwork for its own sake

Founders often focus on gross revenue and ignore tax leakage between jurisdictions. That's a mistake. Every avoidable withholding or treaty denial reduces distributable cash, weakens reinvestment capacity, and complicates group reporting.

A properly supported COR position can help in situations involving:

- Dividends paid into a Singapore holding vehicle

- Interest income earned from overseas counterparties

- Royalties or licensing fees received by a Singapore entity

- Service income where treaty documentation affects local treatment

The value isn't just lower tax friction. It's planning certainty. Your finance team, external accountant, and banking partners can work from a cleaner file when residency evidence is already in place.

Individuals benefit too

A Singapore COR isn't only for companies. Individual entrepreneurs with cross-border income may also need it to support treaty claims. That's why the residency threshold matters so much for founders who relocate or divide their time internationally. The individual route starts from the 183-day presence rule noted by IRAS in the earlier guidance.

The signalling effect matters

There's another benefit that doesn't show up as a line item on a spreadsheet. A business with a credible Singapore residency position looks more organised to foreign banks, counterparties, and tax teams. It suggests the structure wasn't assembled casually.

That's especially relevant when the same group also uses offshore or multi-jurisdictional arrangements. If your broader structure includes international formation strategy, it helps to understand how offshore company and banking setups are typically evaluated alongside treaty eligibility, substance, and operational credibility.

The best COR outcome is often invisible. Payments flow, treaty claims hold, and no one has to scramble for missing evidence after the fact.

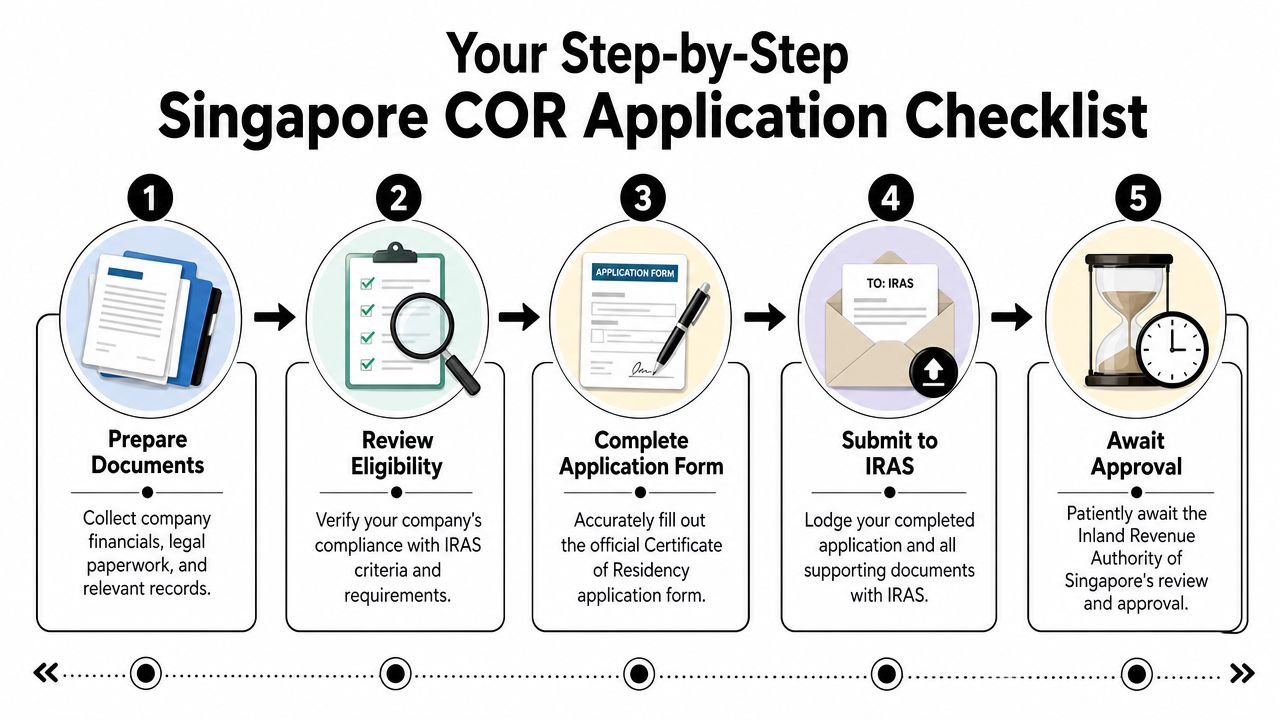

Your Step-by-Step Application Checklist

Most COR problems start before the application is filed. The form is rarely the primary issue. The facts behind it are.

For a UAE-based entrepreneur, the right approach is to build a submission file that makes IRAS comfortable with the residency claim. If you wait until a foreign payer demands a certificate, you're already late.

Step 1 Review the factual position first

Before you touch the portal, check whether the facts support the application.

For an individual, that means confirming your actual physical presence in Singapore aligns with the residency position you want to claim. For a company, it means asking where strategic decisions were made during the relevant period.

Use this pre-check:

- Match the legal story to reality. If the founder in the UAE made all strategic calls, don't pretend the Singapore board controlled the business.

- Identify the applicant category correctly. IRAS treats individuals and companies differently, and individuals also fall into different submission categories.

- Check whether the structure raises substance questions. Foreign-owned holding companies attract more scrutiny now than many legacy guides suggest.

Step 2 Assemble evidence before filing

Strong applications distinguish themselves through the evidence provided. IRAS requires documentation that fits the relevant residency test.

For individuals, prepare records that support your time in Singapore and the basis of your residency position.

For companies, the file should show that control and management sits in Singapore. That usually means practical governance evidence, not generic corporate documents.

Useful records often include:

- Board minutes showing strategic decisions made in Singapore

- Resolutions and internal approvals that reflect actual governance activity

- Director and executive details showing who holds decision-making authority

- Operational records indicating local management presence where relevant

- Supporting corporate records that align with the company's stated activities

Advisor's view: If your evidence only proves the company exists, you haven't proved tax residency.

Step 3 File carefully through the proper channel

The process is formal, and applicants should follow the relevant IRAS route for their category. The key issue here isn't speed. It's consistency.

Make sure the application details align with:

- the company's business purpose,

- the people who make decisions,

- and the jurisdiction where those decisions are made.

If the form says one thing and the documents show another, you've created your own problem.

Step 4 Prepare for the real review question

IRAS isn't only asking, “Was this company incorporated in Singapore?”

It's asking, “Why should this company be treated as resident in Singapore for treaty purposes?”

That's a deeper question. Your file should answer it without forcing the reviewer to guess.

What companies should be ready to demonstrate

A company with a stronger chance of approval usually has several of these features working together:

- Real board activity in Singapore

- Executive involvement located in Singapore

- A non-nominee decision-maker on the ground

- Records that show strategic control rather than back-office administration

This is especially important for UAE-based groups using Singapore as a holding, licensing, or treasury node. The more international the income flows, the more important your evidence trail becomes.

What individuals should avoid

Individual applicants often create issues by being careless with timeline evidence.

Watch for these mistakes:

- Relying on memory instead of records

- Confusing visa status with tax residency

- Assuming partial presence is enough without meeting the IRAS threshold

- Submitting inconsistent travel or employment information

Step 5 Keep the certificate usable

A COR is only valuable if it can be used where needed. That means thinking beyond issuance.

Check whether the foreign country, withholding agent, bank, or payer wants:

- a specific year covered,

- a direct submission format,

- or supporting documentation alongside the COR.

Don't assume one certificate solves every treaty question automatically. The foreign side may ask for additional formalities. Your job is to make the Singapore residency file sound enough that those requests don't expose weak foundations.

Common Pitfalls and How to Avoid Them

The biggest mistake is also the most common one. Founders assume a Singapore-incorporated company is automatically a Singapore tax resident.

It isn't.

IRAS treats control and management as the decisive test for company COR eligibility, and it explicitly says that foreign-owned investment holding companies, nominee companies, and non-Singapore-incorporated companies are generally not eligible under the guidance for company COR and tax reclaim matters in IRAS's corporate COR guidance for companies receiving foreign income.

Pitfall one confusing administration with control

A registered office, company secretary, filing agent, and nominee support don't amount to strategic control.

If the founder in the UAE decides investments, approves contracts, directs financing, and controls the company's major moves, then the governance centre may be outside Singapore no matter what the constitutional documents say.

Fix it by making decision-making match the intended tax position. That means real board process, real executive authority, and records created where control is said to occur.

Pitfall two using nominee arrangements as a shortcut

Foreign-owned groups frequently get into trouble. A nominee structure might satisfy a formation checklist, but it can weaken a COR case if the nominee isn't the true executive decision-maker.

The stricter substance expectations from 2025 make this even less forgiving for foreign-owned investment holding companies. If you still rely on old “light footprint” structuring logic, you're behind the curve.

Pitfall three poor board records

A founder may say the board met in Singapore. That statement is useless without evidence.

You need records that show:

- When strategic decisions were taken

- Who took them

- Where those decisions were made

- Why those decisions fit the company's business reality

Messy minutes, unsigned resolutions, and backdated paperwork are worse than thin records. They suggest the governance file was built for defence rather than created through actual management activity.

Good tax governance looks boring. That's exactly why it works.

Pitfall four building a treaty structure with no operational story

A Singapore company that exists only to receive income, with no local executive involvement and no credible decision-making footprint, invites scrutiny. That doesn't mean every company needs a large office or broad local team. It does mean the company needs a believable operating story.

For UAE-based entrepreneurs, the cleanest approach is to decide early which jurisdiction houses actual strategic control. If it's Singapore, support that with facts. If it isn't, don't force a COR strategy that your records can't defend.

Expert Guidance and FAQs

Can an individual and a company both seek a Singapore COR

Yes, but they qualify under different rules. Don't mix them. Individual residency hinges on physical presence. Company residency hinges on where control and management is exercised.

If my company is incorporated in Singapore, is that enough

No. That assumption causes more failed expectations than almost anything else in this area. Incorporation is a corporate law fact. Tax residency is a tax law conclusion.

What if another country asks for more than the Singapore COR

That happens often. A foreign payer or tax authority may want additional forms, confirmations, or supporting records. The solution isn't to panic. It's to build a strong residency file from the start so the COR sits inside a coherent evidentiary package.

Is this mainly a compliance issue or a strategy issue

It's both, but strategy comes first. A weak structure can file perfectly and still fail. A strong structure with clear governance usually has a much easier compliance path.

If your group spans the UAE and Singapore, and you want your structure to survive banking, tax, and treaty scrutiny, it helps to get a second view from advisers who understand both setup and operating reality. This kind of expert business advisory in Dubai is most useful before documents are filed, not after the foreign payer starts questioning them.

If you need help aligning your Singapore residency position with your UAE structure, Smart Classic Business Hub can help you assess substance, organise supporting records, and build a cleaner cross-border setup from day one.