Most advice on how to open an account offshore starts at the wrong point. It treats offshore banking as a box to tick, as if every UAE founder needs one the moment the company starts sending invoices abroad.

That's lazy advice.

In practice, offshore banking is a strategic tool, not a default setting. The right structure can make cross-border trade cleaner, ring-fence assets, and give you access to multi-currency operations that suit an international business. The wrong structure creates more compliance work, more questions from banks, and more friction in day-to-day operations than a good UAE banking setup ever would.

From a Dubai advisory perspective, the pattern is predictable. Businesses don't usually fail because they chose an offshore bank. They fail because they chose one before defining the purpose, the payment flows, the ownership narrative, and the compliance burden they were signing up for.

Is an Offshore Account Right for Your UAE Business

For many UAE founders, the first question isn't how to open an offshore account. It's whether offshore banking solves an actual problem or instead creates one. As Alpen Partners notes in its offshore account overview, for many UAE SMEs and founders, the key question is not how to open offshore, but whether offshore creates more friction than it removes. The same source also makes the point plainly: offshore banking isn't a tax shortcut, and onboarding can be documentation-heavy even when remote opening is possible.

That aligns with what serious applicants discover very quickly. Banks still want to understand who owns the business, what the company does, where money comes from, where it goes, and why the offshore structure exists at all.

When offshore makes sense

An offshore account can be sensible when the business case is clear and easy to defend.

Common examples include:

- International trading activity: If suppliers, customers, and settlement currencies sit across multiple countries, offshore banking can support cleaner payment routing.

- Holding foreign investments: Some founders want a separate structure for investment assets rather than mixing them with local operating cash.

- Asset segregation: A holding structure can separate ownership and operations where that separation has a genuine legal or commercial purpose.

- Cross-border treasury needs: Businesses receiving and paying in different currencies may want a banking environment built around international transfers and balance management.

If your reason fits one of those categories, you may have a case worth pursuing. If your only reason is “someone told me offshore is better”, that's not enough.

Open an account offshore only when you can explain the commercial logic in one clear paragraph. If your own explanation sounds vague, a bank will reach the same conclusion.

When a UAE bank or multi-currency setup is the better call

A local UAE operating company often needs practical banking more than exotic structuring. Payroll, rent, local supplier payments, VAT records, audit trails, and routine client receipts usually work better when the account sits close to the operating reality of the business.

A multi-currency account can also solve a large part of the problem without introducing offshore complexity. If your business mainly needs to invoice in foreign currency and make recurring international payments, a well-matched UAE banking arrangement may remove less friction overall.

That's especially true if you're still deciding on entity structure. Founders comparing offshore incorporation options should look at the practical consequences for banking, compliance, and ownership from day one, not just the formation cost. A useful starting point is this guide to UAE offshore company options.

A simple decision filter

Use this test before moving forward:

| Question | If the answer is yes | If the answer is no |

|---|---|---|

| Do you have a clear cross-border use case? | Offshore may be justified | Stay local for now |

| Can you document source of funds cleanly? | The application has a chance | Expect delays or refusal |

| Will the structure simplify operations? | Continue assessing | It may add unnecessary admin |

| Do counterparties benefit from the setup? | Offshore may support the model | It may be cosmetic only |

If offshore doesn't improve operations, control, or investment structuring in a concrete way, don't force it.

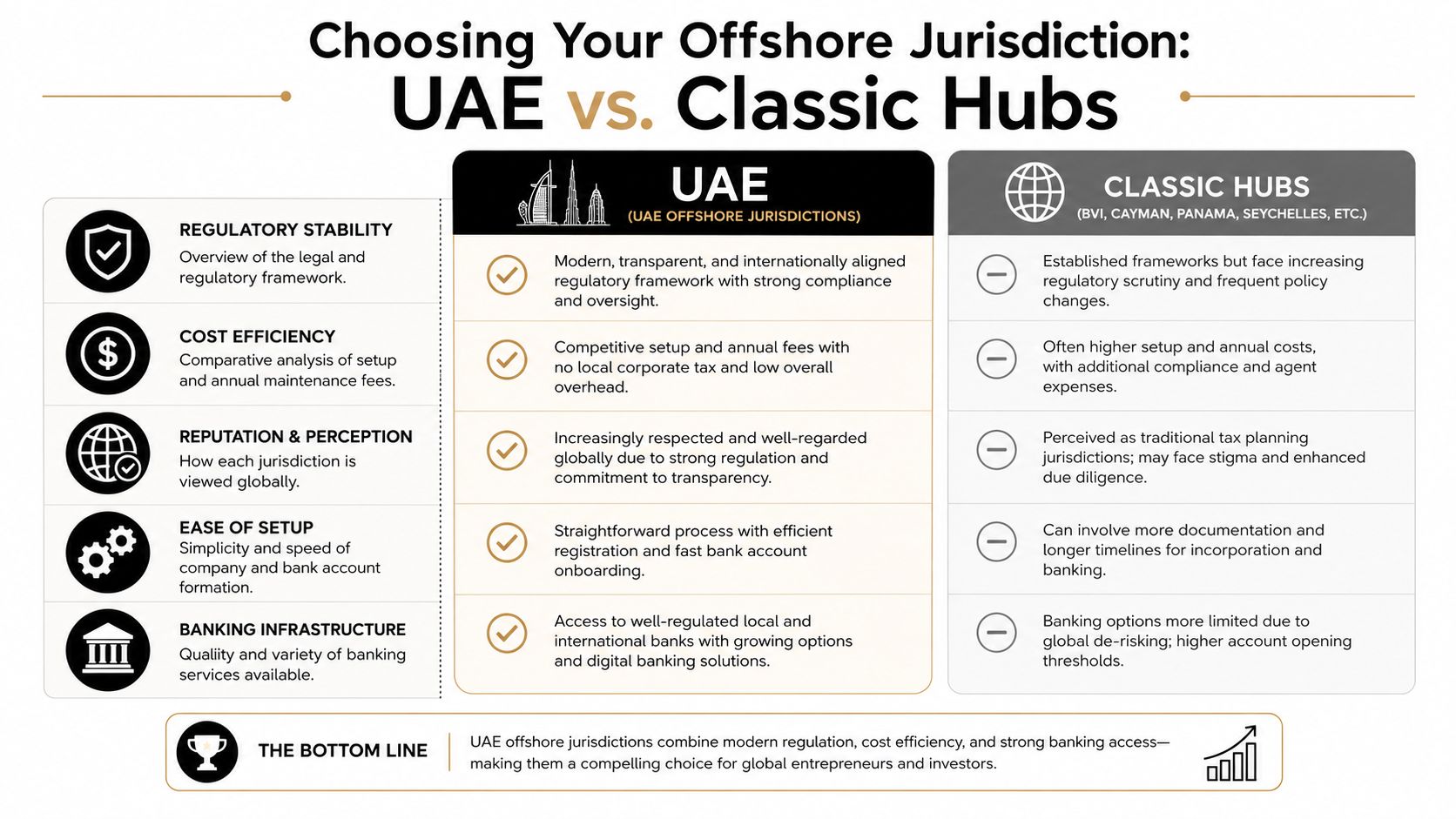

Choosing Your Offshore Jurisdiction UAE vs Classic Hubs

Jurisdiction choice isn't branding. It affects reputation, banking access, document scrutiny, and how much explanation the structure needs every time money moves.

For UAE-linked founders, the biggest practical distinction is often between a UAE-based offshore route and a classic offshore jurisdiction such as BVI, Cayman, or Seychelles. The cheapest formation option isn't always the easiest one to bank.

Why the UAE has a practical banking advantage

The UAE isn't just a place to register entities. It sits inside a large cross-border banking system. According to BIS locational banking statistics, reporting banks in the United Arab Emirates held about US$723 billion in cross-border claims by end-Q1 2024, and BIS notes that these statistics capture around 95% of cross-border banking activity. That matters because scale usually translates into deeper correspondent banking links, broader international transfer capability, and more standardised handling for internationally active clients.

For a founder trying to open an account offshore, that depth matters more than brochure language. Banks in stronger cross-border centres tend to understand regional trade flows better and handle multi-currency needs more routinely.

UAE offshore versus classic hubs

A side-by-side comparison is more useful than a long list of features.

| Factor | UAE-based offshore route | Classic offshore hub |

|---|---|---|

| Banking familiarity for UAE-connected founders | Often easier to position if business activity is tied to the Gulf | May require more explanation if operations are elsewhere |

| Perception by counterparties | Often viewed through a regional commercial lens | Depends heavily on bank and counterparty risk policy |

| Ongoing operational fit | Useful when founders, assets, or management are UAE-linked | Can work for holding or international structuring, but may feel remote from operations |

| Documentation expectations | Still strict, especially for ownership and funds trail | Also strict, sometimes with extra scrutiny due to jurisdiction profile |

| Substance and rationale | Needs a real business case | Needs a real business case, often even more clearly articulated |

What founders often get wrong

Many applicants choose jurisdiction by headline cost. Banks rarely do the same. They care more about whether the structure makes sense for the activity.

A founder living in Dubai, managing Gulf clients, signing contracts from the UAE, and receiving funds tied to regional trade often has an easier narrative with a UAE-linked setup than with a distant island company that appears disconnected from the actual business. On the other hand, if the company is a pure holding vehicle for foreign assets, a classic hub may still fit. The issue isn't fashion. It's coherence.

Practical rule: choose the jurisdiction that makes your business easier to explain to a compliance officer, not the one that sounds most “offshore”.

A working selection lens

Ask these questions before you decide:

- Where is management really happening? If decision-making sits in the UAE, that should align with the structure.

- Where are customers and suppliers based? Payment geography shapes how a bank reads the account.

- Will this jurisdiction help or complicate account opening? Company formation is easy to buy. Banking acceptance is not.

- How often will you need to defend the setup? Every transfer review, annual update, and due diligence refresh brings the same questions back.

The best jurisdiction is usually the one that supports banking, not the one that wins on setup simplicity alone.

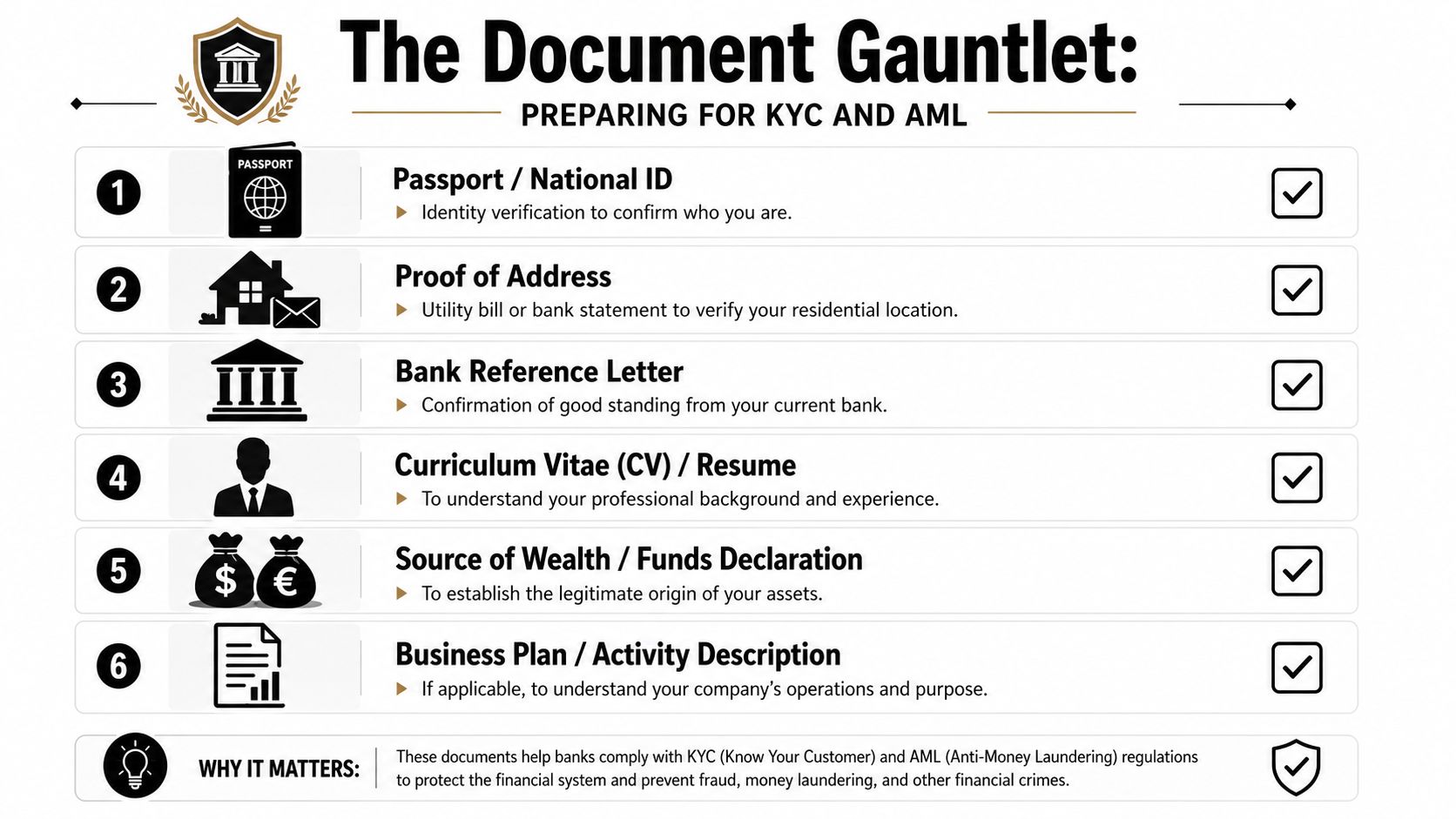

The Document Gauntlet Preparing for KYC and AML

Most offshore applications don't break at the application form. They break in the evidence pack behind it.

Banks can work with unusual ownership structures, foreign income, and multi-country activity. What they won't tolerate is a document file that looks assembled in a hurry. The most failure-prone point is source-of-funds and source-of-wealth evidence. As explained in BBCIncorp's offshore bank account guide, weak documentation is a major reason cases stall because banks want certified authenticity and a coherent transaction narrative, not just identity papers.

What the bank is actually testing

A bank's review isn't just “send passport and wait”. It is usually trying to answer four questions:

- Who are you?

- Where do you live and operate?

- How did you obtain the money?

- Why does this account make sense for your profile?

That's why the file often includes identity documents, proof of address, corporate papers, bank references, CVs, contracts, invoices, payroll records, investment records, and account statements. The bank is building a story. Your job is to make sure every document supports the same story.

The documents that usually decide the outcome

Some documents are routine. Others carry real weight.

- Passport and identification: These confirm legal identity, but by themselves they prove almost nothing about the banking case.

- Proof of address: This often fails on recency, formatting, or mismatch with other records.

- Bank reference letter: Useful when it confirms an existing, stable banking relationship.

- Corporate documents: Formation papers, ownership charts, licences, and shareholder records need to be clean and current.

- Supporting commercial evidence: Contracts, invoices, payroll records, or investment statements show how money was earned.

- Statements for the funds trail: The practical workflow described by BBCIncorp includes collecting 6–12 months of bank statements before submission, alongside notarised or apostilled identity and corporate documents.

If your statements are difficult to review because they're spread across formats, languages, or inconsistent line items, organise them before they reach the bank. Finance teams that want to standardise statement review may find ReceiptsAI's extractor comparison useful when preparing cleaner internal records for diligence.

A weak source-of-funds explanation usually isn't a fraud issue first. It's a clarity issue first. Then it becomes a risk issue.

How to build a file that survives compliance review

Use a disciplined sequence, not a generic checklist.

Pre-screen the beneficiary profile

Before submitting anything, test whether the shareholder, director, and beneficial owner profile will trigger extra questions. Industry, nationality mix, transaction corridors, and previous banking history all matter.

Map every funds path

Write out where incoming money originated, which account received it, and what document proves it. If funds came from salary, show payroll evidence. If they came from dividends, show company records. If they came from investments, show disposal or portfolio records.

Certify what needs certification

Where the bank asks for notarised or apostilled documents, don't substitute scans and hope for flexibility; doing so often leads to many files going back and forth.

Make AML logic visible

A strong file shows that the applicant understands the compliance framework they're entering. Founders who need to strengthen their controls before applying should review core anti-money laundering compliance requirements in the UAE context and align internal records accordingly.

The best submissions feel boring in the right way. Names match. Dates line up. Funds flow logically. Nothing in the file forces the bank officer to guess.

Selecting the Right Bank Criteria Beyond the Brand Name

A famous bank name doesn't guarantee a useful banking relationship. For offshore structures, the better question is whether the bank fits your transaction reality.

Many founders choose banks the way they choose hotels. They recognise the logo, assume the service will be premium, and only discover the problem once operations begin. An offshore account that can't comfortably support your payment routes, documentation cycle, or compliance profile becomes a daily constraint.

What matters more than the logo

Start with operating fit.

Risk appetite

Every bank has sectors and client types it's comfortable with. A trader moving cross-border payments between multiple jurisdictions is not the same risk profile as a holding company receiving passive income. If the bank's compliance team doesn't like your activity, no relationship manager can fix that.

Multi-currency practicality

It's not enough for a bank to say it offers multiple currencies. Ask how those balances are used in practice, what the payment workflow looks like, and how smoothly the platform handles international transfers.

Online banking quality

This is one of the most overlooked criteria. A polished front page means nothing if approvals are slow, user permissions are clumsy, and payment tracking is poor. Finance teams notice this quickly.

If the platform makes routine treasury work harder, the bank isn't a good fit, regardless of reputation.

Questions worth asking before you apply

Use direct questions. Vague conversations lead to mismatched applications.

- Which industries do you routinely bank in this segment?

- How do you assess businesses with international counterparties?

- What supporting documents do you typically request after account opening for payment reviews?

- Can the account structure support the currencies and transaction patterns we expect?

- How does the bank handle ongoing compliance refreshes?

Notice what isn't on that list. Prestige. Lounge access. Brand recognition. None of those solve operational friction.

Evaluate the adviser too

If you're using an introducer or consultant, assess them by the same standard. Do they ask sharp questions about your business model, ownership, counterparties, and source of funds, or do they offer a list of “friendly” banks?

For founders comparing practical options, this round-up of good banks for business accounts is a useful starting point because it pushes the discussion toward suitability rather than reputation alone.

The right bank is the one that can understand your business without constant defensive explanation. That's the standard.

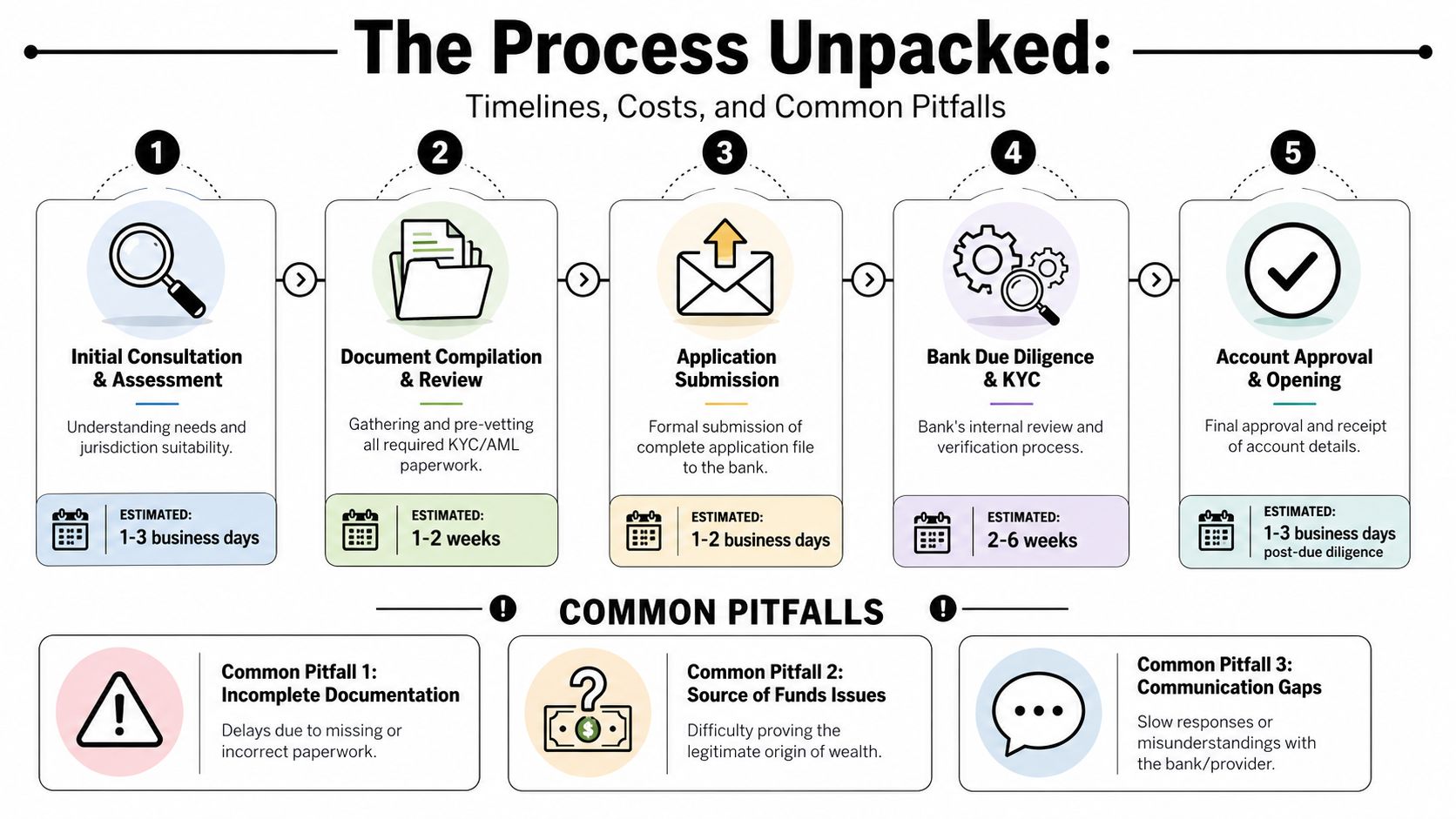

The Process Unpacked Timelines Costs and Common Pitfalls

Once the file is complete and the bank match is sensible, the process becomes much more predictable. Not effortless, but predictable.

The benchmark most applicants should work with is this: Aspire's offshore business account overview notes that the application timeline is usually 1–4 weeks once a complete file is submitted, with minimum deposits often in the USD 100–1,000 range and average-balance requirements commonly around USD 500–2,500 to avoid fees. The same source notes that delays often come from incomplete KYC, inconsistent business-plan details, or failure to meet ongoing balance conditions.

How the process usually works

The order matters.

Assessment and bank matching

The application's success or failure is often determined prior to submission. The business purpose, ownership, payment corridors, and document strength should all be tested before submission.

File preparation

A complete file means more than “all requested documents attached”. It means the documents are consistent, current, and aligned with the narrative the bank will read.

Formal submission

Once submitted, the bank's review tends to focus on identity, ownership, source of funds, intended activity, and account usage. Questions at this stage are normal. Contradictions are not.

Approval and funding

Only fund the account after approval steps are clearly confirmed. Sending money too early or assuming the relationship is active before all conditions are met creates needless confusion.

What often goes wrong

The most common problems are boring. That's why they're expensive.

- Incomplete KYC files: Missing proofs, expired documents, unclear scans, or inconsistent address records.

- Weak business logic: The company says one thing in its application and another in its supporting material.

- Mismatch between bank and activity: The applicant may be legitimate, but the bank doesn't like the transaction pattern.

- Ignoring balance conditions: Some applicants focus on approval and overlook ongoing requirements tied to fees or account maintenance.

A practical pre-mortem

Before filing, ask what the bank is most likely to question.

| Potential issue | What the bank may think | What to fix before submission |

|---|---|---|

| Vague business purpose | “Why does this company need this account?” | Tighten the commercial rationale |

| Unclear source of funds | “We can't trace the money properly” | Add stronger supporting records |

| Conflicting activity descriptions | “The file doesn't tell one consistent story” | Align forms, licences, and narrative |

| Underestimated account conditions | “The client may not maintain this relationship properly” | Confirm deposit and balance expectations |

Slow responses during due diligence can damage a good application. Banks often interpret delay as uncertainty, not busyness.

A realistic applicant plans for document follow-up, clarifications, and occasional requests for extra evidence. A careless one assumes submission equals approval. That assumption causes more delays than the form itself.

Conclusion Partnering for a Smooth Offshore Setup

Opening an account offshore isn't difficult because the forms are mysterious. It's difficult because every decision connects to another one. Jurisdiction affects banking. Banking affects documentation. Documentation affects timing. Timing affects whether the account opens smoothly or turns into a long cycle of compliance queries.

The founders who handle this well usually do four things right. They confirm offshore is necessary. They choose a jurisdiction that supports the banking story. They prepare the source-of-funds file properly. And they select a bank based on operational fit, not image.

What a smoother process looks like

A good offshore setup process is organised before the first submission.

That means:

- The rationale is clear: The account has a real commercial purpose.

- The structure is coherent: Ownership, management, and transaction flow make sense together.

- The documents are prepared properly: Nothing important is missing, vague, or inconsistent.

- The bank choice is disciplined: The institution suits the activity, not just the aspiration.

When those points are handled early, the process becomes more administrative than dramatic.

Where experienced support matters

Advisers can reduce avoidable friction. A consultant should challenge weak logic, identify documentary gaps, and pressure-test the account strategy before the bank does. That is much more useful than forwarding forms.

In practical terms, firms such as Smart Classic Business Hub help founders align company structure, compliance preparation, and bank account strategy in one workflow instead of treating them as separate tasks. That's often the difference between a clean submission and an application that keeps returning for clarification.

The right support doesn't “guarantee” approval, and anyone implying that should be treated cautiously. What it can do is improve fit, reduce rework, and make sure the file presented to the bank is credible from the start.

If you're planning to open an account offshore from the UAE, treat it as a business decision first and a banking exercise second. That order saves time.

If you want a practical review of your structure, documents, and banking options before you apply, speak with Smart Classic Business Hub. Their Dubai-based team supports UAE company formation, offshore structuring, compliance preparation, and bank account coordination so you can move forward with a cleaner, better-prepared application.