You've registered a company in Dubai, or you're about to. The licence is moving, the visa file is in progress, the landlord wants a deposit, and your first supplier is asking when funds will hit the UAE account. Then the practical question lands: how do you move money from India to the UAE without triggering delays, compliance flags, or a rejected transfer?

That's where many founders get stuck. The corridor is active, familiar, and heavily used, but that doesn't make it casual. A transfer for family support is treated very differently from a transfer that funds a new UAE company, and the mistake I see most often is assuming both follow the same path.

Sending Money From India to the UAE An Introduction

An Indian entrepreneur sending start-up capital to Dubai usually isn't struggling with intent. The main friction is execution. The sender knows why the money is moving, but the bank or remittance provider wants that purpose translated into the right category, backed by the right beneficiary details, and submitted through the right channel.

That matters because the India-UAE money movement route is not niche. The UAE is the second-largest remittance source to India, accounting for 18% of remittances sent, and in 2022, exchange houses in the UAE routed 50% of the country's outward remittances, equal to US$39.7 billion (AED 145.7 billion), to India, Pakistan, and the Philippines, according to this UAE remittances market overview. High volume doesn't mean low scrutiny. It means the channel is established and regulated.

For someone searching how to transfer cash from India to UAE, the word “cash” can be misleading. In practice, compliant transfers usually end in a bank credit through formal rails. You may fund the transfer through a branch deposit or another approved method, but the transaction still has to pass through a bank, licensed money changer, or regulated platform.

Practical rule: If the money is intended for a Dubai business, treat the transfer as a compliance event, not just a payment.

The founders who move funds smoothly usually do three things early. They confirm the transfer purpose, they collect exact beneficiary banking details, and they compare providers based on total landed value rather than the advertised fee alone. If you're trying to sharpen that side of your process, this guide on optimizing international payments is a useful companion because it frames transfers as an operational decision, not just a treasury task.

The rest is straightforward once the pieces are in the right order. The route exists, the providers exist, and the process works. What causes trouble is usually not the transfer itself. It's the mismatch between the sender's purpose and the path they chose.

Navigating Indian Regulations for UAE Transfers

Before you compare apps, banks, or exchange houses, you need to understand the Indian side of the transaction. That's where the main gatekeeping happens. If the transfer doesn't fit the permitted route, no provider comparison will save it.

The limit that shapes most retail transfers

For resident individuals, India's Liberalised Remittance Scheme caps outward remittances at US$250,000 per financial year, and a major Indian bank notes that online or mobile-app transfers to the Middle East generally cannot exceed US$25,000 per transaction. The same guidance says the recipient bank's SWIFT code is required for UAE transfers, as set out in Axis Bank's guidance on sending money to the Middle East.

That gives you two practical constraints immediately.

- Annual cap matters: If you're funding a business personally from India, your room under LRS matters more than your appetite to send.

- Per-transfer cap matters online: A larger transfer may need to be split operationally or handled through a branch-based process, depending on the provider.

- SWIFT details aren't optional: A UAE transfer can stall before it starts if the SWIFT code is wrong or incomplete.

The question isn't only “Can I send this amount?” It's also “Can I send it through this channel for this stated purpose?”

Why banks ask for so much paperwork

Founders often get irritated by KYC, PAN checks, and purpose coding. That reaction is understandable, but it misses the point. The bank isn't just moving money. It is documenting why funds are leaving India, who is receiving them, and whether the transfer sits inside the permitted framework.

A personal support transfer usually moves through a cleaner path. A business-linked transfer can invite closer review because the bank will want clarity on source of funds, beneficiary identity, and the commercial reason for remittance. That's also why firms operating in the UAE need a working grasp of local controls such as anti-money laundering compliance in the UAE. The sending side and receiving side aren't separate worlds. They meet at compliance.

Banks rarely reject a transfer because the customer wanted to send money. They reject or delay it because the file doesn't tell a coherent story.

What to prepare before you initiate anything

Don't wait for the provider to ask. Have your documentation lined up before you start.

- Identity records: Keep your PAN, KYC records, and any provider-specific profile information updated.

- Beneficiary banking information: Match the recipient name to the UAE bank records exactly and verify the account number and SWIFT code directly from the beneficiary.

- Purpose support: If the transfer is business-related, expect to justify the purpose more clearly than you would for family support.

- Funding trail: Make sure the source of funds is easy to explain and consistent with the transfer purpose.

Business owners with US connections or cross-border tax exposure also tend to underestimate how tax reporting can interact with money movement. If that applies to your structure, a practical primer on managing IRS obligations can help you think through reporting issues before funds start moving across multiple jurisdictions.

What works and what does not

What works is simple. A clear purpose, complete beneficiary details, and a transfer amount that fits the chosen channel.

What doesn't work is trying to make a business capital transfer look like a generic personal remittance just because the online form is easier. That may feel convenient at the start, but it often creates a bigger problem later when the UAE bank, auditor, or licensing authority asks what the incoming funds were.

Comparing Your Transfer Options and Costs

If the paperwork is in order, the next decision is the rail. Provider comparisons are often approached ineffectually. The headline fee frequently receives initial attention, and the evaluation concludes there. For India-UAE transfers, that's often the least useful number on the screen.

The hidden cost sits in the rate

BookMyForex publicly lists a transfer fee of Rs225 plus GST for India-to-UAE wire transfers, and the same public guidance makes the key point that the actual cost is provider-dependent because the exchange-rate spread can matter more than the visible fee. It also notes that reliable providers issue a tracking reference such as a SWIFT copy or MTCN, as shown in BookMyForex's page on sending money to the UAE.

That means you shouldn't ask, “What's your fee?” and stop there.

Ask instead:

- What all-in INR-per-AED rate am I getting?

- Is this bank-to-bank SWIFT, or another settlement method?

- Will I receive a tracking reference after payment?

- What extra documentation applies if the transfer is for business use?

A low fee with a poor FX rate can still be an expensive transfer.

India to UAE money transfer methods compared

| Method | Typical Speed | Cost Structure | Best For |

|---|---|---|---|

| Bank wire via SWIFT | Usually slower than simplified retail flows, especially if compliance review is involved | Visible transfer fee plus FX spread, and sometimes intermediary effects on final credit | Business funding, formal account credits, higher-documentation cases |

| Online remittance platform | Often more convenient at the front end | Platform fee, FX spread, and channel-specific limits | Routine personal transfers and straightforward bank credits |

| Licensed exchange house or money transfer operator | Can be efficient for standard corridors | Fee plus conversion margin, with provider-specific collection and settlement options | Senders who want branch support or an established remittance operator |

This table avoids fake precision for speed because actual timing varies by provider, review level, and banking cut-off. In practice, the right method is less about “fastest” and more about “least likely to bounce back for your specific purpose.”

How banks compare with remittance platforms

A traditional bank wire is still the cleaner path for many business-related transfers. It gives you a formal trail, clearer alignment with bank account credits, and better documentation for later reconciliation. The trade-off is friction. Banks ask more questions, and they should.

Online remittance platforms are easier to initiate. For personal transfers, that convenience is real. For business transfers, the issue isn't whether the app works. The issue is whether the app's workflow accommodates your actual purpose and required documentation.

Licensed exchange houses and established money transfer operators sit somewhere in the middle. They can be useful when the sender wants branch assistance or a familiar remittance process, but you still need to confirm the end credit method and compliance requirements before assuming it's suitable for company funding.

A practical selection framework

Use this filter before picking a provider:

- If the transfer funds a UAE company: Lean towards a path that creates a formal banking trail and supports purpose-based documentation.

- If the beneficiary is an individual: Convenience may matter more, provided the details are exact and the purpose is straightforward.

- If the amount is sensitive to FX: Compare the all-in converted result, not just the fee displayed on the first page.

- If reconciliation matters later: Prioritise a provider that gives you documentary evidence of the transfer.

For founders operating across several jurisdictions, it also helps to see how providers position themselves in other regulated markets. This overview of money transfer services in Canada is useful not because Canada and the UAE are identical, but because it trains you to compare rails, user experience, and hidden pricing instead of relying on one advertised fee.

One final point. Don't confuse “cash transfer” with “informal transfer.” The method that works best is usually the one that leaves the cleanest compliance trail. For a business owner, that trail often matters more than a marginal difference in convenience.

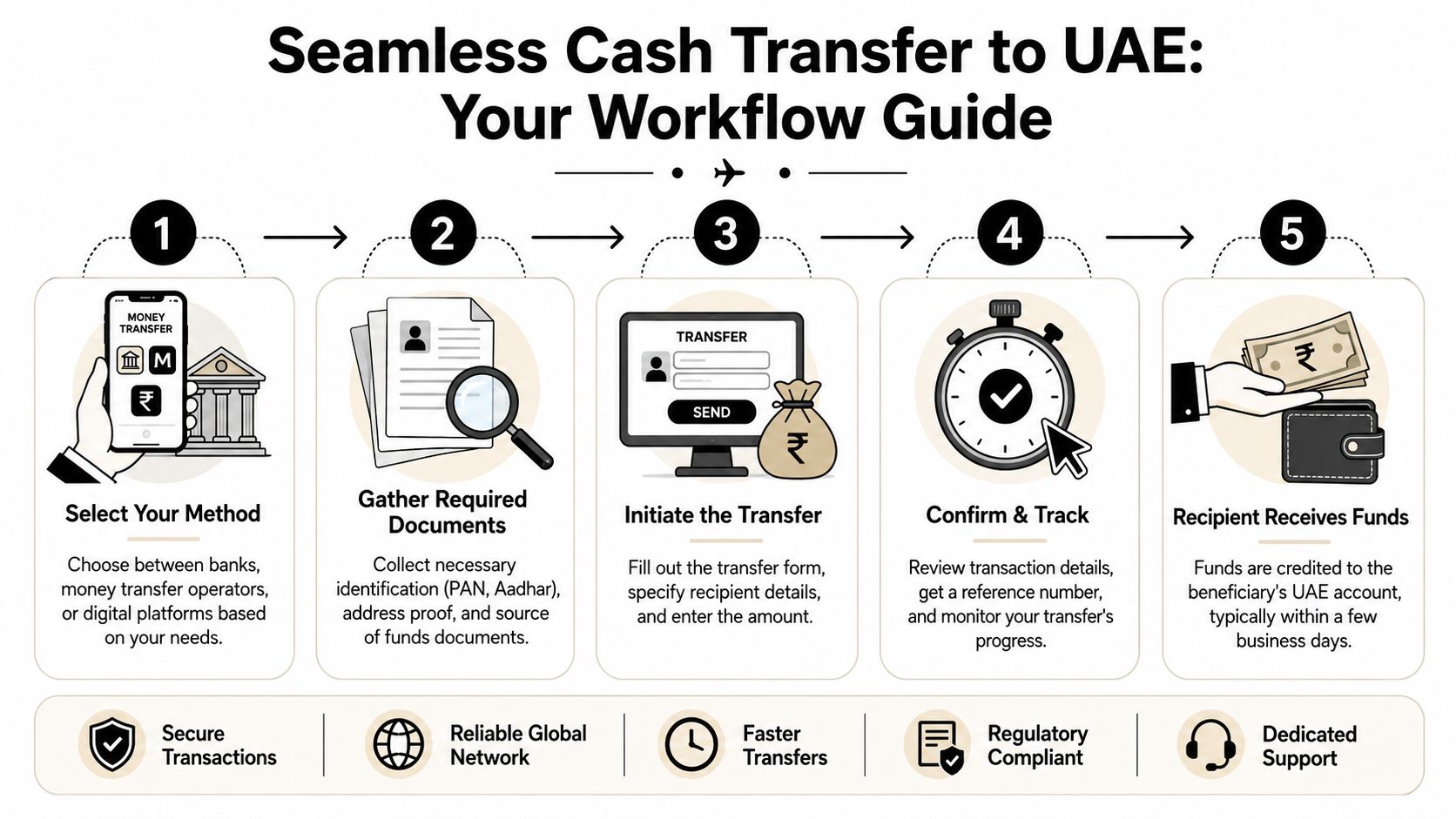

Executing Your Transfer A Step-by-Step Workflow

Individuals looking to transfer cash from India to UAE usually want a sequence they can follow without missing a hidden requirement. The operational flow is simple. The discipline is what matters.

Start with beneficiary data, not the amount

The first thing to lock down is the recipient record. A compliant outward remittance requires the sender to initiate the transfer, enter the beneficiary's full bank details including the SWIFT code, and complete LRS and KYC documentation. Guidance from IndusInd's forex resource also notes that common failures include the wrong SWIFT code, incomplete beneficiary data, or missing purpose-of-remittance documents, all of which can delay or block the transfer, as outlined in this India to UAE transfer workflow guide.

That means your checklist starts here:

- Beneficiary legal name: It must match the UAE bank record exactly.

- Account number: Reconfirm it from a bank document or official bank-generated instruction.

- SWIFT code: Don't copy this from an old chat message unless the beneficiary has verified it.

- Purpose of remittance: Decide this before opening the transfer form.

- Sender KYC profile: Make sure your provider account is current before the transaction day.

If the receiving account is newly opened in Dubai, make sure the account is ready to receive inward funds and the banking details are formally issued. Founders who are still at the account-opening stage often benefit from understanding the basics of a non-resident bank account in Dubai before attempting the first transfer.

Choose the initiation path that matches the purpose

There are two broad execution paths in real life.

A digital path works when the provider supports your amount, your purpose, and your documentation profile. You enter the beneficiary details, complete the declarations, fund the transfer through the provider's accepted method, and wait for confirmation.

A branch-led path is often better when the purpose is more sensitive, the supporting documents need review, or the provider's digital workflow doesn't clearly fit the remittance category. This route takes longer at the front end, but it can save time overall because the file is assessed more carefully before funds move.

If you're unsure whether a transfer belongs online or at a branch, that uncertainty is itself a sign to pause and clarify the purpose first.

Funding and tracking the transfer

Once the instructions are accepted, the sender funds the transaction through the provider's allowed method. Different providers support different funding rails, including net banking, debit card, UPI, or branch cash deposit depending on the setup and the provider's process. After payment, retain every confirmation generated by the provider.

Keep these records together:

- Transfer receipt or provider confirmation

- Tracking reference, such as a SWIFT copy or similar reference

- Purpose declaration

- Any supporting document submitted during the process

This is not admin for its own sake. If the beneficiary says the money hasn't arrived, those records are what let you escalate intelligently instead of guessing.

The small mistakes that cause large delays

Most failed transfers don't fail for dramatic reasons. They fail because one field was wrong, one name didn't match, or one document was missing.

The errors I see repeatedly are predictable:

Name mismatch

The sender uses a trading name, nickname, or shortened form instead of the beneficiary's bank-registered name.Wrong SWIFT code

The bank name may be right, but the branch routing detail is not.Unclear purpose

The sender selects a general category online while the transaction relates to business formation or investment.Missing support

The provider or branch asks for extra evidence, and the sender only starts collecting it after the transfer is already in motion.

The cleanest workflow is boring. Verify, submit, fund, track, reconcile. That's exactly why it works.

Special Considerations for Business and Investment Transfers

Generic remittance advice usually proves inadequate. Sending money to a relative and sending money to capitalise a UAE business are not the same exercise. The payment rail may look similar on the surface, but the compliance logic is different.

Purpose changes the path

Western Union's India-to-UAE guidance makes the core point clearly: the purpose of the remittance significantly changes the compliance path, and a transfer for business investment may trigger a request for additional supporting documents at a bank branch, unlike a simpler online transfer for family support. That distinction is especially important for founders funding a new UAE company, as reflected in Western Union's page on sending money to the UAE.

For a business owner, the phrase “purpose of remittance” is not a box to click through quickly. It drives what the bank expects next.

A business investment transfer should look like a business investment transfer in both the paperwork and the transaction trail.

What banks and providers may want to see

The exact list depends on the provider and the structure of the transaction, but business-related remittances often need stronger support than personal transfers. In practice, founders should be ready with documents that establish the receiving entity, the relationship to that entity, and the reason the funds are being sent.

That commonly means preparing items such as:

- Company formation records: The UAE entity's incorporation or registration documents, where available.

- Constitutional documents: Materials such as a memorandum or equivalent company documents if the provider requests them.

- Shareholding context: Evidence showing why the sender is funding that business.

- Purpose narrative: A concise explanation that aligns the payment with business setup, capital contribution, or another legitimate commercial use.

If the receiving structure is offshore or part of a wider asset-holding arrangement, the banking treatment can become more document-heavy. In that scenario, it helps to understand the realities of a UAE offshore bank account before choosing the transfer route.

What founders often get wrong

The biggest error is trying to force a company funding transfer into the same workflow used for a routine remittance. That can create trouble later when the receiving bank asks what the funds represent or when your finance team needs a clean audit trail.

The second mistake is sending funds before the beneficiary account setup is fully coherent. If the company account isn't ready, or if the beneficiary name still reflects an earlier draft of the entity records, even a correctly sent transfer can become painful to reconcile.

Business remittances need consistency across four points:

- Sender identity

- Declared purpose

- UAE beneficiary record

- Supporting documents

When those four align, banks usually have a clear basis to process the transfer. When they don't, the transaction can drift into manual review. For a founder trying to launch quickly, that delay is expensive in all the ways that don't show up on a transfer receipt.

Troubleshooting and Expert Transfer Tips

If a transfer is delayed, start with the basics before escalating. Check whether the beneficiary name, account number, and SWIFT details match the bank record exactly. Then pull the transfer reference and ask the provider where the payment currently sits in the chain. Vague follow-up wastes time. A specific query tied to the reference gets better answers.

If a transfer is rejected, don't resend immediately with the same details and hope for a different outcome. Find out whether the issue was beneficiary data, purpose coding, or missing documentation. Repeating the same mistake can make the next review stricter.

The practical habits that save trouble

- Compare total conversion outcome: Don't choose a provider on fee alone. The landed AED amount matters more.

- Use the right rail for the purpose: A business remittance often deserves a more formal route even if another option looks easier.

- Keep a clean file: Save receipts, references, and purpose documents in one place from the start.

- Coordinate with the UAE side: The beneficiary should know the transfer is coming and be ready to answer any receiving-bank query.

A question that comes up often is whether multiple people can support a business funding requirement. The answer depends on how the transaction is structured, who the senders are, and how the funds will be reflected on the UAE side. That's where casual advice becomes risky. If more than one director, shareholder, or family member is involved, get the structure clear before money moves.

The same applies if you're thinking ahead to tax residency, profit repatriation, or treaty use. A transfer itself doesn't solve those issues. It only creates the funding trail. The legal and tax position still needs to match the commercial reality.

If you're transferring funds from India to support a UAE business setup, banking structure, or compliance-sensitive investment, Smart Classic Business Hub can help you align the transfer purpose, company documents, and UAE-side requirements before the payment runs into avoidable delays. That's often the difference between a clean launch and a week lost in bank queries.