You've got the trade licence. The company name is approved. The setup agent has handed over a neat folder of documents. At that point, most founders assume the hard part is done.

Then the bank asks questions you weren't prepared for.

Not just your passport and licence. They want to know what the business does, how money will move, who the owners are, where the funds come from, and whether your declared activity matches your operations. For a foreign investor, especially one without UAE residency, that's where the smooth launch often turns into delays, rejections, and repeated applications.

A UAE corporate account is not a routine admin step. It's a risk review. If you understand that early, the process becomes far easier to manage. If you treat it like a form-filling exercise, you can lose weeks.

Why Opening a UAE Business Bank Account Can Be a Challenge

A common pattern looks like this. A founder sets up a Free Zone company for consulting, software, trading, or e-commerce, then walks into a bank expecting a straightforward account opening. The bank officer takes the file, asks a few polite questions, and then silence follows. Later, more documents are requested. Then a business plan. Then proof of contracts. Then clarification on shareholder residence, source of funds, and expected counterparties.

That doesn't happen because the bank is being difficult for no reason. It happens because UAE banks assess structure, substance, and risk before they onboard a company.

What banks are really reviewing

Banks usually look beyond the trade licence itself. They want to understand:

- Who owns the company: Directors, shareholders, and ultimate beneficial owners must be easy to identify.

- Where the business will operate: Mainland, Free Zone, and offshore structures don't get treated the same way.

- How credible the activity is: A vague description such as “general trading” or “consultancy” without detail often creates friction.

- Whether the founder is resident or non-resident: That changes the level of scrutiny.

A practical way to think about the process is this. Your company file has to make sense to a compliance team that doesn't know you and isn't interested in optimism. They're looking for consistency.

Practical rule: A bank approves clarity faster than ambition. A modest, well-documented business model is usually easier to bank than a broad, loosely explained one.

Foreign founders often underestimate the financial side too. Banking decisions affect working capital, timelines, and operating flexibility, which is why many businesses treat account opening as part of broader corporate financial risk mitigation, not as a back-office formality.

Why foreign investors feel the pressure more

For overseas shareholders, the challenge is sharper because the bank can't rely on local history. If you don't have a UAE visa, Emirates ID, local address trail, or established operating footprint, the bank has less comfort and asks for more evidence.

That's the key starting point for a successful business bank account in the UAE. Not the application form. The quality of the story your documents tell.

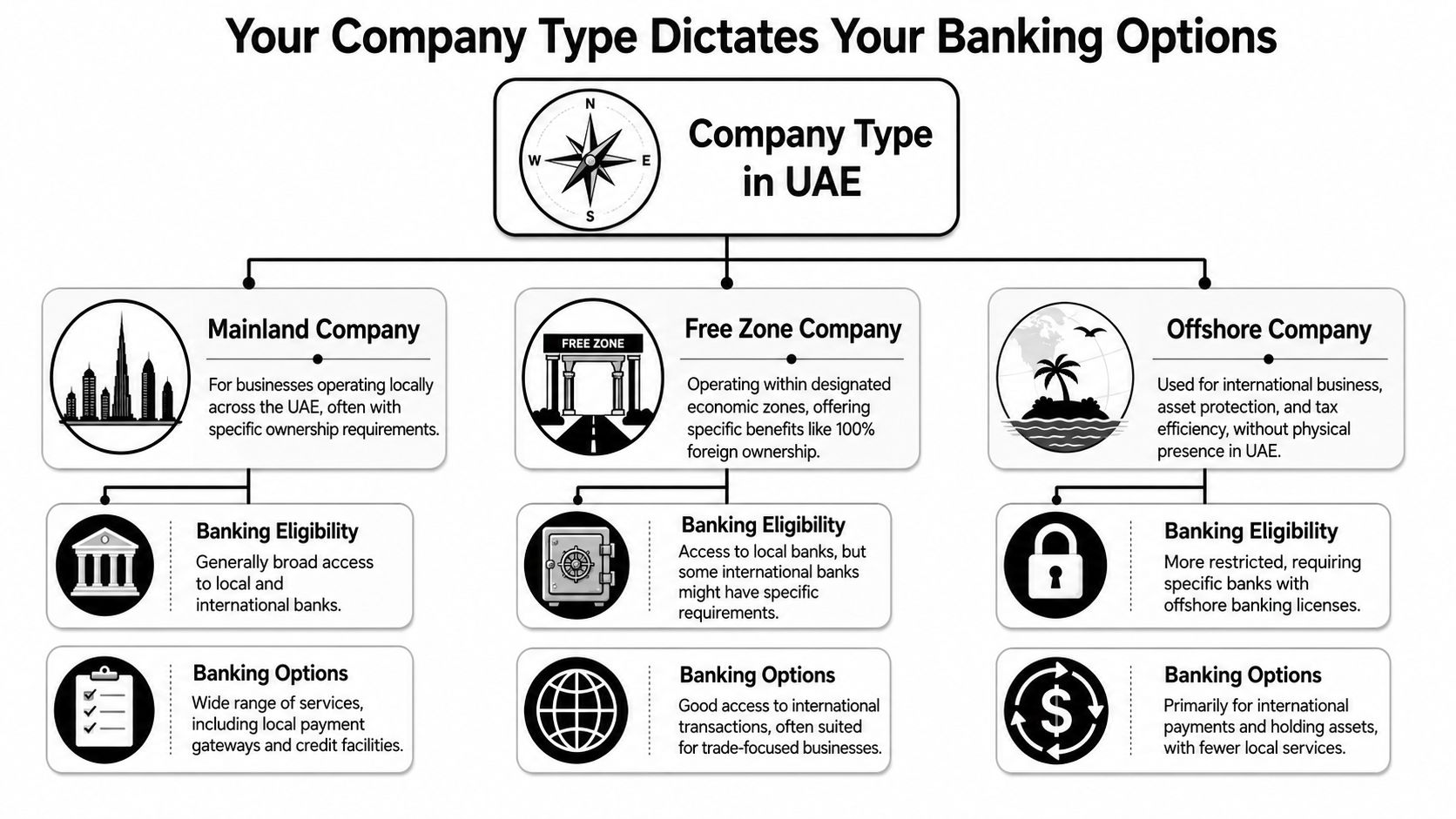

Your Company Type Dictates Your Banking Options

The legal structure you choose doesn't just affect licensing and operations. It shapes how a bank reads your file from day one.

Some founders shortlist banks first and only later realise their company type already narrowed their options. That's backwards. Start with how the bank will classify your entity, then choose where to apply.

Mainland companies

A Mainland company is usually the easiest structure to explain to a bank if the business will serve the UAE market directly. Banks tend to understand the commercial logic more quickly because the company sits clearly within the domestic economy.

That doesn't mean approval is automatic. It means the operating case is often easier to present when you have a physical presence, local contracts, staff plans, or customers inside the UAE.

Mainland structures tend to work well for businesses that need:

- Local trading flexibility: You're dealing directly with the UAE market.

- Operational substance: Office lease, employees, and local invoicing strengthen the file.

- Broader service access: Payment collection and local banking tools are generally easier to justify.

Free Zone companies

Free Zone entities are common with foreign founders, and for good reason. They can be efficient, flexible, and well suited to service businesses, cross-border trade, and holding structures. But banks don't treat all Free Zones equally, and they don't treat all Free Zone activities equally either.

A Free Zone company can be perfectly bankable. The issue is whether the bank can quickly understand why the company exists, where it will transact, and why that particular setup was chosen.

Watch for these pressure points:

- Business activity clarity: If the licence is broad but the actual model is narrow, explain the narrow model clearly.

- Economic logic: A software consultancy, import-export trader, and IP holding company won't be assessed the same way.

- Supporting evidence: Contracts, invoices, and a coherent profile matter more than founders expect.

Some foreign investors, especially those structuring assets or international holdings, also look for specialist reading before picking a zone. If that's your situation, this overview on guidance for HNWIs on Dubai Freezones is useful background on how structure affects wider planning.

Offshore companies

Offshore companies create the most confusion. Many founders assume offshore means easy international banking. In practice, it often means the opposite if you're seeking an operational onshore business account in the UAE.

Banks usually see offshore entities as limited-purpose vehicles unless the structure is documented very carefully. They may be suitable for holdings, asset ownership, or international structuring, but they are often less suitable for day-to-day UAE operating activity.

A quick rule of thumb:

| Company type | How banks usually view it | Common banking fit |

|---|---|---|

| Mainland | Local operating business | Strong fit for active UAE operations |

| Free Zone | Flexible commercial vehicle | Good fit when activity is specific and documented |

| Offshore | Special-purpose or holding structure | More restricted for routine operational banking |

If you're weighing that route specifically, this guide on opening an offshore company and bank account helps frame the practical implications before you apply.

Banks don't bank legal forms. They bank business logic. If the structure and the activity don't fit naturally, the file becomes harder immediately.

The Essential Document Checklist for Your Application

A founder can submit every standard company paper and still get stuck in review for weeks. I see this often with foreign investors who assume the checklist is the job. It is not. The bank is trying to understand whether the licensed activity, the expected transactions, and the shareholder profile make sense together.

That is why technically complete files still fail.

Core company documents

Banks will ask for the basic legal pack first. Prepare clean, readable copies and make sure names, dates, and activities match across all documents.

- Trade licence: The licensed activity must align with what you plan to do through the account.

- Incorporation and constitutional documents: Usually the Certificate of Incorporation, Memorandum of Association, Articles of Association, or the free zone equivalent.

- Passport and ID documents for shareholders and directors: Visa, Emirates ID, and proof of address may also be requested, depending on residency status.

- Office lease or address evidence: A tenancy contract, Ejari where applicable, or approved business address document helps show operating presence.

- Share register or ownership chart: This matters more when there are multiple shareholders, a holding company, or an overseas parent.

This part proves the company exists. It does not yet prove the business makes sense to the bank.

The documents that decide whether the file feels credible

Many applications tend to weaken at this stage, especially for non-resident owners and newly formed companies.

Banks want to see how money will move, who the counterparties are, and why this UAE entity should handle that activity. If the licence says “general trading” but the file describes software consulting, or if the shareholder says the company will serve GCC clients but all projected payments are from unrelated high-risk jurisdictions, the bank will slow the file down or decline it.

Include these documents from the start:

- Business summary or business plan: Keep it practical. Explain the service or product, target customers, supplier base, countries involved, and why the UAE company is being used.

- Expected transaction profile: State estimated monthly volume, average ticket size, key currencies, sending and receiving countries, and whether cash, cheques, or only transfers will be used.

- Source of funds evidence: Show where startup capital and opening deposits come from, such as personal savings, business income, sale proceeds, or group-company support.

- Proof of actual or pending activity: Signed contracts, invoices, purchase orders, LOIs, supplier correspondence, client emails, and a company website all help.

- Existing banking history, if available: Prior business bank statements or a bank reference can help if the shareholders already run an operating business elsewhere.

One practical point matters here. Remote onboarding is not a substitute for a weak file. Some founders hear that a bank allows part of the process online and assume that means lighter scrutiny. In practice, remote steps help with convenience, but compliance still wants the same commercial logic and may ask for a meeting, clarifications, or extra support before approval.

Build the file around the questions compliance actually asks

A useful application pack should answer five points clearly:

- What does the company do in plain English?

- Who will pay the company?

- Who will the company pay?

- Where does the money come from?

- Why does this transaction flow fit the licensed UAE activity?

If those answers are scattered across emails and attachments, the file becomes harder to approve. A short cover note tying the documents together often helps more than another stack of certificates.

I also advise founders to prepare one page on the shareholder story. Banks are often more comfortable when they can see the investor's background, existing business interests, and reason for setting up in the UAE. This matters even more if the company is new and has no local revenue yet.

Banks do not reject papers only because something is missing. They reject files when the activity, transaction pattern, and ownership story do not line up cleanly.

For founders comparing practical setup routes in Ras Al Khaimah, this guide to a RAK business account is a useful reference. If your group also needs cross-border support beyond basic account opening, outside providers of financial services solutions can help structure the wider picture before you submit the file.

How to Choose the Right UAE Bank for Your Business

There is no single best bank for every foreign investor. There is only the bank type that best fits your structure, transaction profile, and onboarding reality.

That distinction matters. Founders often choose based on brand recognition, then discover the bank's risk appetite, minimum balance, or onboarding method doesn't match the business.

The three bank categories that matter

In practice, most new businesses compare three groups.

Traditional UAE banks are often the first option founders think of. They usually suit businesses that need local credibility, a broader branch network, and potentially more mature cash-management capabilities. They can also be more conservative in onboarding, especially for non-resident shareholders or unusual business models.

Digital-first banks appeal to founders who want speed, cleaner interfaces, and less branch dependency. They may work well for certain startup profiles, but founders should not assume “digital” means universally easy. Eligibility can still depend on nationality, structure, activity, and compliance comfort.

International bank branches can be relevant for companies with cross-border owners, overseas group structures, or international trade patterns. But they may also be selective, particularly if the UAE entity is new and has limited local operating history.

Minimum balance is not a side issue

A business bank account in the UAE often comes with a capital commitment that founders don't budget for properly. According to Middle East Briefing's guide to opening a bank account in the UAE, corporate accounts typically require a minimum balance ranging from AED 50,000 to AED 500,000, with many banks setting thresholds between AED 25,000 and AED 150,000. The same source notes that this barrier is usually higher for non-resident founders without a UAE visa or Emirates ID.

That changes the decision completely for lean startups. A bank that looks prestigious on paper may be the wrong fit if it locks up too much liquidity or imposes penalties when the balance drops.

Remote opening is not as simple as adverts suggest

This is one of the most misunderstood parts of the process. Some banks market digital onboarding, but that doesn't always mean a foreign shareholder can complete everything remotely.

As noted in this LinkedIn analysis of non-resident shareholder account opening in the UAE, the average timeline for non-resident opening is 3 to 6 weeks, many UAE banks still require at least one physical visit for verification or signature, and only a limited number of digital banks, including Wio and Mashreq NeoBiz, may support fully remote access depending on profile and nationality. That same review highlights the challenge of navigating 60+ licensed institutions without an up-to-date shortlist.

If remote onboarding is essential, verify the exact step that must be done in person. Founders often learn too late that “online application” is not the same as “fully remote account opening”.

Comparing UAE bank types for new businesses

| Bank Type | Best For | Typical Min. Balance | Remote Opening? | Key Feature |

|---|---|---|---|---|

| Traditional UAE bank | Companies with local operations and straightforward activity | Often within the ranges noted above, depending on bank and profile | Sometimes partly digital, often with in-person verification | Wider local banking ecosystem |

| Digital-first bank | Startups and founders who want a simpler interface and faster handling | Varies by profile and product | Possible in some cases, but not universal | Streamlined user experience |

| International bank branch | Cross-border groups and internationally structured businesses | Often profile-dependent | Usually selective and not always fully remote | Familiarity with international ownership structures |

How to shortlist properly

Don't apply randomly. Match the bank to the business.

Use these filters:

- Residency status: Non-resident founders should ask about this before preparing the full file.

- Licensed activity: Some banks are far more comfortable with service firms than with trading models, and vice versa.

- Transaction geography: If most payments are international, ask about currency handling and cross-border operations early.

- Liquidity tolerance: Minimum balance terms can make one bank practical and another expensive.

- Onboarding method: Confirm whether the shareholder, signatory, or both must appear in person.

For a broader practical shortlist, this guide to good banks for business accounts is a useful starting point. And if your business also needs wider payment infrastructure or cross-border support, providers offering financial services solutions can help complement your core banking setup.

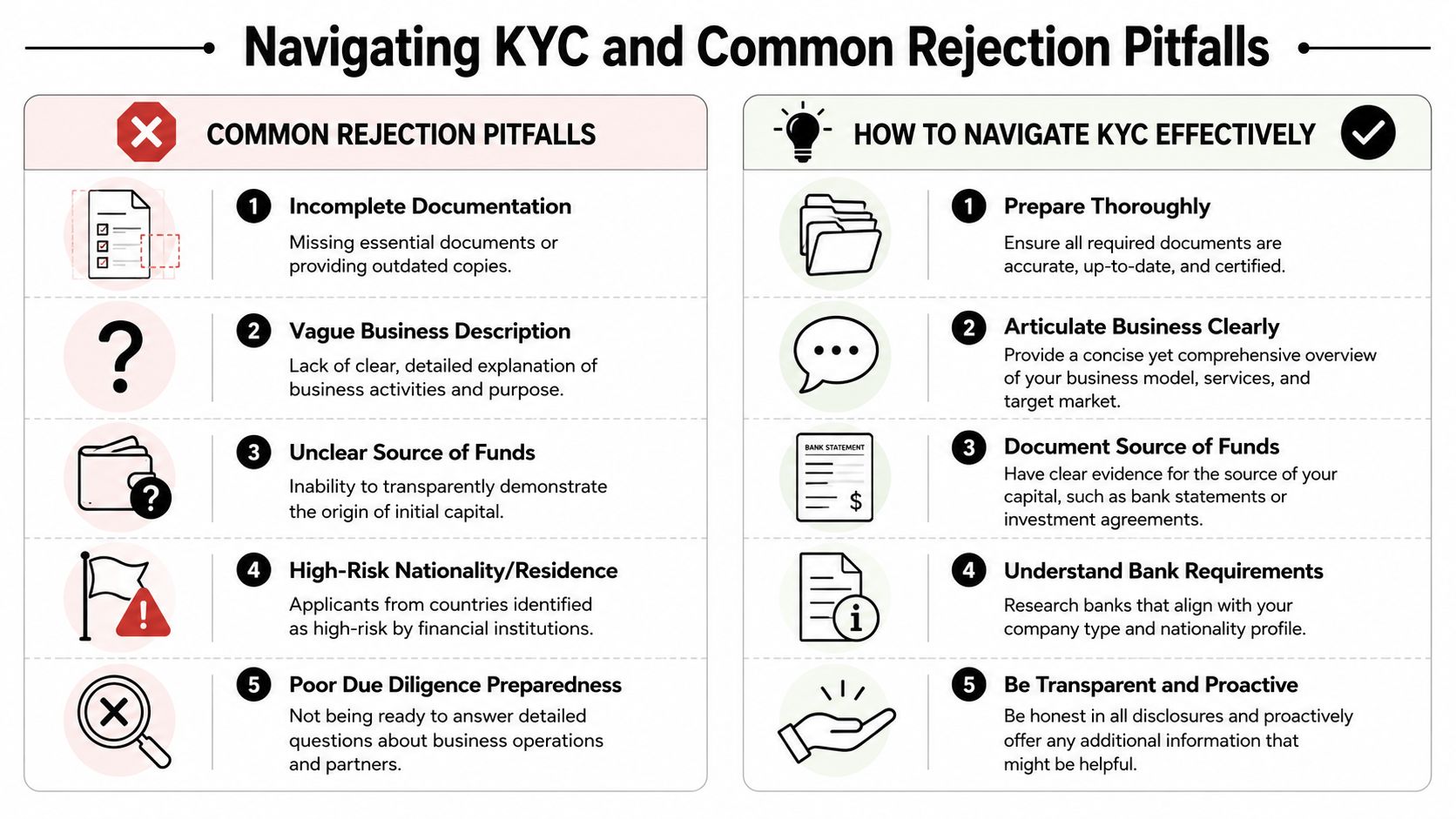

Navigating KYC and Common Rejection Pitfalls

A foreign founder gets the company set up, uploads the standard documents, and expects the bank account to follow. Then the questions start. What exactly do you sell? Why does the licence say one thing while the website says another? Who are the first customers, and where will the money come from?

That is the part many applicants underestimate.

KYC for a UAE corporate account is not an admin check. It is a risk review. The bank is trying to decide whether your business model is clear, your ownership is traceable, and your expected transactions fit the profile you presented. If those pieces do not line up, approval slows down or the file is declined.

Banks review credibility, not just completeness

Founders often assume a complete file is a strong file. It is not. A complete file can still raise doubts if the business story is vague.

Banks want a version of your company that is easy to verify. That means a clear description of what you do, who you bill, which countries you deal with, and why the UAE company is the right operating vehicle. If the application says “consulting, software, trading, and general services,” compliance reads that as uncertainty. If it says “software implementation for B2B clients in the GCC, invoiced by the UAE entity, with payments received by bank transfer,” the reviewer has something concrete to assess.

Specificity lowers friction.

Activity mismatch causes more rejections than founders expect

One of the common reasons for refusal is a mismatch between the licensed activity and the actual operating model.

Grow Across explains this problem well in its review of UAE business banking. The practical issue is simple. Banks do not stop at the trade licence. They compare the licence against the website, company profile, sample invoices, contracts, counterparties, and the answers given by the shareholder or signatory.

Many foreign investors are often caught when a licence, broad enough in a corporate setup sense, still looks weak under bank compliance review. I see this often with companies that describe themselves one way for incorporation and another way once they start speaking to banks.

Banks usually compare these points:

- Website language and service descriptions

- Invoices, proposals, and draft agreements

- Customer and supplier locations

- Expected monthly transaction types

- The explanation given in forms or interviews

If your licence points to consultancy but your materials show product trading, or if the company looks like it will receive money on behalf of third parties, expect scrutiny.

The better question is not whether the licence can technically include the activity. The better question is whether the activity can be explained clearly and defended consistently.

Remote onboarding is less straightforward than many founders assume

This is another hidden problem, especially for non-resident shareholders.

A bank may say onboarding can be done remotely, but that often depends on the shareholder profile, the nationality mix, the type of activity, and the comfort level of the compliance team reviewing the file. In practice, remote opening is not a blanket rule. A case can begin remotely and still end with a request for in-person verification, original documents, or a meeting with the signatory.

That catches founders who planned the process from abroad and assumed the account would be approved without travel.

The practical fix is to ask the bank two separate questions early. Can the application start remotely? Can the account be approved and activated without the shareholder or signatory attending in person? Those are not the same question, and banks answer them differently.

How to make the file easier to approve

Start by writing a short operating summary in plain English. Keep it factual. State what you sell, who pays you, where those clients are based, and how funds move in and out of the account.

Then check consistency across the file. The trade licence, website, company profile, contracts, and transaction explanation should describe the same business. If you have several licensed activities, lead with the one that drives revenue instead of presenting every possible line of business at once.

Source of funds also needs more than a generic statement. “Personal savings” is too thin on its own. Banks want a traceable origin and a simple explanation that matches the shareholder's background and supporting documents.

Prepare the owners and signatories as well. A polished application can still fail if the interview answers are hesitant, contradictory, or too broad. Compliance teams notice quickly when a founder does not sound fully clear on customers, suppliers, or expected transaction flows.

A strong KYC file does one thing well. It makes the business easy to believe.

When to Use a Consultancy like Smart Classic Business Hub

Some founders can handle the process themselves. If the company is simple, the shareholder is resident, the activity is straightforward, and the documents are already organised, self-managing the application can work.

But there are situations where outside help is the sensible move.

Cases where support saves time

A consultancy becomes useful when the file has moving parts that banks are likely to question:

- Non-resident shareholders: Remote onboarding assumptions often collapse once physical verification enters the process.

- Activity complexity: Mixed business models, broad licences, or unusual transaction flows need sharper positioning.

- Previous rejection: Once a bank declines a file, the next application should be adjusted, not merely resubmitted.

- Time pressure: Founders trying to launch operations quickly usually don't want to spend weeks learning bank-specific preferences.

What practical support should look like

Useful help is not “we submit forms for you”. It is support that improves bank-readiness.

That usually means:

- refining the business description for compliance review

- checking whether the licence and the operating model align

- helping prepare source-of-funds and transaction explanations

- steering the founder towards banks that fit the profile instead of broad, low-probability applications

One option in that category is Smart Classic Business Hub, which works with founders on UAE setup, documentation, and banking-related preparation as part of wider company formation support.

If you've been delayed, rejected, or you're applying as a foreign investor without local history, the primary value of a consultancy is not convenience alone. It's avoiding preventable mistakes that cost time and credibility.

If you want a practical route through the UAE banking process, Smart Classic Business Hub can help you prepare the right documents, align your business activity with bank expectations, and approach the banks that fit your company structure and shareholder profile.