You've probably felt the mismatch already. Sales look healthy in Xero or QuickBooks. The P&L says the business is moving. But the bank balance tells a different story, especially when customers pay on terms, suppliers want settlement before your receipts land, and VAT sits inside the account making the cash position look better than it really is.

That's where a Cash Flow Statement Template stops being an admin file and becomes a control tool. In the UAE, generic templates usually miss two realities that matter every week. First, payment timing drives liquidity far more than accounting profit. Second, VAT can distort decision-making if you treat collected tax as spendable cash.

Used properly, a cash flow statement template helps you see what's operational, what's structural, and what's temporary. It also gives you a format that lenders, investors, finance teams, and founders can all read consistently.

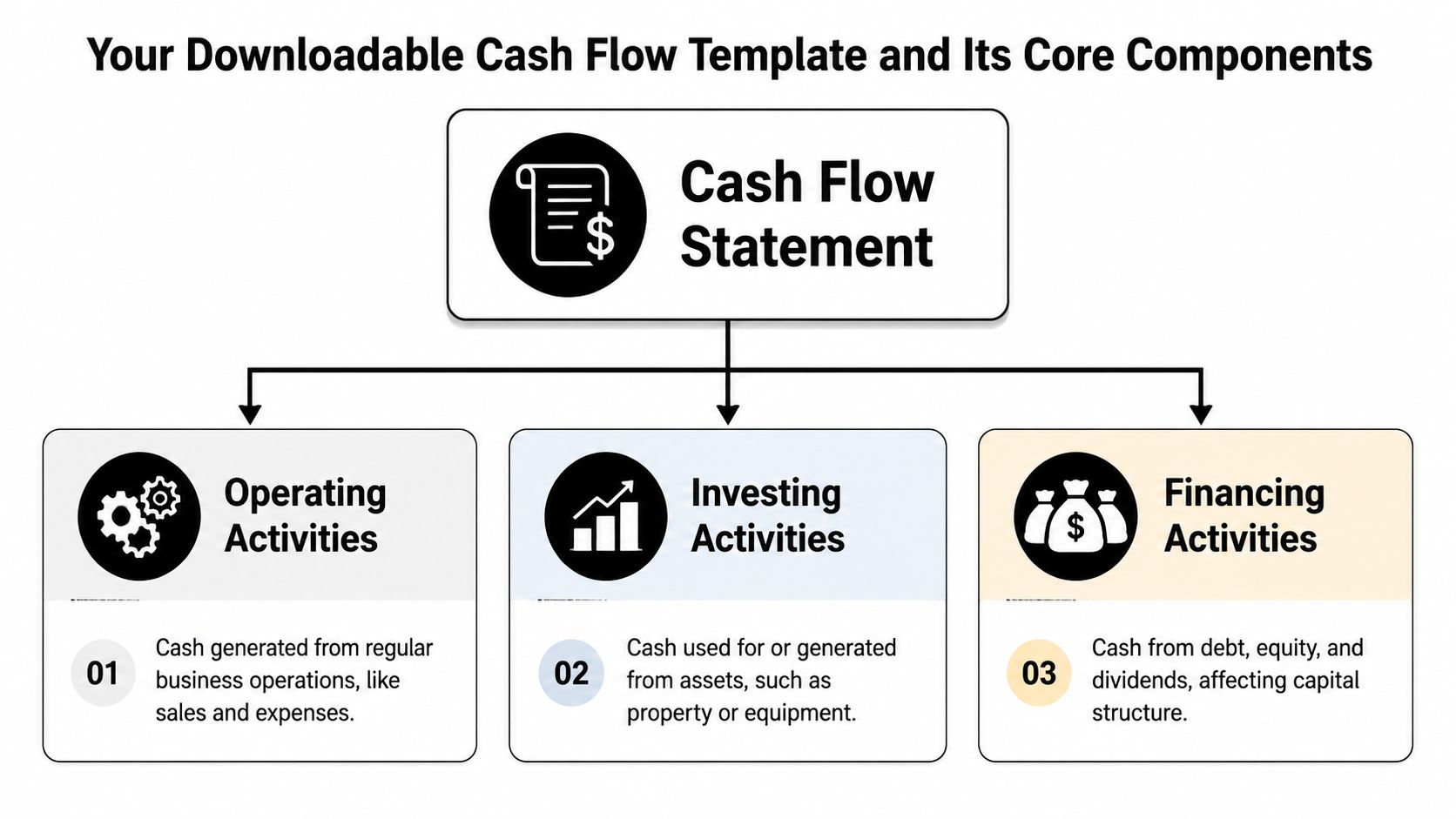

Your Downloadable Cash Flow Template and Its Core Components

Most templates fail because they're built like spreadsheets, not like businesses. A useful Cash Flow Statement Template has to follow the actual logic of cash movement. That means three standard sections: operating activities, investing activities, and financing activities, which is the accepted structure for the statement of cash flows according to CFI's guidance on the statement of cash flows.

Operating activities

This is the section most founders should watch first. It captures the cash that comes in and goes out from normal trading. For a UAE company, that usually means customer collections, supplier payments, payroll, rent, utilities, software subscriptions, logistics, and routine tax-related cash movements if you choose to show them operationally.

If you run a trading company, inventory purchases often shape this section more than revenue does. If you run a service business, the big pressure points are usually collections, salaries, and contractor payouts.

Practical rule: If the transaction comes from day-to-day trading, start by testing whether it belongs in operating activities.

Investing and financing activities

Investing activities cover longer-term asset decisions. Think laptops for a new team, fit-out spending, vehicles, machinery, or software development costs where your accounting policy treats them as longer-term assets. A free zone setup fee may need careful treatment depending on how it's recorded in your books, so the template should align with your accounting file rather than guess.

Financing activities capture capital structure. Founder injections, investor funds, bank loan proceeds, loan repayments, and dividend payments belong here. This section answers a blunt question. Is the business funding itself from operations, or is cash being supported from outside?

A simple way to design the template is to include:

- Opening cash balance tied to your bank and cash ledger

- Section totals for operating, investing, and financing

- Net cash movement for the period

- Closing cash balance that must reconcile back to the balance sheet

That final reconciliation matters. It's what turns a worksheet into a report that a bank or finance manager can trust. If you're building a broader finance stack around it, your operating account structure also matters, especially if you're setting up or reviewing a business banking account in the UAE.

For shorter-term planning, don't rely on annual templates alone. A well-built working file should let you predict cash flow shortages before they become missed payroll, delayed supplier payments, or emergency funding conversations.

Completing Your Template Section by Section

A good template only works if the inputs are clean. In practice, I've found most cash flow errors come from one of three things: mixing accrual numbers with cash numbers, misclassifying one-off payments, or forgetting that timing matters more than labels.

Start with the cash ledger, not the P&L

Pull your bank transactions first. Then pull your accounting detail. The bank tells you what moved. The accounting system tells you what it was.

For practical treasury control, a 13-week direct-method forecast is the standard horizon for identifying near-term cash pressure, while monthly or quarterly indirect-method reconciliation is more common for formal reporting, as noted in QuickBooks' cash flow statement template guidance.

That means you should usually build the template in two layers:

| Use case | Method | What goes in |

|---|---|---|

| Weekly control | Direct method | Actual or forecast receipts and payments |

| Formal period reporting | Indirect method | Net income adjusted for non-cash items and working capital movements |

Fill in operating activities

With the direct method, list cash in and cash out line by line. This is the most useful format for owner-managed businesses because it mirrors how money moves through the bank.

Typical direct-method lines include:

- Customer receipts: Cash received from invoices, advance payments, or point-of-sale sales

- Supplier payments: Inventory, raw materials, subcontractors, freight, clearing, and recurring vendors

- People costs: Salaries, wages, commissions, and visa-related payroll cash outflows where applicable

- Overheads: Rent, utilities, marketing, subscriptions, telecoms, insurance, and routine admin spend

With the indirect method, start from net income and adjust for items that affected profit but not cash. Then adjust for changes in receivables, inventory, and payables. It's more compact, but it can hide urgency. A profitable business can still run short of cash if receivables are stretching or stock is building.

The direct method helps operators manage next week. The indirect method helps accountants explain last month.

Record investing activities carefully

This section is where many SMEs bury cash drains by accident. If you buy a delivery vehicle, warehouse equipment, a server, or long-term software, don't leave it in overheads just because it was paid from the operating account.

A clean investing section usually includes:

- Asset purchases such as equipment, vehicles, fit-out, and technology.

- Asset sales if you dispose of older equipment or recover cash from a sale.

- Longer-term deposits or investments if the business parks cash outside normal operations.

The point isn't technical perfection for its own sake. It's visibility. Management should be able to separate cash spent to run the business from cash spent to build it.

Capture financing without mixing it with trade cash

Founder cash injections often get confused with revenue. Loan proceeds get mixed into collections. Repayments disappear into general expenses. All three create noise.

Keep financing lines distinct:

- Equity in: Founder or investor funding received

- Debt in: Loan proceeds or credit facilities drawn

- Debt out: Principal repayments

- Owner distributions: Dividends or drawings where relevant

When the template is complete, test one thing before anything else. Opening cash, plus net movement across all sections, must equal closing cash. If it doesn't, the file is not ready.

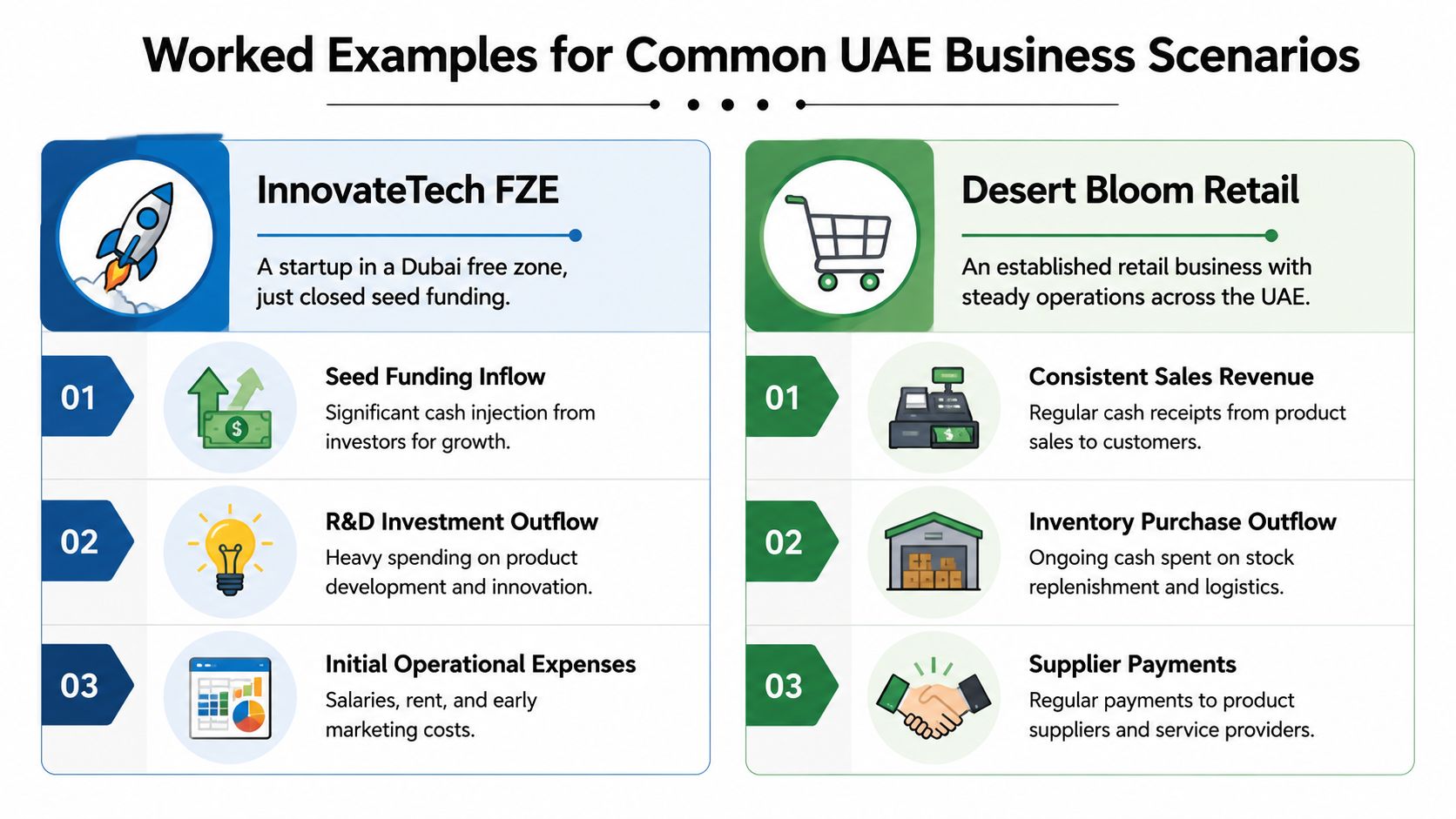

Worked Examples for Common UAE Business Scenarios

Two companies can have the same bank balance and completely different cash risk. That's why a Cash Flow Statement Template has to reflect business model, not just accounting structure.

InnovateTech FZE

InnovateTech FZE is a newly incorporated free zone startup. It has just received seed funding from its founders and early investors. Revenue exists, but it's inconsistent and still too early to fund operations reliably.

Its cash flow story usually looks like this:

- Financing dominates first. The major inflow is founder capital or investor funds.

- Investing appears early. The company buys laptops, development tools, office equipment, and may spend on setup costs that are treated as longer-term assets.

- Operating cash is negative at the start. Salaries, cloud subscriptions, legal support, licences, rent, and early customer acquisition spend go out before collections become stable.

This is normal for a startup. The mistake is not negative operating cash. The mistake is pretending that funding cash and earned cash are the same thing. In a template, they must stay separate or management loses sight of runway.

Global Traders LLC

Global Traders LLC is an established mainland SME involved in import and resale. Its problem isn't startup burn. Its problem is working-capital tension.

The monthly pattern is more operationally intense:

| Area | What happens in cash terms | What management needs to watch |

|---|---|---|

| Receivables | Customers buy now and pay later | Collection discipline |

| Inventory | Stock is purchased before it is sold | Reorder timing and overbuying |

| Payables | Suppliers may offer terms, but not always on the same cycle as customer receipts | Payment scheduling |

This company may look profitable on paper while cash tightens in the bank. That happens when stock arrives, customs-related costs hit, supplier invoices fall due, and customer receipts lag behind.

A trading business can grow itself into a cash problem if sales rise faster than collections.

Why the templates should differ

The startup template should give management a sharp view of runway, financing dependence, and burn drivers. Weekly granularity matters. Hiring plans, software commitments, and one-off setup spend need their own visibility.

The trading company needs tighter operating detail. Separate lines for customer collections, inventory purchases, key supplier payments, and VAT-related cash movements are more useful than a highly compressed statement.

Both companies still use the same three-part structure. What changes is the level of detail inside the lines. A founder-led startup often needs clearer financing visibility. A mature SME usually needs stronger working-capital control.

That's why copying a generic template from the internet often fails. It may be technically correct, but operationally useless.

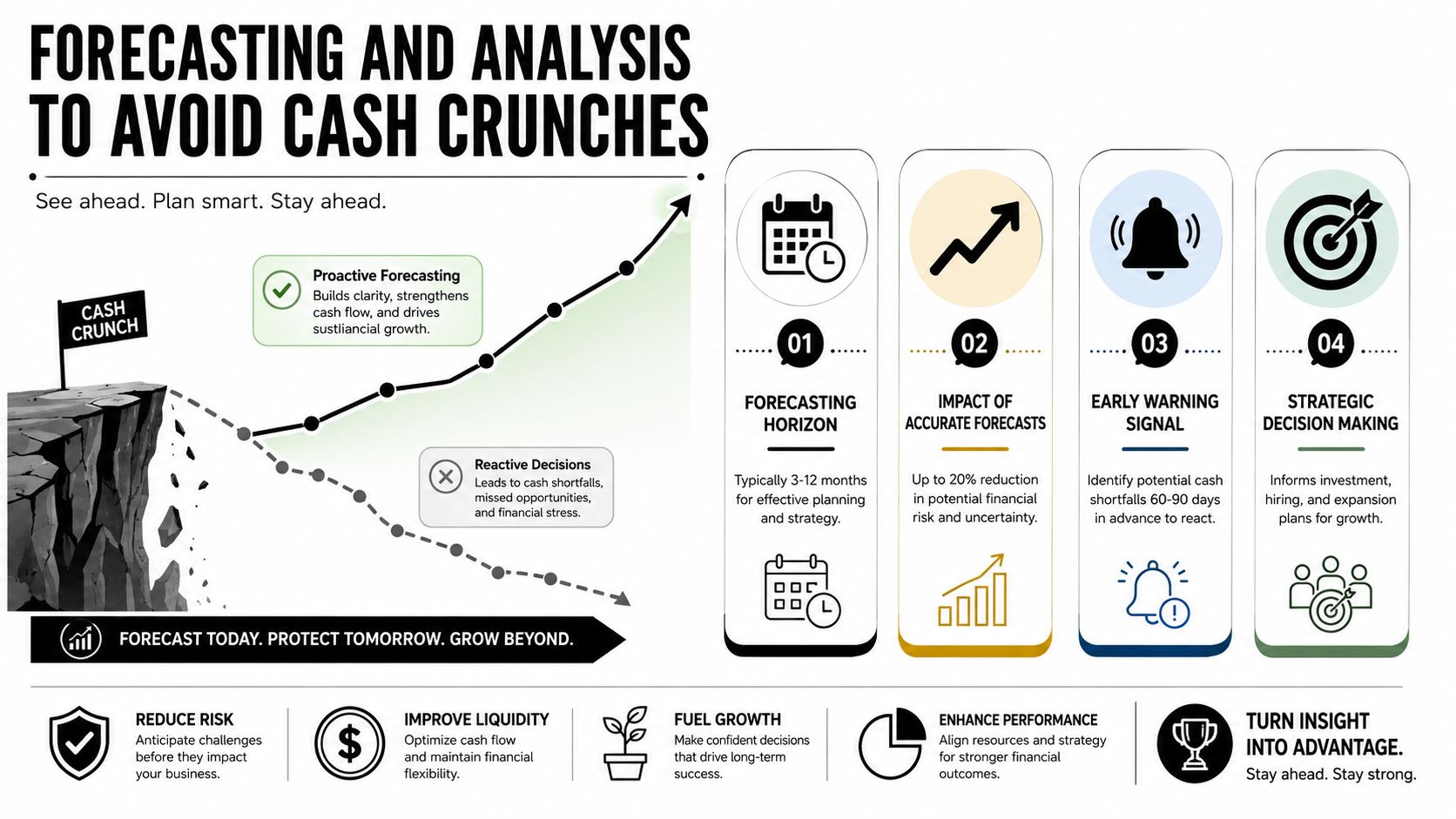

Forecasting and Analysis to Avoid Cash Crunches

Historical reporting tells you what happened. Forecasting tells you whether the business is about to get squeezed.

In the UAE, timing isn't a side issue. According to the World Bank data cited by Harvard Business School Online, firms in the United Arab Emirates faced an average of 38.9 days to collect from customers and 44.2 days to pay suppliers, with Dubai at 52.2 days to pay suppliers and Abu Dhabi at 62.1 days. Those timing gaps are exactly why cash forecasting matters in practice, not just in theory, as noted in HBS Online's cash flow guidance.

Build a working forecast, not a presentation file

A useful forecast is usually operational, not polished. It should let you answer simple questions fast:

- What cash is likely to come in this week

- Which payments are unavoidable

- Which outflows can be delayed without damaging the business

- Where the lowest projected cash point sits

If a client says they'll pay at month end, don't place the receipt on invoice date. Put it on the date cash usually arrives. If a supplier has terms on paper but frequently pushes for earlier settlement, forecast the actual pattern, not the contractual one.

Stress-test the weak points

Good forecasting isn't about optimism. It's about pressure-testing assumptions before the bank does it for you.

Use scenario planning around a few variables:

Late collections

Move a major customer receipt later and see what happens to payroll week and rent week.Inventory build-up

Test what happens if demand softens and stock sits longer than expected.New hires or expansion costs

Add the full cash impact, not just salary. Recruitment, onboarding, equipment, visas, and setup all matter.Tax settlement timing

If VAT is due, ring-fence it in the forecast so the operating position isn't overstated.

Forecasting works best when the owner, finance lead, and operations team challenge the same numbers together.

Use external advice selectively

Some owners overcomplicate forecasting with dense models they never update. Others keep it too simple and miss obvious shocks. A balanced approach is to use a working spreadsheet, review it weekly, and compare forecast against actual so assumptions improve over time.

If you want a practical outside perspective on tightening cash discipline, this roundup of Baron Accounting cash flow advice is useful as a companion read. The value isn't in copying another business. It's in spotting controls you haven't built into your own process.

The forecast should end in action, not observation. Chase receivables earlier. Stage discretionary spending. Negotiate terms before pressure builds. If the file only tells you that cash is tight after it happens, it's too late.

Common Mistakes and UAE-Specific Financial Nuances

The most common mistake is simple. Owners assume profit means cash is available. It doesn't.

A profitable company can still be strained if customer money hasn't landed, if stock has absorbed cash, or if loan repayments and tax obligations are sitting just ahead. That's why a Cash Flow Statement Template has to be built from actual cash movement and then reviewed against operational reality.

Profit is an opinion until cash arrives

Profit follows accounting rules. Cash follows the bank.

That distinction matters most when businesses sell on credit. Revenue may be recognised now, but the related cash may arrive much later. The same problem shows up when large purchases are capitalised. The P&L spreads the expense over time, but the bank account feels the outflow immediately.

Typical errors include:

- Treating unpaid invoices as cash available: Sales booked are not the same as collections received.

- Hiding loan repayments in overheads: Principal repayments affect cash but not profit in the same way normal expenses do.

- Ignoring one-off outflows: Deposits, equipment purchases, visa-related payments, and annual renewals can hit hard if the template only tracks monthly averages.

VAT is not operating cash

A common pitfall for many UAE SMEs involves generic templates often ignoring VAT timing, which creates a false sense of liquidity. Guidance on cash flow setup emphasises the importance of stating whether figures include or exclude transaction taxes, and that principle is highly relevant in the UAE. Businesses need to separate VAT collected, VAT payable, and recoverable input VAT so they don't mistake tax held in trust for free cash, as reflected in guidance on setting up a cash flow statement.

A practical UAE template should include separate lines or a separate schedule for:

| VAT element | Why it matters in the template |

|---|---|

| VAT collected from customers | It increases bank cash but isn't yours to spend freely |

| Input VAT paid on purchases | It affects timing and recovery expectations |

| Net VAT due or recoverable | It shapes the real short-term cash position |

If your business files monthly or quarterly, map the expected settlement dates in the same forecast file. Otherwise the bank balance can look comfortable until the filing cycle turns.

Keep VAT visible. Hidden VAT is one of the fastest ways to overstate available cash.

For businesses that need the compliance side handled properly as well as the reporting side, it helps to understand the mechanics of VAT filing in the UAE and align your template with the filing calendar.

Classification mistakes that distort management decisions

Not every error breaks the accounts. Some errors make management decisions worse.

A few examples:

- Founder funding shown as sales makes operations look stronger than they are.

- Asset purchases buried in operating expenses make routine overhead look inflated and hide investment decisions.

- No split between recurring and non-recurring cash items makes forecasting noisy and hard to trust.

The best templates aren't the most complicated. They're the clearest. You should be able to open the file and answer three questions quickly. What cash came from trading. What cash went into assets. What cash came from or went back to funders.

Turning Your Cash Flow Statement into a Growth Strategy

A business that understands cash makes better decisions earlier. That's the strategic value of a Cash Flow Statement Template. It tells you whether growth is being funded by customer receipts, by slower supplier payment, or by fresh debt and equity. Those are not the same thing, and they lead to very different choices.

When cash is consistently healthy, management can expand with more confidence. That might mean hiring, opening a new line of business, investing in stock, or upgrading systems. When cash is tight, the right response is usually operational first. Improve collections. Reduce unnecessary stock build. Delay discretionary spend. Restructure payment timing where possible.

The UAE rewards businesses that stay organised on liquidity. Payment cycles, VAT timing, and growth-related outflows can all pressure the account before the P&L shows a problem. Owners who review cash weekly usually spot pressure early enough to act. Owners who review it only for year-end reporting usually react late.

If growth decisions, capital planning, or funding readiness need a stronger framework, specialist support in corporate finance advisory in Dubai can help turn a reporting file into a decision-making tool.

If you want help building a UAE-ready cash flow model, tightening VAT-aware reporting, or setting up finance processes that support growth, Smart Classic Business Hub can help you structure the numbers properly from the start.