You’ve got the trade licence. The company is live. Suppliers are asking where to send invoices, and your first client wants your IBAN before they release payment. Then the banking reality hits. The UAE is business-friendly, but corporate banking still has gatekeepers, paperwork, and more conditions than most founders expect.

That’s why the zero balance business bank account in uae has become such a popular starting point. It sounds simple. No minimum balance. Fast setup. Digital onboarding. For a new entrepreneur, that sounds like relief.

It can be. But only if you understand what “zero balance” means in practice, where the hidden conditions sit, and when a low-cost account creates bigger problems later in tax, compliance, or operations.

The First Big Hurdle Understanding UAE Business Banking

You register the company on Monday. By Wednesday, a supplier wants a transfer receipt, your landlord asks for a company cheque, and your first client says payment will be released once they have your business IBAN. That is usually the moment founders realise company formation was the easy part. Banking is where the first operational delay starts.

In the UAE, banks do not assess a new business only on the trade licence. They look at expected turnover, business activity, shareholder profile, visa status, source of funds, and whether the company looks like it will maintain regular account activity. A zero balance account can reduce the cash pressure at the start, but it does not remove those checks.

Why founders look for zero balance first

The reason is simple. Early-stage businesses need liquidity more than they need an expensive banking package.

Traditional UAE business accounts often come with minimum balance requirements and shortfall fees. For a startup, that can mean leaving useful cash idle instead of putting it into inventory, staff, ads, software, or visa costs. Zero balance options appeal because they lower the amount trapped inside the banking setup from day one.

That matters more than many banks admit. A founder may save the minimum balance requirement, then discover the actual test is monthly usage, transfer volume, or maintaining enough activity to avoid review.

What founders are actually buying

A zero balance account is not just a cheaper account. It is a trade-off.

You keep more cash available, which helps in the first six to twelve months. In return, you may get tighter transaction limits, fewer relationship support options, stricter monitoring for low activity, and fee triggers tied to services rather than balance. For some companies, that is a fair exchange. For others, it creates friction later, especially once payroll, VAT filings, supplier payments, and corporate tax recordkeeping become routine.

I usually tell founders to judge the account by operating fit, not by the headline label.

Here is what usually makes zero balance attractive at the start:

- Better cash control: funds stay available for operations instead of sitting in the account to satisfy a threshold

- Lower entry cost: founders can start banking without setting aside a large reserve

- Faster early operations: some providers support more digital onboarding and simpler day-to-day use

- Cleaner startup budgeting: banking costs are easier to forecast if the company is still testing revenue

The catch is that "low-cost" and "low-friction" are not the same thing.

A free zone consultancy with a few invoices a month may do well with a lean account. A trading company handling regular supplier transfers may outgrow it quickly. An e-commerce business may open one for speed, then need a second banking relationship once payment volume increases. Founders comparing providers should look beyond the zero balance label and review broader business bank options in the UAE before choosing.

The first hurdle is not opening any account. It is opening the right account for your transaction pattern, compliance obligations, and growth plan.

Demystifying Zero Balance What Banks Don't Advertise

A founder opens a zero balance account expecting a cheap starting point. Three months later, the account is active but still expensive. Monthly charges appear because usage stayed below an internal threshold, international transfers cost more than expected, and the bank starts asking for clearer proof of business activity. That pattern is common in the UAE.

“Zero balance” only tells you one thing. You do not need to park a minimum amount in the account. It does not mean the account is low-cost, easy to keep, or suitable for every business model.

The catch behind the label

Banks usually recover the waived minimum balance in other ways. The charges are often tied to account behavior rather than account opening. That can include monthly fees after an introductory period, transfer charges, higher FX spreads, limits on teller or branch transactions, and penalties if turnover stays too low.

Some providers also package zero balance accounts as digital-only products with narrower operating features. That works for a service business with simple inbound and outbound payments. It becomes restrictive if the company needs cheque handling, trade finance support, cash services, or multi-user approval controls.

A no minimum balance business account in the UAE can still be the right choice. The question is whether the account economics make sense after the first few months, once real banking activity starts.

What banks screen for quietly

Founders often assume approval depends on trade licence, passport, visa, and company documents. Those matter, but banks also look at commercial logic and compliance risk.

In practice, applications get harder when the company shows one or more of these signals:

- Weak expected activity: no clear invoice flow, no signed contracts, or no explanation of where incoming funds will come from

- Mismatch between licence and use case: a consultancy account application that mentions cash-heavy trading activity, or a general trading licence with no supplier background

- Unclear source of funds: shareholder profile, startup capital, or first transactions are not documented properly

- High-risk payment corridors: expected transfers to jurisdictions or sectors that trigger more compliance review

- Low substance: no website, no customer pipeline, no tenancy evidence where one is reasonably expected, or no operating narrative the bank can follow

Many “startup-friendly” claims often falter here. A bank may accept new companies in principle, but still reject or restrict businesses that look inactive, poorly documented, or difficult to monitor.

The trade-off founders usually miss

Zero balance accounts are often sold as a simpler option. They are simpler only if your business is simple from a banking perspective.

A solo consultant billing local clients by bank transfer may find the model efficient and cost-effective. A small trading company may save on minimum balance requirements, then lose that benefit through transfer fees, compliance delays, and account limitations. An e-commerce company can run into another problem. Settlement inflows may look healthy, but chargeback patterns, payment processor flows, and cross-border refunds can make the account harder to manage than the marketing suggests.

Corporate tax adds another layer. Once the business is within the UAE corporate tax regime, the bank account stops being just a payment tool. It becomes part of your audit trail. If founders use a basic account with weak statement clarity, mixed personal and business transfers, or poor payment narration, the cleanup work later is expensive. Accountants can fix some of it, but they bill for that time.

What to check before you commit

A zero balance account can work well, but only after a proper stress test. Review these points before signing anything:

- Monthly fee after any promo period

- Minimum turnover or usage conditions

- Transfer fees, FX margin, and cash deposit charges

- Limits on users, cards, and approval workflows

- Support for VAT and corporate tax recordkeeping

- Ease of getting stamped statements, bank letters, or compliance confirmations

- Whether the bank is comfortable with your actual activity, not just your licence title

I usually tell founders to read the fee schedule and the eligibility criteria together. One shows what the account costs. The other shows how easily the bank can make the relationship difficult.

The right zero balance account is a strategic starting tool. It helps preserve cash in the early stage. It can also create hidden cost, friction, and tax recordkeeping problems if the business profile does not fit the account.

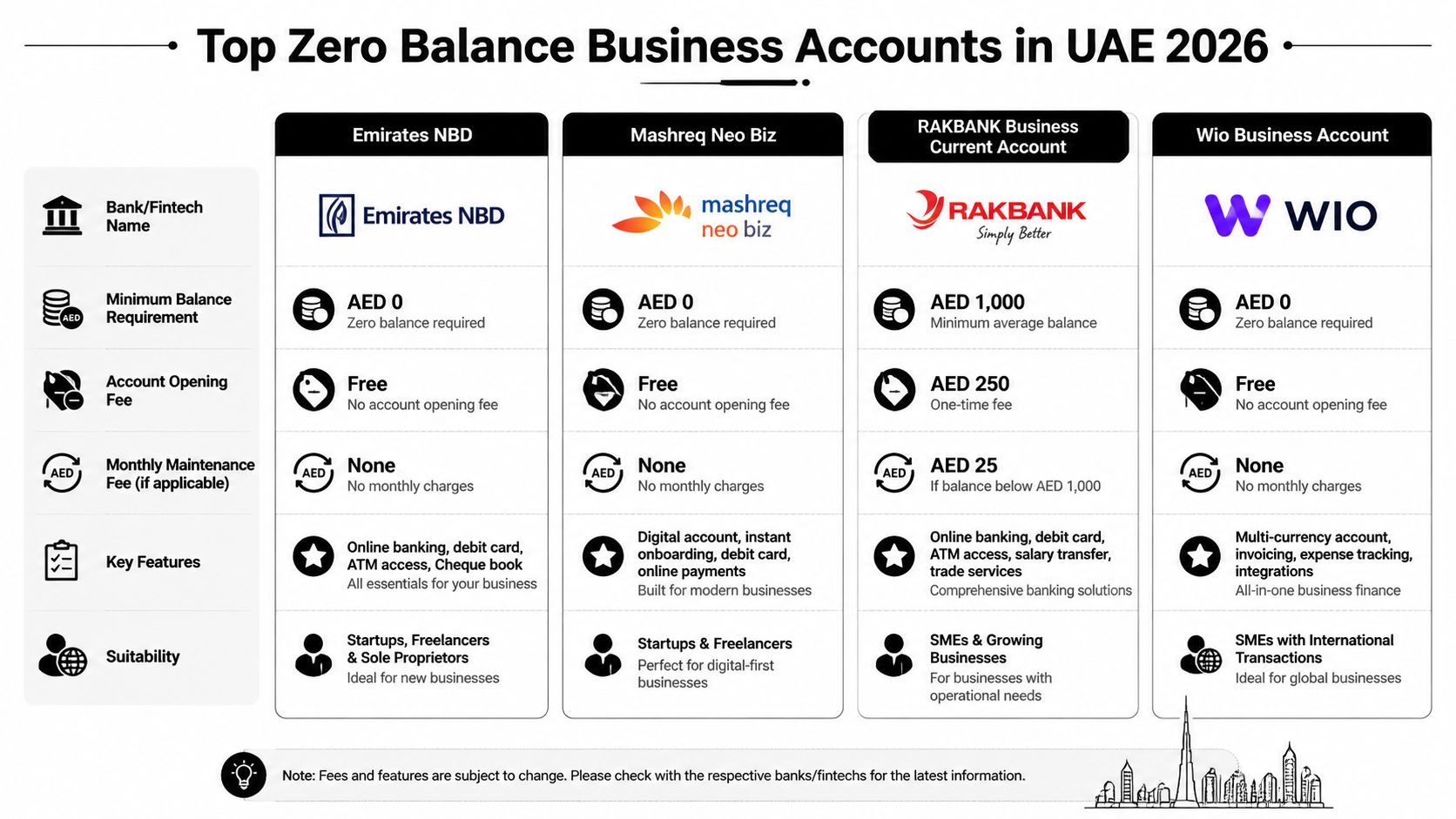

Comparing Top Zero Balance Business Accounts in 2026

A founder opens a zero balance account to avoid tying up cash, then discovers three months later that the true cost sits elsewhere. Transfer fees are higher than expected. FX spreads eat into overseas receipts. The bank asks for extra clarification on routine payments because the business activity and transaction pattern do not line up neatly. That is the comparison that matters in 2026.

A useful shortlist starts with Mashreq NeoBiz, RAKBANK RakStarter, ADCB Starter Business Account, and digital-first options such as Hubpay or Wio. The right choice depends less on the headline promise of "zero balance" and more on how the account behaves once invoices start coming in, suppliers need paying, and corporate tax records have to be clean.

What to compare beyond the headline

Banks and fintechs package these accounts differently, but the practical filters stay the same.

- Monthly cost in real use: Check the fee after any introductory period, and check whether the account stays low-cost if monthly activity is light.

- Transaction economics: Review local transfers, international payments, FX margin, cash deposit charges, and any cost for extra cards or users.

- Eligibility fit: Some accounts look startup-friendly but become harder to maintain if the company has foreign shareholders, higher-risk activity codes, frequent cross-border receipts, or unclear source-of-funds documentation.

- Tax and audit usability: Clear statements, usable payment references, downloadable records, and support for bank letters matter once bookkeeping and corporate tax filings begin.

- Operational ceiling: Approval workflows, payroll capability, cheque access where relevant, and integration with accounting habits all affect whether the account still works after the launch phase.

2026 Comparison of UAE Zero & Low-Balance Business Accounts

| Provider | Account Name | 'True' Monthly Fee | Key Feature | Best For |

|---|---|---|---|---|

| Mashreq | NeoBiz / NeoBiz Lite | Can include monthly charges depending on plan conditions | Strong app experience and broad day-to-day banking tools | Early-stage service businesses that want speed and can track plan rules closely |

| ADCB | Starter Business Account | Depends on account terms and activity conditions | Established bank relationship with an entry-level business option | Founders who prefer a conventional bank and expect more formal banking needs later |

| RAKBANK | RakStarter | Depends on current structure and usage | SME-oriented onboarding and practical business banking setup | Small trading or service companies that want a bank-led route |

| Hubpay | Business account offering | Depends on account structure and usage | Digital onboarding and multi-currency functionality | Internationally active startups comfortable with fintech processes |

| Wio | Business account offering | Depends on plan selected | Digital-first interface and fast setup experience | Lean teams with simple approval needs and online-heavy operations |

This is not a winner-versus-loser table. It is a trade-off table.

Which account tends to suit which founder

A solo consultant or small agency usually prioritises fast setup, low fixed cost, and easy outbound transfers. A digital-first account can suit that model well, especially if transaction volumes are predictable and there is no need for complex approval layers.

A mainland SME handling payroll, supplier payments, VAT, and regular compliance requests should be more careful. The cheapest opening option can become expensive if statements are hard to reconcile, support is slow, or the bank becomes cautious about transaction patterns after onboarding. I have seen founders save on opening costs, then spend far more later on accounting cleanup and bank clarifications.

Trading businesses need even more caution. Zero balance does not always mean low-friction. Cash deposits, international remittances, and higher transaction frequency can expose fee lines that service businesses barely notice.

The better question is simple. Will this account still be workable once the company is filing corporate tax, answering auditor queries, and processing routine supplier payments every week?

If you are narrowing your shortlist, this guide to a no minimum balance business account in the UAE helps frame the practical differences.

Your Step-by-Step Guide to Opening an Account

A founder gets the trade licence, signs the lease, pays the setup fees, then assumes the bank account is the easy part. In practice, banking is often where the first serious delay appears. The problem is rarely the company itself. The problem is a weak file, unclear expected activity, or an ownership structure the bank views as higher review.

Zero balance business accounts are usually marketed as simple. The application process is not. Banks still screen for risk, source of funds, business model clarity, shareholder profile, and whether the account will be used in a way that matches the licence. Free zone companies can often open accounts online relatively quickly with some providers, while traditional banks may take longer and may still ask for an in-person step.

Phase one document preparation

Build the banking file before you start comparing portals and application forms. Many approvals are won or lost at this stage.

Most banks and fintech providers will ask for:

- Valid trade licence: The activity on the licence should match the way you describe the business to the bank.

- Incorporation documents: MOA, AOA, certificate of incorporation, or the free zone equivalent.

- Shareholder and signatory IDs: Passport, visa page, and Emirates ID where available.

- Proof of address: For the company, shareholders, or authorised signatories, depending on the provider.

- UBO details: If ownership is layered, expect questions about the ultimate beneficial owner.

- Business profile: A short summary of what the company does, who it sells to, expected monthly volume, and key countries involved.

This last item matters more than founders expect. A vague profile such as "general trading" or "consultancy services" often creates more questions, especially if the actual activity involves cross-border payments, crypto-adjacent work, high-volume transfers, or regulated sectors.

If the company will have payroll, tax filings, and annual audit requirements, prepare the file with that future use in mind. Clean records now make later work easier, including any review of UAE personal tax considerations for founders and residents where banking trails and residency evidence start to matter.

Phase two application submission

Submission is not just document upload. It is a risk presentation exercise.

The bank wants a coherent answer to three questions. What does the company do, who will it transact with, and why does this account fit that activity? If those answers are unclear, the application slows down even when the documents are technically complete.

Use the form carefully:

- Describe the activity in plain terms. "Marketing consultancy for UAE retail clients" is stronger than "business services."

- Explain expected flows. Mention approximate incoming and outgoing transaction patterns without guessing wildly.

- Name key geographies. Domestic-only businesses are reviewed differently from firms receiving funds from multiple jurisdictions.

- Disclose cash handling transparently. If the business expects cash deposits, say so early. Some zero balance options are poor fits for cash-heavy models.

- Match the signatory structure to real operations. If two partners approve payments internally, set that expectation from the start.

A cheap account can become expensive here. Some providers approve quickly, then place tight limits on transfers, supporting documents, or payment reviews after activation. That is not always visible in the marketing page.

Phase three verification and onboarding

Verification usually includes KYC checks, ownership review, and follow-up questions on the commercial model. Speed depends less on the headline promise and more on how easy your company is to understand.

A single-owner design studio with local clients is usually straightforward. A trading company with overseas suppliers, three shareholders, and frequent international remittances will face more review. That is normal.

Practical habits improve approval odds:

- Keep names identical across documents: Trade licence, tenancy contract, incorporation papers, and the application should all match.

- Send complete scans: Missing pages, cropped passport copies, and unclear stamps create avoidable delay.

- Reply fast to compliance queries: Slow responses often push files to the back of the queue.

- Prepare proof for source of funds: Initial capital, shareholder funding, and first expected receipts should make commercial sense.

- Check FATCA and CRS exposure early: Cross-border founders should understand how banking disclosures may apply. AuditReady's audit-ready compliance gives a useful overview of what banks may ask for.

One more point that gets missed. Approval is only the first test. Ongoing use matters more.

If the bank later asks for invoices, contracts, tax registration details, or counterpart information, the business should be able to produce them quickly. Founders who treat onboarding as paperwork often run into trouble later. Founders who treat it as the start of a compliance file usually have fewer payment holds, fewer review calls, and fewer surprises.

The Hidden Risk Corporate Tax Compliance and Your Bank Account

A founder opens a zero balance account on Monday, starts invoicing on Friday, and assumes the banking piece is done. Six months later, the company needs bank evidence for tax residency, audit support, or a compliance review, and the account that worked perfectly for collections turns into a weak point.

That happens more often than founders expect.

The problem is not corporate tax itself. The UAE corporate tax regime applies at 9% on taxable profits above AED 375,000, and many businesses can handle the filing side with proper accounting. The issue is whether the account you chose produces the kind of statements, account confirmations, and local banking trail that later applications may require. Some zero balance and fintech-led setups are efficient for day-to-day payments but less persuasive when a government body, auditor, or counterparty wants conventional banking evidence.

This matters most for founders who chose the account purely on speed, minimum balance relief, or lower fees. Those are valid priorities. They just should not be the only ones.

Where the real risk sits

A zero balance account can save cash at launch. It can also create hidden costs later.

The first cost is delay. If the business later needs stronger proof of banking presence in the UAE, the founder may have to open a second account under time pressure. The second cost is admin. Finance teams then have to reconcile activity across two platforms, explain why receipts hit one account while tax records reference another, and respond to extra compliance questions. The third cost is perception. For some tax, audit, or residency-related processes, a traditional local bank relationship still carries more weight than a newer payment platform.

None of this means fintech accounts are a bad choice. It means they are a tool with limits.

A practical structure for companies with tax exposure

For many mainland companies, import-export businesses, and firms with overseas shareholders, a hybrid setup is often the safer choice:

- Use one account for operating cash flow: collections, payroll, supplier payments, and daily transfers.

- Keep one conventional UAE bank relationship for formal banking evidence: account letters, stronger statements, and documentation support if tax residency or external review becomes relevant.

That setup adds work. It may also add fees. But it can reduce the risk of scrambling later when the company needs documents that a lighter digital provider does not issue in the format an authority or institution expects.

Cross-border founders should also look beyond corporate tax filings themselves. FATCA and CRS classifications can affect what banks request, how shareholder information is reviewed, and how account activity is monitored. AuditReady's audit-ready compliance is a useful reference if the ownership structure or transaction profile is international.

Questions to settle before opening the account

Founders should press the bank or provider on specifics, not general promises:

- Will the provider issue statements and bank letters that are accepted for tax residency or audit support if needed?

- Can the account history be used cleanly for VAT and corporate tax bookkeeping?

- Does the provider support the transaction pattern your licence suggests, especially if funds will move across borders?

- If the company scales, will the account still fit, or will you need to migrate later under pressure?

Banking and tax now overlap more than many first-time founders realise. A cheap account that saves money in month one can cost more in month twelve if it creates friction around tax records, residency proof, or compliance reviews. Founders with broader planning needs should also review the wider tax position early, including personal tax in the UAE, because ownership, residency, and banking records often intersect in practice.

How Smart Classic Business Hub Ensures a Seamless Launch

A founder gets the trade licence approved, receives the incorporation documents, and expects the bank account to be a quick final step. Then the bank asks for clarifications on business activity, shareholder background, expected monthly turnover, and proof that the company is commercially credible. That delay is where many launches lose momentum.

The problem is rarely one missing form. It is usually a mismatch between how the company was set up and how the bank will assess it. Banking, licensing, and tax records need to line up from day one if the account is meant to support real operations rather than create avoidable back-and-forth.

Zero balance accounts help keep early cash available for stock, payroll, visas, software, or marketing instead of tying funds up to satisfy a minimum balance rule. That advantage is real. It also comes with trade-offs, because the fastest account to open is not always the one that best supports the company six months later.

Where founders usually lose time

The delays are usually predictable.

- Documents do not match cleanly: The trade licence, MOA, shareholder details, and stated business activity raise questions when reviewed together.

- The account choice is too narrow: The founder chooses based on low entry requirements, then finds the account is weak on transaction flexibility, bank letters, or later support.

- The setup is treated as separate workstreams: Incorporation gets finished first, banking gets handled later, and tax considerations only appear after transactions begin.

What a better setup process looks like

Smart Classic Business Hub handles account readiness as part of the wider company launch, not as a simple introduction to a bank. That means preparing the document file in the format banks usually expect, checking whether the chosen provider suits the company’s activity and ownership structure, coordinating with PRO steps after incorporation, and flagging practical issues that can affect VAT bookkeeping or tax documentation later.

That approach saves time because it reduces avoidable mismatches. A founder does not need just any zero balance business account in the UAE. The founder needs one that fits the licence, the expected payment flow, the jurisdictions involved, and the level of banking proof the business may need later.

I have seen founders lose weeks by solving only for approval speed. The account opened, but the structure was poor for supplier payments, compliance queries, or formal banking documents. Fixing that later is usually slower and more expensive than choosing properly at the start.

A coordinated launch is usually a cleaner launch.

For a lean startup, that may mean choosing a zero balance option with clear limits and accepting that an upgrade may be needed later. For a mainland company with more complex transactions, it may be better to accept slightly stricter onboarding in exchange for stronger long-term fit.

Frequently Asked Questions About Zero Balance Accounts

Some of the most important questions don’t fit neatly into a sales page. They usually come up after a founder has already chosen a bank, or after an application is delayed.

Here are the practical answers.

| Question | Answer |

|---|---|

| Is a zero balance account always free? | No. “Zero balance” usually means no minimum balance requirement. It doesn’t always mean no monthly fee, no transaction conditions, or no usage thresholds. |

| Can a startup be rejected even with a valid trade licence? | Yes. A valid licence helps, but banks still assess activity profile, documentation quality, and whether the business appears commercially active. |

| Are free zone companies treated the same as mainland companies? | Not always. Free zone companies often find online onboarding simpler, while mainland entities may face more manual review depending on the provider and structure. |

| Will a zero balance account support every tax and compliance need? | Not necessarily. Some fintech-style account setups may be operationally convenient but less suitable when formal banking proof is needed for tax residency or related compliance matters. |

| Should I choose a fintech account or a traditional bank? | That depends on what the business needs first. If speed and lean operations matter most, digital-first can work well. If documentation strength and conventional banking comfort matter more, a traditional bank may be safer. |

| Can I use one account for everything? | Sometimes, yes. But businesses with international activity, tax residency requirements, or more formal reporting often benefit from separating daily operations from compliance-heavy banking needs. |

| What if my revenue is irregular in the first months? | Then review the account’s activity expectations carefully. Some accounts are more forgiving than others, and “low activity” can create problems if the bank expected a more active profile. |

| Do zero balance accounts suit growing SMEs? | They can suit the launch stage very well. Once transaction complexity increases, some businesses outgrow them and need a broader banking structure. |

The smartest approach is to treat zero balance banking as a tool, not an identity. It’s useful when it matches your stage, your documents, and your next compliance step. It’s less useful when it’s chosen just because the headline sounds cheap.

If you're setting up a company and want a practical banking route that also fits licensing, PRO work, VAT, and tax residency planning, Smart Classic Business Hub can help you organise the full setup properly. The value isn’t just opening an account. It’s making sure the account still works for your business after the launch week is over.