Before you even think about paperwork or online portals, the first and most important question is a simple one: do you actually need to register for VAT?

It all boils down to your business turnover. If your taxable supplies and imports have crossed the AED 375,000 mark in the last 12 months, the answer is a clear yes—VAT registration is mandatory.

Understanding the UAE VAT Registration Thresholds

Figuring out if you need to register for Value Added Tax (VAT) in the UAE isn't just about ticking a compliance box; it's a critical strategic decision for your business. The Federal Tax Authority (FTA) has set very clear financial benchmarks, or thresholds, that determine when a business must register, and when it can choose to.

Getting this right from the start is the bedrock of your VAT compliance journey. It’s what keeps you on the right side of the law and helps you sidestep some pretty hefty penalties.

There are really only two thresholds you need to keep in mind: one that forces your hand and one that gives you a choice.

- Mandatory Registration Threshold: This is the big one. If your total taxable supplies and imports have exceeded AED 375,000 over the past 12 months, you are legally required to register. The same applies if you expect to cross that line in the next 30 days.

- Voluntary Registration Threshold: Maybe you're not legally obligated to register just yet. You still have the option to if your taxable supplies or expenses are over AED 187,500 in the past 12 months.

The Mandatory Threshold Explained

That AED 375,000 figure is the most crucial number in the UAE's VAT system. If you cross it, you have to start the registration process immediately to avoid a painful AED 20,000 penalty for late registration. This rule has been in place since VAT was introduced on 1 January 2018, and it's a core part of the tax framework.

Calculating your turnover isn't a once-a-year thing. You need to look at a rolling 12-month period. For instance, at the end of May, you’d look at your total taxable sales all the way from last June to this May. It's a continuous calculation you should be doing regularly to stay ahead of the curve.

Why Consider Voluntary Registration?

It might be tempting to stay under the mandatory threshold to avoid the extra admin, but registering voluntarily can be a surprisingly smart move, especially for startups and growing businesses.

When your turnover is above AED 187,500, choosing to register can give you a real financial edge. The single biggest advantage is the ability to reclaim input VAT—that’s the tax you pay on all your business-related purchases and expenses.

By registering voluntarily, you can offset the VAT paid on your costs (like rent, software, or professional fees) against the VAT you collect from your customers. This can seriously improve your cash flow and trim your operational costs.

On top of that, being VAT-registered often gives your business a more professional look. Many larger corporations and government bodies prefer dealing with VAT-registered suppliers because it makes their own accounting much smoother. Having a Tax Registration Number (TRN) shows that your business is established and compliant, which can open doors to bigger contracts and better opportunities.

To help you see where you stand, here’s a quick comparison of the two thresholds.

UAE VAT Registration Thresholds at a Glance

This table quickly compares mandatory versus voluntary VAT registration criteria, helping you identify your business's obligations and opportunities.

| Criteria | Mandatory Registration | Voluntary Registration |

|---|---|---|

| Turnover Threshold | Exceeds AED 375,000 in the last 12 months (or expected in the next 30 days) | Exceeds AED 187,500 in the last 12 months |

| Legal Obligation | Yes, it is compulsory | No, it is optional |

| Key Benefit | Compliance and avoidance of penalties | Ability to reclaim input VAT on business expenses |

| Best For | Established businesses with consistent, high revenue | Startups, growing businesses, and B2B service providers |

Understanding which category your business falls into is the first step toward making a sound financial decision that aligns with both the law and your long-term growth strategy.

Real-World Scenarios for Clarity

Let's break down how these rules work in practice with a few examples.

-

Scenario 1: The E-commerce Shop

A Dubai-based online store selling electronics is growing fast. In October, the owner runs the numbers and realises their revenue for the past 12 months just hit AED 380,000. They have now crossed the mandatory threshold and must begin the VAT registration process right away. -

Scenario 2: The Freelance Consultant

A freelance marketing consultant in Abu Dhabi has an annual turnover of AED 250,000. She spends about AED 20,000 a year on software subscriptions and co-working space fees, all of which include VAT. By registering voluntarily, she can reclaim the AED 1,000 in VAT she paid on those expenses. As we cover in our guide to freelance visas and business setup, knowing your obligations is vital. -

Scenario 3: The New Café

A new café opens its doors and, based on a solid business plan, projects its revenue will hit AED 400,000 within the first six months. Since they fully anticipate crossing the mandatory threshold very soon, they are required to register for VAT within 30 days of making this projection.

Assembling Your Documents for a Flawless Application

Let's be honest, the paperwork is often the biggest headache when you're trying to register for VAT in the UAE. I've seen it time and time again—a single missing document or a blurry scan sends an application right back to square one, leading to completely avoidable delays.

Taking the time to get your documents in order before you start is the single best thing you can do for a smooth ride with the Federal Tax Authority (FTA). Think of it this way: you wouldn't build a house on a shaky foundation, and you definitely shouldn't submit a tax application with a messy, incomplete file. The FTA needs a crystal-clear picture of your business, its owners, and its financial health.

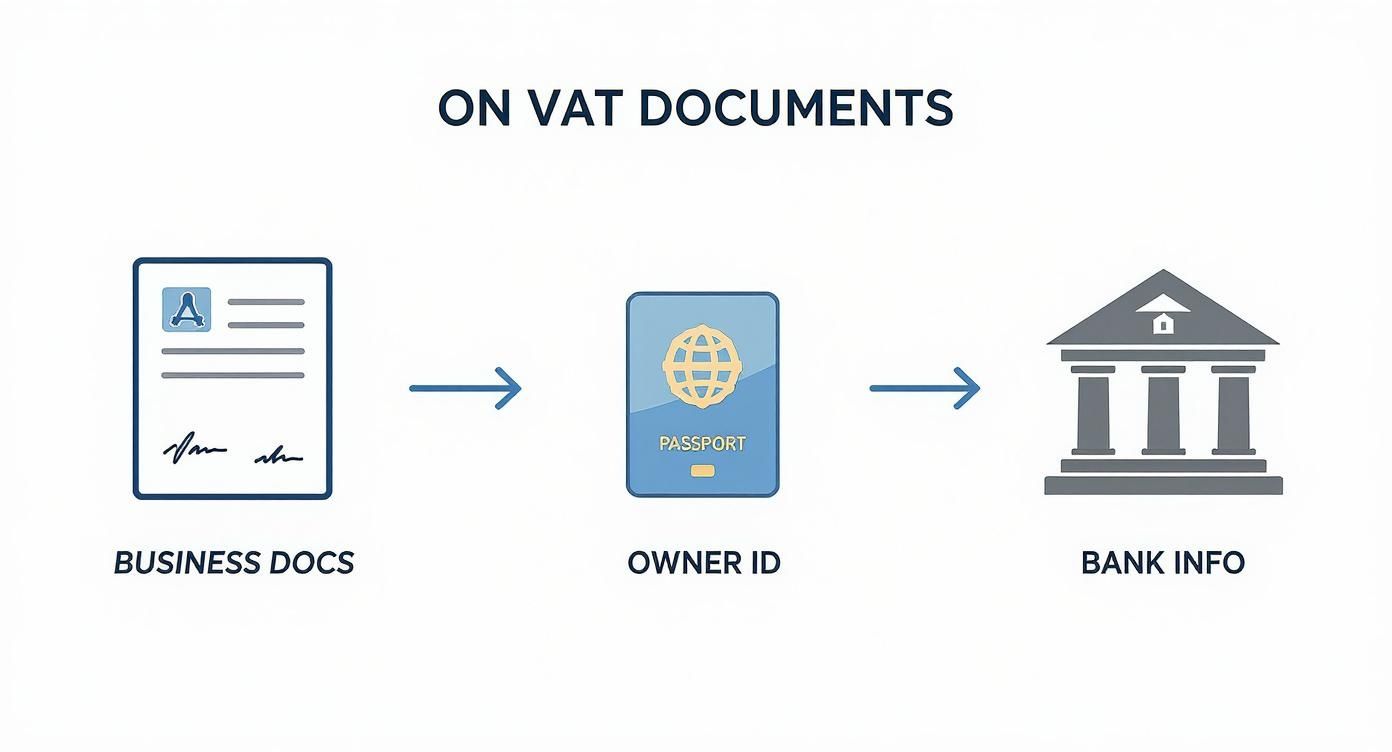

The Core Documents Every Business Needs

It doesn’t matter if you’re a sole establishment, an LLC, or a free zone company—some documents are non-negotiable. These are the absolute basics, and you should have them scanned and ready to go before you even think about logging into the FTA e-Services portal.

Here's your essential checklist:

- Valid Trade Licence: A clean, current copy of your trade or commercial licence.

- Passport Copies: Scans of the passports for the business owner and every partner.

- Emirates ID: The same goes for the Emirates ID of the owner and all partners.

- Contact Information: The mobile number and email address of the person who can legally sign off on things for the company.

These documents are what prove your business is a legitimate legal entity and who's behind it. Make sure every scan is high-quality and easy to read. A fuzzy scan where the expiry date is unreadable is just as bad as not uploading it at all.

Getting Specific to Your Business Structure

Now, beyond the universal requirements, the paperwork starts to change based on your company's legal setup. This is a common tripwire for applicants who assume it's a one-size-fits-all process. You have to provide the documents that match how your business is legally structured.

For a Limited Liability Company (LLC), for example, you'll also need to upload the Memorandum of Association (MOA). This is the legal blueprint of your company, showing the FTA exactly who the shareholders are and what they've contributed.

On the other hand, if you're running a Sole Establishment, you won't have an MOA. For this structure, the core documents like your trade licence and personal IDs are usually enough, which simplifies things a bit.

My Pro Tip: Before you start uploading, take five minutes to name your files properly. Ditch "Scan_123.pdf" for something like "Trade_Licence_2024.pdf" or "Partner_Ahmed_Passport.pdf." This simple organisational habit can save you from a world of headaches and prevent you from uploading the wrong file into the wrong slot.

Proof of Your Financial and Banking Details

The FTA needs to lock down your financial details to verify your turnover and have a formal way to handle tax matters. This part is crucial, and it requires official proof directly from your bank.

You absolutely must submit an official bank letter that confirms your company's bank account details. A screenshot from your online banking won't cut it. You need a formal letter issued by your bank, usually called a "Bank Account Confirmation Letter" or an "IBAN Letter."

This letter has to clearly state:

- The official name of your bank

- Your company’s full legal name as the account holder

- The International Bank Account Number (IBAN)

This document is the FTA's proof that the bank account you've provided actually belongs to the business applying for VAT. It's a key step to prevent fraud and ensures that if you're ever due a VAT refund, it goes to the right place.

And a final word of advice: if your registration is mandatory because you've crossed the turnover threshold, have your financial statements or a turnover declaration ready. While you might not be asked for it upfront, having it on hand can prevent major delays if the FTA asks for more proof of your eligibility.

A Walkthrough of the FTA Registration Portal

The Federal Tax Authority's (FTA) e-Services portal is your one and only stop for VAT registration. It’s a solid platform, but let’s be honest, it can feel a little intimidating the first time you log in. This guide will walk you through the entire online application, step-by-step, flagging the common sticking points to make sure you get everything right from the start.

First things first, you'll need to set up an e-Services account. It's a pretty standard sign-up process: choose a username, create a password, and punch in your contact details. Keep an eye on your inbox for a verification link to complete the setup. Once that’s done, you’re ready to log in and kick off the VAT application.

Navigating the Application Form

Once you’re in, you'll see the VAT registration form is broken down into eight main sections. It's designed to be filled out in order, but the good news is you can save your progress and come back to it later. The system walks you through each part, but the devil is in the details, so pay close attention.

The first few sections are straightforward—just your basic business details and contact info. Accuracy is everything here. Make absolutely sure the legal name of your business on the form is an exact match to what's on your trade licence. Even a tiny discrepancy can trigger a query from the FTA and bring the whole process to a halt.

Defining Your Business Activities

One of the first places people get tripped up is the "Business Activities" section. You’ll need to declare your primary business activity and list out any secondary ones. Don't be vague. Instead of simply putting "Consulting," you’re better off being specific, like "Management and IT Consulting Services."

If your business has more than one income stream, you need to list them all. This gives the FTA a clear picture of your operations and helps with their internal statistics. Any mismatch between what you declare here and what's on your trade licence is a major red flag.

The FTA’s digital-first approach has made compliance much easier, which has encouraged a huge number of voluntary registrations. You can see how well the system is working in the speed of VAT refunds, which shot past AED 3.2 billion in 2025. This points to a healthy, transparent tax system. For a deeper dive into the numbers, check out this detailed report on the UAE’s record compliance and VAT refund surge.

Uploading Your Documents Correctly

After you’ve filled in all the fields, you’ll hit the document upload stage. This is where all your prep work really pays off. The portal has specific slots for each document—your trade licence, passport copies, bank validation letter, and so on.

Here are a few essential tips I give all my clients for this stage:

- File Format: Stick to the approved formats. The portal usually accepts PDF, JPG, or PNG.

- File Size: Watch the file size. Most uploads are capped at 2MB per document, so you might need to compress larger files.

- Clarity is Key: Before you upload, open each file and double-check that it’s crystal clear and easy to read. A blurry scan is one of the top reasons for an application to be sent back.

Submitting and Tracking Your Application

The very last step is the summary page. It gives you a chance to review your entire application. Read through every single field one last time. It’s your final chance to catch a typo before you hit that submit button.

Once you’ve submitted, you’ll get an email confirmation, and you can track the application’s status right from your e-Services dashboard.

Officially, the FTA has 20 business days to review your application. During this period, they might reach out through the portal’s messaging system to ask for clarification or an extra document. This is why it’s so important to log in regularly and check for messages. A quick response from you keeps the process moving forward and gets you one step closer to approval.

Navigating Special VAT Registration Scenarios

While the standard VAT registration process is straightforward for most businesses, things can get a bit more complex once you step outside the typical local setup. The UAE's tax framework has specific rules for more intricate or international structures.

Getting to grips with these special cases is about more than just ticking a compliance box; it's about making sure your tax position and administrative load are optimised. Two of the most common situations we see are non-resident businesses making sales into the UAE and local companies with multiple related entities.

VAT Rules for Non-Resident Businesses

For businesses operating from outside the UAE, the standard registration thresholds simply don't apply. If you're a foreign company selling goods or services to customers in the UAE without a fixed establishment here, the game changes entirely.

The rule is simple and strict: you must register for VAT from your very first taxable sale. There's no AED 375,000 threshold to wait for. This ensures a level playing field and makes sure VAT is collected on imports and cross-border services. The FTA’s online portal is used for this, and once you’ve submitted all the right documents, you can expect to get your TRN within about 20 business days. This number is your ticket to operating in a VAT-compliant way, from issuing tax invoices to filing returns.

Imagine you’re an overseas digital marketing agency and you land your first client in Dubai. That first invoice triggers your mandatory registration. You can't wait for your UAE-based revenue to grow. Often, this means appointing a local tax representative to manage your VAT affairs, which can involve specific legal documents. You can find out more about the nuances from this helpful article on Value Added Tax in the UAE.

The crucial takeaway for any international business is that there's no grace period. You have to be proactive and register from day one to avoid some pretty hefty non-compliance penalties down the line.

Forming a VAT Tax Group

Does your company have multiple related entities all operating in the UAE? If so, you know that managing separate VAT registrations and filings can quickly become an administrative headache. To solve this, the FTA allows for the formation of a Tax Group. This provision lets two or more legally separate businesses be treated as a single taxable person for VAT.

It’s a strategic move that can seriously streamline your compliance. When a Tax Group is formed, it gets a single Tax Registration Number (TRN). One company is named the "representative member," and it takes on the responsibility of filing one consolidated VAT return for the entire group.

Of course, there are a few conditions you need to meet to be eligible:

- Legal Status: Every company involved must be a legal person, like an LLC.

- UAE Presence: All members need to have a place of establishment or a fixed establishment in the UAE.

- Related Parties: The businesses must be "related parties." This usually means one company controls the others, or they are all under common control.

The benefits are huge. One of the biggest advantages is that any transactions between members of the Tax Group are completely disregarded for VAT purposes. That means no VAT is charged on intra-group sales, which can massively simplify your accounting and give your cash flow a healthy boost.

To set up these kinds of formal relationships and grant authority for tax matters, it's often necessary to understand the details of a UAE Power of Attorney and its applications. Getting these special scenarios right really comes down to having a solid grasp of your own business structure and how it fits within the UAE's tax laws.

Common Mistakes and How to Avoid Costly Penalties

Getting your VAT registration sorted is a massive step forward, but the path is littered with little tripwires that can cause serious delays and, even worse, some eye-watering financial penalties. Frankly, knowing what can go wrong is just as important as knowing how to get it right.

Too many businesses treat VAT registration like another piece of admin, only to get tangled up in compliance issues down the line. From getting the turnover calculation wrong to sending in blurry documents, these common slip-ups can turn a simple process into a huge headache. Let's walk through the mistakes we see most often and how you can steer clear of them.

Miscalculating Your Taxable Turnover

This is probably the biggest and most costly error we see. Businesses often get it wrong by just looking at their net profit or only checking their turnover once a year. That’s not how the FTA sees it.

The Federal Tax Authority requires a rolling 12-month calculation. This means that at the end of every single month, you need to look back at the previous 12 months of revenue. A great quarter or a sudden spike in sales could easily tip you over the AED 375,000 mandatory threshold much sooner than you anticipated, meaning you need to act fast.

Our Pro Tip: Pop a recurring reminder in your calendar for the last day of each month to review your 12-month rolling turnover. It's a simple habit that makes sure you're never caught by surprise and can kick off the VAT registration process with plenty of time to spare.

The High Cost of Late Registration

Failing to register for VAT on time is one mistake the FTA absolutely does not take lightly. The penalty isn't just a slap on the wrist; it's a fixed AED 20,000. That’s a significant hit to your bottom line, and it's completely avoidable with a bit of forward planning.

This penalty kicks in if you don't get your application submitted within the timeframe set by the law after you become liable. It’s a clear signal that keeping a close eye on your financials isn't just good business practice—it's a legal requirement.

Key UAE VAT Penalties to Avoid

To really drive home how important it is to get this right, we've put together a quick summary of the common penalties. Think of it as a financial motivation to stay on top of your VAT obligations.

| Violation | Penalty Amount (AED) |

|---|---|

| Failure to Register on Time | 20,000 |

| Failure to Submit a Tax Return | 1,000 for the first time, 2,000 for repetition |

| Incorrect Tax Return Submission | 3,000 for the first time, 5,000 for repetition |

| Failure to Keep Required Records | 10,000 for the first time, 50,000 for repetition |

As you can see, these penalties add up quickly and can escalate for repeat offences. A small oversight can easily become a major financial burden if you're not careful.

Other Common Application Slip-Ups

Beyond the big-ticket financial mistakes, a few smaller errors can still throw a spanner in the works and get your application rejected. They might seem trivial, but they cause real delays.

- Poor-Quality Documents: We’ve seen it all. Blurry, unreadable scans of trade licences or passports are an instant red flag for the FTA. Make sure every single document you upload is a crystal-clear, high-resolution copy.

- Incorrect Bank Information: Trying to use a personal bank account is a no-go. The account must be a corporate one, in your company's exact legal name. The official bank letter you submit also must show the IBAN. No exceptions.

- Misunderstanding Start Dates: This one causes a lot of confusion. You must start charging VAT from your registration's effective date, not the date you receive your TRN. These two dates can be different, so pay close attention.

By keeping these common pitfalls in mind, you can approach your VAT registration with the care it requires, setting yourself up for a smooth, penalty-free journey from start to finish.

What to Do After Receiving Your TRN

So, your Tax Registration Number (TRN) has just landed in your inbox from the Federal Tax Authority (FTA). It’s a great feeling, and a huge step forward. But it's crucial to understand that this isn't the finish line; it's the starting pistol for your ongoing VAT compliance. The real work starts now.

Your most immediate job is to start issuing proper tax invoices. From the effective date of your VAT registration, every single invoice you send out for taxable goods or services has to be fully VAT-compliant. This isn't just about tacking 5% onto your old invoice template; it’s a specific format with mandatory details.

Issuing Compliant VAT Invoices

For an invoice to be considered valid by the FTA, it has to contain several key pieces of information. If you miss anything, it can cause headaches for both you and your clients.

Every tax invoice must clearly show:

- The words "Tax Invoice" front and centre.

- Your business name, address, and your new TRN.

- The recipient's name, address, and their TRN (if they're also registered).

- A unique invoice number and the date it was issued.

- A clear description of the goods or services provided.

- The total amount due, the 5% VAT rate, and the final VAT amount charged in AED.

Getting your invoicing right from day one is non-negotiable. It's the primary evidence for all your VAT transactions and the foundation for accurate tax returns. An incorrect invoice can be rejected by your clients for VAT recovery, damaging business relationships.

Setting Up Your VAT Accounting System

With your TRN secured, the next logical step is a serious look at your bookkeeping system. Is it ready for VAT? You are now legally required to keep precise, up-to-date records that specifically track the VAT you collect from customers (output VAT) and the VAT you pay on your business expenses (input VAT).

This goes way beyond simple income and expense tracking. You need a robust system—whether that's dedicated accounting software or a professional service—that can cleanly separate these VAT amounts for easy reporting. Flawless record-keeping isn't just for filing returns; it’s your best defence in a potential FTA audit.

Many business owners find that the time and expertise required for this is better outsourced. Exploring a comprehensive company PRO services package is a smart move to get the professional accounting and compliance support you need.

Finally, you have to file your VAT returns on time. For most businesses, this is a quarterly task done through the FTA e-Services portal. You'll declare your total output and input VAT for the period and pay the difference to the authority. Don't be late—missing a filing deadline can trigger penalties starting from AED 1,000, so get those dates in your calendar and have your records ready to go well in advance.

Your UAE VAT Registration Questions, Answered

Getting into the weeds of VAT registration can feel a bit overwhelming, and it's natural for specific questions to pop up along the way. We get asked these all the time, so let's clear up a few of the most common ones.

How Long Does It Take to Get a TRN?

Once your application is in, you can typically expect the Federal Tax Authority (FTA) to review and approve it within 20 business days.

Of course, this timeline assumes everything is in perfect order. If the FTA needs to ask for more information or if your initial submission is missing something, it will naturally take longer. The absolute best way to avoid delays is to make sure your application is complete and accurate right from the start.

Can I De-Register for VAT?

Yes, you can, but only under certain conditions. You can apply to de-register if your business stops making taxable supplies altogether. Alternatively, if your turnover drops below the voluntary registration threshold of AED 187,500 and stays there for a full 12-month period, you can also apply.

One key point to remember: If you registered voluntarily, you're locked in for at least 12 months. The FTA puts this rule in place to stop businesses from jumping in and out of the tax system.

What Happens If I Fail to Register on Time?

This is a situation you really want to avoid. The penalty for late registration is a hefty AED 20,000. On top of that significant fine, you’ll also be held responsible for paying all the VAT you should have collected from the date you were legally required to be registered.

Making sure you handle VAT correctly is a cornerstone of running a successful business in the UAE. At Smart Classic Business Hub, we live and breathe this stuff. We offer expert VAT registration, accounting, and advisory services so you can stay compliant without the headache, leaving you free to focus on what you do best: growing your business.

Contact us today to secure your peace of mind.

Article created using Outrank