So, you’ve secured your UAE trade licence. Well done. That’s a huge first step. But what comes next is arguably just as critical for building a real, sustainable business here: opening your corporate bank account.

This isn't just another box to tick. Think of it as the foundation of your company's financial credibility and your key to operating legally and efficiently in this dynamic business hub.

Why You Absolutely Need a UAE Business Bank Account

Getting a dedicated business account is non-negotiable. It creates a clean, clear line between your personal money and your company's finances. Why does that matter so much? It’s fundamental for protecting your personal assets, making your bookkeeping a breeze, and ensuring you’re reporting taxes accurately. Trying to run a business from a personal account is a recipe for a financial mess that can cause major headaches during audits and raise serious red flags with the authorities.

It’s All About Credibility and Trust

Imagine sending an invoice to a major client and asking them to pay into your personal account. It immediately looks unprofessional and can damage your reputation before you’ve even started. Clients, suppliers, and government bodies all expect a legitimate company to have a proper corporate banking setup. It signals that you’re serious, transparent, and here for the long haul. In the UAE, that kind of trust is everything.

Beyond perception, a business account unlocks the core functions of your daily operations:

- Getting Paid by Clients: It’s the only professional way to receive payments.

- Tracking Your Spending: You get a clear, auditable trail of every business expense.

- Building a Financial History: A well-managed account establishes a track record, which is vital if you ever want to apply for business loans or credit facilities down the line.

The UAE's banking scene is sophisticated and growing fast, thanks in part to ambitious national strategies like the 'We the UAE 2031' vision. This is a highly-banked country. In fact, recent data shows that an impressive 94% of residents have personal bank accounts, and this expectation of formal banking flows directly into the corporate world.

A business bank account isn't just a regulatory hoop to jump through—it's your official entry ticket into the UAE's formal economy. It proves to everyone that you're committed to building a compliant and lasting business here.

Ultimately, it doesn't matter if your company is Mainland, Free Zone, or Offshore; you need a business bank account. It’s a cornerstone of the many benefits of setting up a business in Dubai, allowing you to manage your money correctly, stay compliant, and position your company for real growth.

Your Essential Document Checklist Before You Apply

Let's be blunt: walking into a bank meeting unprepared is the fastest way to get your application delayed, or worse, rejected outright. To open a business bank account in the UAE, you need to start thinking like a compliance officer. Banks here have a legal duty to perform thorough due diligence, so having every single document organised isn't just a nice-to-have—it's mandatory.

Think of this as your pre-flight check. Getting all your paperwork in order before you even think about booking an appointment shows the bank you're serious and will massively speed up the process. The documents fall into two buckets: papers for the company itself, and papers for the people behind it.

Corporate Documents Your Business Will Need

The specific company paperwork you'll need hinges on where your business is registered—Mainland, Free Zone, or Offshore. Each jurisdiction has its own quirks because their legal structures and regulators are different. Banks pore over these documents to confirm your company's legal status, who owns it, and what it's approved to do.

No matter your company type, you'll need the bank's application form, fully completed and stamped. But beyond that, here are the core documents you can't do without:

- Valid Trade Licence: This is non-negotiable. It’s the primary proof that your company is legally registered and allowed to operate in the UAE.

- Certificate of Registration: This certificate officially confirms your business's incorporation with the relevant authority, whether that's the Department of Economy and Tourism for a Mainland setup or a specific Free Zone authority.

- Memorandum of Association (MOA) & Articles of Association (AOA): These are the legal guts of your company. They detail your business activities, outline shareholder responsibilities, and map out the ownership structure. It gives the bank a crystal-clear picture of who controls the company and what it does.

- Share Certificates: These documents put names to the numbers, officially identifying the company's owners and the percentage of shares each person holds.

- Board Resolution: This is a formal document, signed by the board of directors or shareholders, that explicitly authorises the opening of a bank account. Crucially, it also names the specific individuals who will have the power to operate it.

A company's establishment card is another vital piece of the puzzle, especially for handling visas and other official business. If you're not entirely clear on its role, our guide explains the purpose of an establishment card in the UAE in more detail.

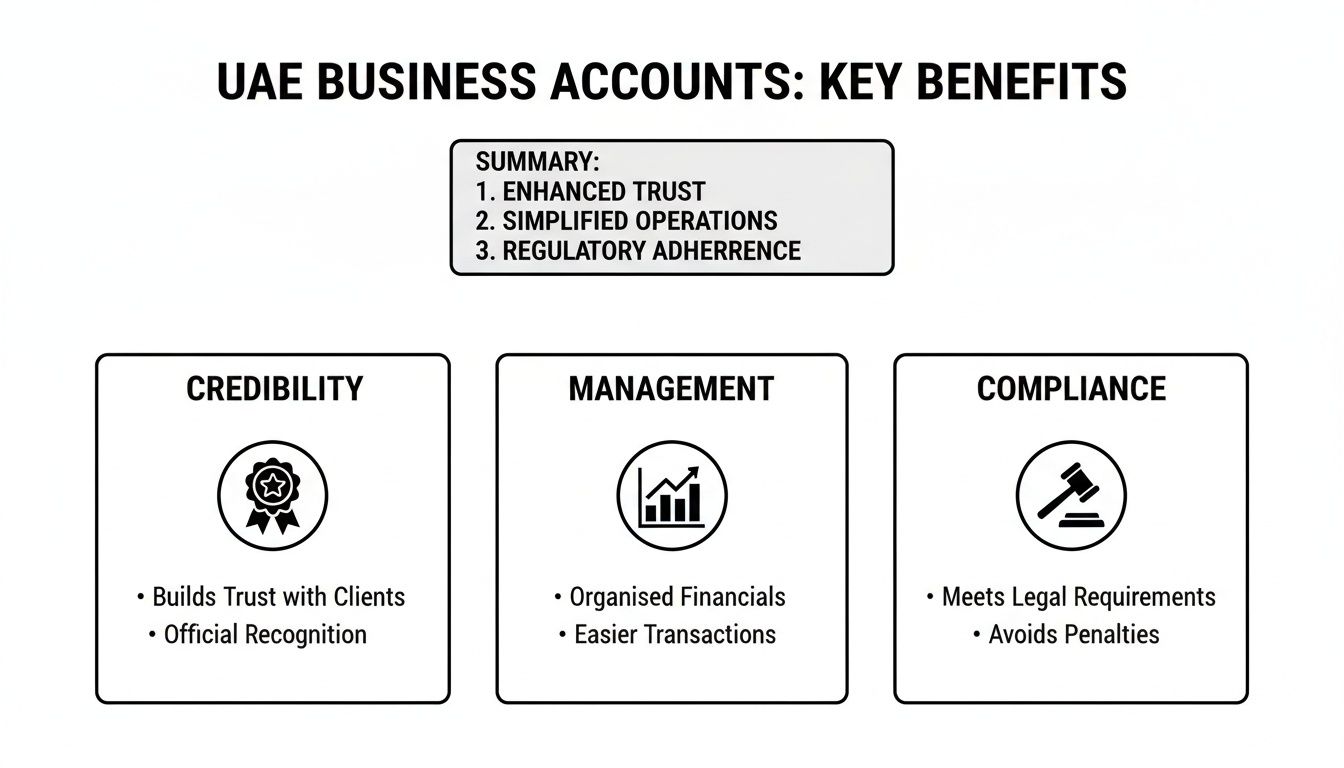

This infographic breaks down exactly why getting these formal structures right from the start is so critical for your long-term success.

Having a proper corporate account, supported by these official documents, doesn't just tick a box. It cements your business's credibility, makes financial management a breeze, and keeps you fully compliant with UAE regulations.

To make it even clearer, here’s a breakdown of the key corporate documents required, based on where your company is set up.

Required Documents by Company Type

| Document Type | Mainland Company | Free Zone Company | Offshore Company |

|---|---|---|---|

| Trade Licence | Required | Required | Not applicable |

| Certificate of Incorporation | Required | Required | Required |

| Share Certificates | Required | Required | Required |

| Memorandum of Association | Required | Required | Required |

| Board Resolution for Account Opening | Required | Required | Required |

| Establishment Card | Required | Required | Not applicable |

| Certificate of Good Standing | Not applicable | Often requested | Required |

As you can see, while there's a lot of overlap, subtle differences exist. Offshore companies, for instance, won't have a Trade Licence but will need a Certificate of Good Standing. Knowing these distinctions ahead of time saves a lot of back-and-forth.

Personal Documents for All Shareholders and Signatories

Banks don't just vet your business; they vet the people running it. This is a massive part of the Know Your Customer (KYC) rules designed to combat financial crime. Every single shareholder, manager, and authorised signatory on the account must provide a full set of personal documents.

Get ready to provide the following for each individual:

- Passport Copies: A clear, valid copy for every person involved. Make sure it’s not expiring anytime soon.

- UAE Residence Visa and Emirates ID: For any partners or signatories living in the UAE, copies of their visa page and Emirates ID are mandatory. This confirms their legal residency status.

- Proof of Address: This is usually a recent utility bill (like DEWA or Etisalat) or a tenancy contract registered in the individual's name. It absolutely must be dated within the last three months.

- Personal CV: Banks often ask for a brief CV from the main account signatory or general manager. They want to see professional background and experience that's relevant to the business you're running.

- Bank Reference Letter: Some banks might request a reference letter from the personal bank of a major shareholder, particularly if they are new to the UAE banking system.

Expert Tip: Don't get tripped up by the small stuff. Make sure every copy is crystal clear and every detail is perfectly legible. A blurry passport photo or an expired visa is a rookie mistake and a completely avoidable reason for your application to grind to a halt. Double-check the validity of every single document before you submit.

It might feel like a mountain of paperwork, but gathering this list is a fundamental first step. Arriving with a complete, organised file not only makes a brilliant first impression but also clears the most common hurdles that trip people up on the journey to getting their business financially up and running.

Choosing the Right Banking Partner for Your Business

Picking a bank in the UAE isn't just about finding the closest branch or the most recognisable logo. This is a strategic decision. It’s going to shape your daily operations, how you manage cash flow, and even your ability to grow. Think of your bank as the financial backbone of your company—the right one provides sturdy support, while the wrong one can cause constant friction and unexpected costs.

So, where do you start? Your business model. That's the most critical piece of the puzzle. An e-commerce startup, for instance, lives and dies by its payment gateway. Seamless integration and low transaction fees will be their top priority. A global trading company, on the other hand, couldn't care less about that; they're laser-focused on sharp foreign exchange (forex) rates and minimal fees for international transfers.

Look Beyond the Big Names

It's tempting to walk straight into the biggest local banks like Emirates NBD or First Abu Dhabi Bank, or even global players like HSBC. And while they're all solid institutions, they are not a one-size-fits-all solution. You might find that a smaller, more specialised bank offers terms and services that are a much better match for your actual needs.

Before you even think about signing an application, you need to do a bit of homework. Compare your options across these key points:

- Minimum Balance Requirements: This is a big one. Banks here can require you to keep an average monthly balance anywhere from AED 25,000 to over AED 250,000. If you dip below that threshold, you'll get hit with hefty penalty fees that can slowly bleed your profits dry.

- Account Maintenance Fees: Don't overlook the fixed monthly or annual charges. Some banks will waive them if you maintain the minimum balance, but that's not always the case. Get it in writing.

- International Transfer Fees: Planning to send money or get paid from abroad? You need to dig into the fees for SWIFT transfers. The difference between banks can be staggering.

- Digital Banking Platform: In this day and age, a clunky online portal is a dealbreaker. How user-friendly is their website and mobile app? A poorly designed system can turn simple tasks into a daily headache.

The UAE's banking sector is buzzing with activity. We've seen a major uptick in corporate lending and deposits lately. In the first quarter of this year alone, net loans jumped by 3.6% quarter-on-quarter, driven by strong demand from businesses. This tells us the economy is healthy and banks are eager to partner with legitimate companies that have their paperwork in order.

Matching Bank Features to Your Business Needs

To make a smart choice, you have to map a bank's offerings directly to what you do every day. For example, some banks have specialist teams and faster processes for companies set up in a free zone. Our guide on business setup in a Dubai free zone digs into why this kind of specialisation can be a huge advantage.

Let's look at a couple of real-world examples:

Scenario A: The Digital Marketing Agency

This business gets paid mostly through local bank transfers and runs payroll every month. Their must-haves are pretty clear:

- A smooth online platform that handles batch salary payments (and is WPS compliant).

- Low, or even zero, fees for domestic transfers.

- A relationship manager they can actually get on the phone for quick help.

Scenario B: The Import/Export Firm

This company is juggling suppliers in Asia and customers in Europe. Their priorities look completely different:

- Multi-currency accounts (USD, EUR, AED) so they can hold funds without being forced to convert at a bad rate.

- Competitive forex rates for when they do need to convert currency.

- Fast and affordable international wire transfers.

Your choice of bank is a core business decision, not just an item on your to-do list. Find a partner whose strengths directly fuel your main activities and future plans. Don’t get distracted by shiny introductory offers; focus on the long-term relationship, the service, and the costs.

Comparing Local and International Banks

One of the first questions we get is whether to go with a local UAE bank or a big international name. Honestly, there's no single correct answer. Each has its pros and cons.

Local Banks (e.g., Emirates NBD, ADCB)

- Pros: They have branches and ATMs everywhere. They have a deep, nuanced understanding of the local market and regulations, and often show more flexibility with SMEs.

- Cons: Their digital platforms can sometimes feel a bit behind the curve, and their services for foreign transactions might be pricier.

International Banks (e.g., HSBC, Standard Chartered)

- Pros: Their online banking experience is often top-notch. They have a powerful global network that makes international business much smoother, and their multi-currency options are usually better.

- Cons: The flip side is that they can have much stricter eligibility rules and demand higher minimum balances. They might also be less willing to take a chance on smaller or newer businesses.

Ultimately, you're not just looking for a place to park your money. You're looking for a bank that makes it easier to run and grow your business. If you carefully weigh these factors against your own unique situation, you’ll be able to confidently open an account that will serve you well for years to come.

Submitting Your Application and Facing the Interview

Alright, you’ve done the heavy lifting. Your documents are in order, and you've picked the bank that feels like the right partner for your business. This is where all that prep work really starts to shine, transforming what could be a nerve-wracking process into a manageable one. The journey isn't just about handing over a stack of papers; it's about building a relationship and proving your business is the real deal.

First up is getting your application package in front of the bank. While online portals are common, we’ve consistently seen better, faster results by submitting in person with a dedicated relationship manager. It puts a human face to your name right from the start. This simple step can help you clear up any small questions on the spot, preventing minor misunderstandings from snowballing into major delays down the line.

The All-Important KYC Interview

Once the bank has your documents, they’ll schedule a Know Your Customer (KYC) interview. Don't mistake this for a simple box-ticking exercise; it's the heart of their due diligence. The bank’s goal is straightforward: they need to understand your business, figure out its risk level, and make sure everything is legitimate and above board.

Your goal is just as clear: present your business confidently and professionally. The bank manager is looking for a credible entrepreneur with a solid plan. Think of it less as an interrogation and more as a professional conversation. They are essentially looking for reasons to write a positive internal report recommending your company for an account.

Expect them to dig into the nitty-gritty of your operations.

- Your Business Model: Be ready to explain precisely how you make money. Who are you selling to? What are your products or services?

- Transaction Profile: They'll ask about the money flow. What's your expected monthly turnover? Where are funds coming from—local clients, international wire transfers?

- Source of Funds: This is a big one. You need to be crystal clear about where your initial share capital and any future funding is coming from.

- Economic Substance: Why the UAE? The bank needs to see a genuine business reason for you to be here, not just a mailbox for tax purposes.

Your ability to clearly and logically explain your business plan during the KYC interview is often the single most important factor. Prepare concise, confident answers that show you truly understand your market and your numbers.

Presenting Your Business Like a Pro

Confidence is a byproduct of preparation. Before you walk into that meeting, practise a simple, two-minute summary of your business. This "elevator pitch" should cover what you do, who you serve, and why you’re set up for success. Having this down cold helps you kick off the conversation on a strong, professional note.

Here’s a tip: bring a brief business plan or even just a one-page executive summary, even if they didn't ask for it. It's a proactive move that screams professionalism and gives the bank manager a tangible document to understand your vision. It shows you’re serious and have thought through your strategy, which goes a long way in building trust.

How Long Does Approval Really Take?

It’s crucial to have realistic expectations about the timeline. While some slick digital banks might promise quick turnarounds, the reality for most established banks is a bit more measured. The time it takes is directly tied to how complex your company structure is and how busy the bank's compliance team is at that moment.

- Simple Setup: For something like a single-shareholder company in a low-risk industry, you’re typically looking at 2 to 4 weeks from submission to account activation.

- Complex Setup: If you have multiple corporate shareholders or deal with international trade, it can easily stretch to 1 to 3 months as the bank conducts deeper checks.

The most common culprit for delays? Incomplete paperwork or slow replies to follow-up questions from the compliance department. This is exactly where having a consultant like Smart Classic Business Hub in your corner makes a huge difference. We make sure the application is perfect from day one and manage all bank communications, cutting down the waiting game so you can get your business up and running faster.

Common Application Roadblocks and How to Avoid Them

Even with the most organised paperwork, opening a business bank account in the UAE can sometimes hit a snag. Getting rejected is frustrating, but I can tell you from experience, it’s rarely a random decision. UAE banks operate within a highly stable and well-regulated financial world, and their strict due diligence is all about protecting that stability.

It helps to think of your application less like a request and more like a business proposal to the bank. You have to convince them you’re a good bet.

So, why are they so cautious? The UAE's banking sector is a global powerhouse. Fitch Ratings recently noted that local banks hit a record high in annual profits, boasting a 19.1% return on average equity. To keep up this performance and manage risk, banks scrutinise every application to maintain their strong asset quality. You can dive deeper into the strength of the UAE banking sector and its performance metrics on FitchRatings.com.

This intense scrutiny creates common roadblocks. The good news? Most of them are entirely avoidable if you know what to look for. Let's walk through the most frequent issues I see and how you can steer clear of them.

Unclear Business Model or Vague Projections

One of the biggest red flags for a bank is an owner who can’t clearly explain what their company does and how it will make money. If your relationship manager is confused about your revenue streams, they can't effectively argue your case with their compliance team.

- The Roadblock: You describe your business as a "global consultancy" or a "digital solutions provider." Honestly, these terms are too vague. They don't tell the bank anything concrete about your day-to-day activities or where your money is coming from.

- The Solution: Get specific. Instead of "consultancy," explain, "We provide supply chain optimisation consulting for manufacturing firms in the GCC." Rather than "digital solutions," say, "We develop and sell a SaaS-based inventory management platform for retail businesses." A clear, concise business description builds immediate confidence.

Perceived High-Risk Activities

Banks have a list of industries and transaction types they consider "high-risk" because of their potential connection to money laundering or financial crime. This doesn't mean it's impossible to get an account, but you will face a much tougher review.

Some commonly flagged activities include:

- General trading with a wide, unrelated mix of goods.

- Businesses that deal heavily in cash.

- Companies involved with cryptocurrency or precious metals.

- Operations with frequent large payments to and from high-risk countries.

The Solution: If your business touches on any of these areas, transparency is your best friend. Prepare a detailed business plan that justifies your model and clearly outlines your anti-money laundering (AML) controls. You need to show the bank you understand the risks and have solid processes to manage them.

A classic mistake I see is a trade licence that lists too many unrelated activities, like "real estate management" and "textile trading" on the same licence. To a bank, this signals a lack of focus and can be perceived as high-risk. Make sure your licensed activities are specific and directly related to what your business actually does.

Lacking Economic Substance in the UAE

Banks need to be sure your UAE company is a real, operational business—not just a "paper" company set up for tax benefits. This concept is known as economic substance, and failing to prove you have a genuine presence here is a common reason for rejection.

- The Roadblock: Your company has a virtual office address, no local staff, and all shareholders live abroad. From the bank's perspective, there’s no real tie to the UAE.

- The Solution: Proving substance is absolutely critical. A physical office lease (not just a flexi-desk), a UAE resident visa for a manager or shareholder, and a local phone number are all powerful signals of a legitimate operation. It shows the bank you're genuinely invested in the local economy.

Complex or Opaque Shareholder Structures

Banks must know exactly who owns and controls a company. If your ownership structure is overly complicated with multiple layers, it sends up immediate red flags for the compliance department.

- The Roadblock: Your company is owned by another company, which is in turn owned by a trust registered in another country. This maze-like structure makes it incredibly difficult for the bank to identify the Ultimate Beneficial Owner (UBO).

- The Solution: Simplify wherever you can. Be ready to provide a complete ownership chart that traces the structure all the way back to the individual people who own it. You'll need to submit full documentation for every single corporate entity in that chain. Yes, it can be a lot of work, but providing this information upfront can save you weeks of frustrating back-and-forth with the bank.

Ultimately, getting your business bank account approved is all about thinking ahead. Anticipate the bank's questions and concerns, and address them before they become problems. When you present a clear, transparent, and well-documented case, you turn potential roadblocks into mere speed bumps on your way to getting that account open.

Your Top Questions About UAE Business Banking Answered

Even with a perfectly prepared stack of documents, the world of UAE business banking can throw a few curveballs. We've been through this process hundreds of times with our clients, so we know exactly where the common sticking points are.

Think of this as a conversation about the things that aren't always clear in the official guidelines. We're tackling the real-world questions we hear every single day to save you time and frustration.

Can I Open a Business Account Without a UAE Residency Visa?

Let's get straight to the point: it's incredibly difficult, and we almost never recommend trying.

While you might hear whispers about "non-resident" accounts, they are a rarity and come with some serious strings attached. The vast majority of reputable UAE banks have a non-negotiable rule: at least one signatory on the account must hold a valid UAE residency visa.

Why are they so strict about this? For a bank, your residency visa is proof of your commitment to the UAE. It demonstrates genuine economic substance and shows you have a real stake in the country, which significantly lowers their risk.

An important heads-up: The few non-resident accounts that do exist often demand exceptionally high minimum balances (think AED 500,000 or more), offer limited functionality, and put you under an even more intense compliance microscope.

The smoothest, fastest, and most reliable path is to ensure a key partner or director has their residency sorted. This is precisely why at Smart Classic Business Hub, we often handle visa processing and company formation together. They are two sides of the same coin for successful banking.

What Is a Typical Minimum Balance Requirement?

This is the million-dirham question, isn't it? The truth is, there's no single answer. The minimum balance requirement exists on a spectrum, influenced by the bank you choose, the account type, and their assessment of your business.

You'll find some of the newer digital banks wooing startups with zero-balance accounts. While tempting, these often come with trade-offs like higher per-transaction fees or a more limited service menu. For most established, traditional banks, it’s best to plan for these ranges:

- Standard SME Accounts: Be prepared to maintain an average monthly balance somewhere between AED 50,000 and AED 100,000.

- Premium Corporate Accounts: For businesses that need more sophisticated tools and services, this figure can easily jump to AED 250,000 or higher.

The most critical detail to confirm is how they calculate this. Is it an "average monthly balance" or a "minimum balance at all times"? The difference matters. Falling below the required threshold can trigger surprisingly high monthly penalty fees, so getting this clear from the start is vital for managing your cash flow.

How Long Does It Really Take to Open an Account?

It's crucial to set realistic expectations here. Ignore the flashy ads promising instant approvals. The reality of UAE banking is a more measured, compliance-driven process. The timeline depends heavily on your company structure, your specific business activities, and how busy the bank's compliance department is.

In a best-case scenario—say, a simple single-shareholder LLC with every single document perfectly in order—you might be looking at 2 to 4 weeks.

However, if your situation is more complex, the clock ticks much slower. For a company with corporate shareholders in different countries or one operating in a sector that demands extra scrutiny (like general trading), the process can easily stretch to 2 or even 3 months. From our experience, the biggest hold-ups almost always come down to incomplete paperwork or delays in responding to the bank’s follow-up questions.

Navigating these details is where having an expert in your corner makes all the difference. If you're ready to open your UAE business bank account without the guesswork, our team at Smart Classic Business Hub is here to streamline the entire process. We make sure your application is flawless from the get-go, handle all the back-and-forth with the bank, and clear the path for a successful opening.