You've found the UAE opportunity. The company structure is taking shape, the funds are ready, and you're thinking about invoices, suppliers, property, payroll, or investment flows. Then the banking question lands on your desk and everything slows down.

That's where most new investors get frustrated. Not because a UAE bank account for non resident applicants is impossible, but because the process isn't uniform. One bank will entertain the application. Another will only consider a premium relationship. A third may accept the profile in principle but still stall over source-of-funds questions.

The main issue isn't usually eligibility alone. It's whether your file makes sense to a compliance officer who has to justify onboarding you. That's the part official bank pages rarely explain in plain language.

Securing Your Financial Gateway to the UAE

A non-resident usually starts with a simple question: can I open a UAE bank account without residency? The practical answer is yes, but that answer is only useful once you understand the hidden filter behind it. Banks don't assess these applications as a retail formality. They assess them as a risk file.

What confuses applicants is that the document list looks familiar, but the outcome varies sharply by bank. Recent guidance notes that requirements differ materially by institution, and some banks ask for a passport, UAE entry stamp or visa copy, 3 to 6 months of statements, a bank reference letter, proof of foreign address, and a source-of-funds explanation, while others are stricter on minimum relationship size and may only offer savings-style products. The same guidance also notes that minimum balance thresholds for personal non-resident accounts can range from AED 25,000 to AED 500,000 depending on the bank and relationship type, according to this UAE non-resident banking guide.

That's why random applications fail. The applicant assumes the process is administrative. The bank treats it as investigative.

Why the process feels inconsistent

Banks aren't just checking identity. They want a coherent story:

- Why the UAE: Investment, property holding, regional business, treasury diversification, or personal wealth management.

- Why this bank: Service level, account type, branch support, international transfers, or relationship fit.

- Why these funds: Salary, dividends, retained earnings, asset sale proceeds, consulting income, or another lawful source that can be evidenced.

- Why now: Recent market entry, a transaction pipeline, a company launch, or portfolio reorganisation.

Practical rule: The biggest bottleneck is often compliance packaging, not formal eligibility.

Applicants dealing with multiple jurisdictions often face the same pattern elsewhere. If you're comparing regional approaches, this guide on navigating Israeli bank accounts is useful because it shows how cross-border banking often turns on documentation quality rather than headline eligibility.

The unwritten rule most people miss

A bank wants to know whether you'll look understandable six months after the account opens. If your expected transfers, profile, and documents align, the file feels safe. If the profile is vague, the same documents suddenly look weak.

That's the mindset to carry through the rest of the process. You're not just opening an account. You're proving that your banking behaviour will be legible from day one.

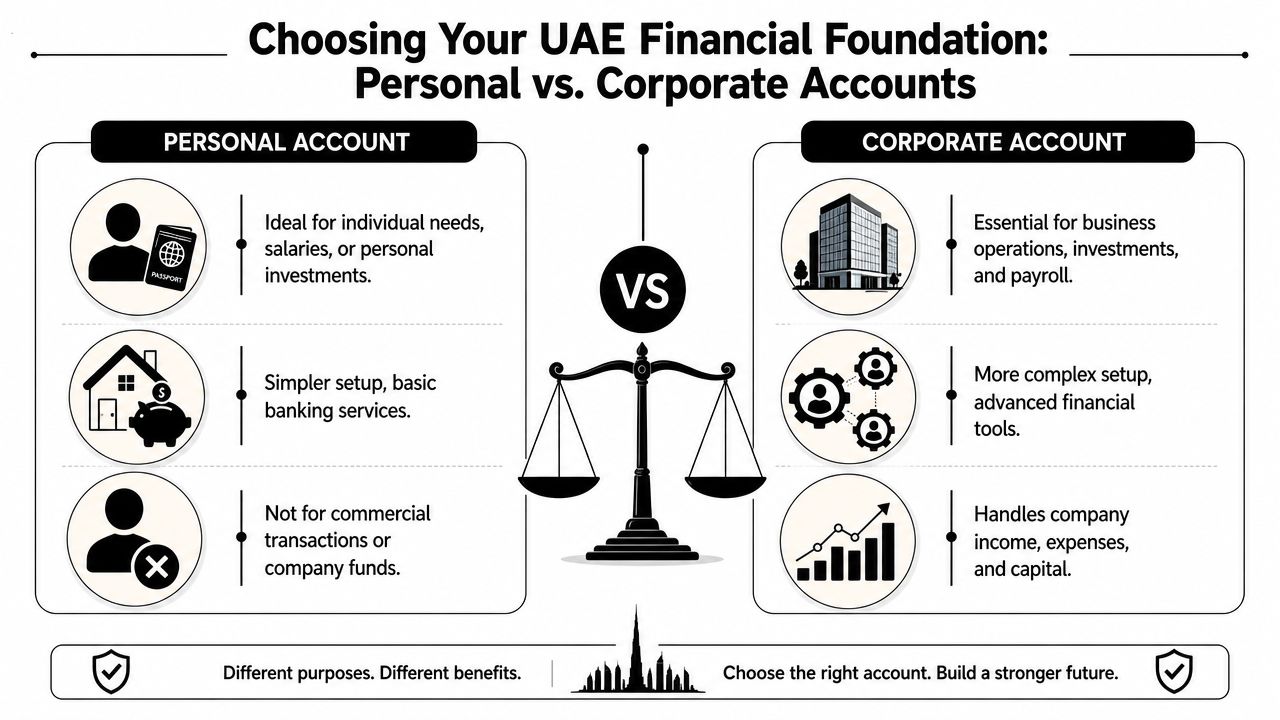

The Two Paths Personal Versus Corporate Accounts

The first decision is basic but important. Are you trying to bank as an individual, or are you trying to bank a business structure? Many applicants blur the two and create avoidable problems.

The UAE does allow non-residents to hold bank accounts, and the regulatory framework has long recognised access for non-resident entities. The UAE banking classification captured in the AFP country report states that non-resident entities may hold fully convertible AED bank accounts and foreign currency bank accounts within the UAE, while market practice for individuals is more restrictive, with many banks offering savings-type products rather than full current accounts and commonly limiting cheque books and overdrafts for non-residents, as outlined in the AFP UAE country report.

What a personal non-resident account is really for

A personal non-resident account suits people managing personal funds. That might include holding capital for future relocation, receiving investment-related transfers, maintaining a UAE banking presence, or handling personal expenditure tied to visits or assets.

It usually isn't the right tool for active commercial operations. If you plan to invoice clients, pay suppliers, or run company turnover through the account, you're moving into territory banks will treat differently.

A personal account can open the door. It usually can't replace a proper operating account for business activity.

What a corporate account is really for

A corporate account is the right route if the underlying activity is business. That includes a UAE mainland company, free zone company, or another legal entity with genuine business purpose and supporting documents.

Corporate banking is harder because the bank is assessing more than one person. It wants to understand the company, shareholders, expected counterparties, transaction flows, and commercial logic. But if your objective is actual business in the UAE, the corporate path is usually cleaner in the long run.

Personal vs Corporate Non-Resident Account Comparison

| Feature | Personal Non-Resident Account | Corporate Non-Resident Account |

|---|---|---|

| Primary purpose | Personal savings, personal investment support, private fund holding | Business operations, company income, supplier payments, payroll, capital deployment |

| Typical product style | Often savings-type or limited-function account | Operational business account, subject to broader review |

| Residency sensitivity | Higher sensitivity for features and product access | Focus shifts more to entity substance, ownership, and business rationale |

| Cheque book and overdraft access | Commonly limited or unavailable without residency | Depends on bank and company profile |

| Currency access | Depends on bank product | Can support AED and foreign currency structures where approved |

| Compliance focus | Personal source of funds, address, banking history, profile clarity | Corporate activity, ownership chain, business model, counterparties, source of funds |

| Best suited to | Passive investor, property holder, frequent visitor, individual wealth planning | Founder, trading company, consultancy, holding company, operating business |

| Main risk if misused | Business-like activity can trigger scrutiny | Weak substance or unclear model can delay or block approval |

The practical trade-off

A lot of founders try the personal route first because it feels simpler. Sometimes it is simpler. But if the primary intention is business turnover, that shortcut often creates future friction.

Choose based on actual use:

- Choose personal if the funds are yours and the activity is personal.

- Choose corporate if the account will touch company revenue, expenses, or investment flows.

- Don't mix the two just to get an account faster. Banks notice inconsistent transaction patterns quickly.

The cleanest applications are the ones where account purpose, account holder, and future transaction behaviour all match.

Your Essential Document Checklist for Approval

Most rejected files aren't rejected because one document is missing. They're rejected because the file doesn't answer the bank's internal question: is this applicant bankable and understandable?

That's why I tell clients to stop thinking in terms of a “document list” and start building a compliance pack. The pack has one job. It must allow the relationship manager and compliance team to explain who you are, where your money comes from, and what this account will be used for without chasing you repeatedly.

Public guidance and market practice show that non-resident applications are increasingly segmented by risk tier and bank appetite, with reported minimum-balance bands of roughly AED 25,000 and above for some non-resident or priority offerings, some account types requiring AED 30,000 to AED 60,000, and higher-tier relationships requiring AED 250,000 or more. The same market guidance highlights that stronger files show a stable six-month account history, credible employment or business proof, and a consistent remittance pattern, as discussed in this UAE banking market guidance video.

What the bank is trying to prove

The bank wants documentary comfort around four things:

- Identity

- Address

- Source of funds

- Expected account behaviour

If your file is weak on any one of those, the application can drag or fade away.

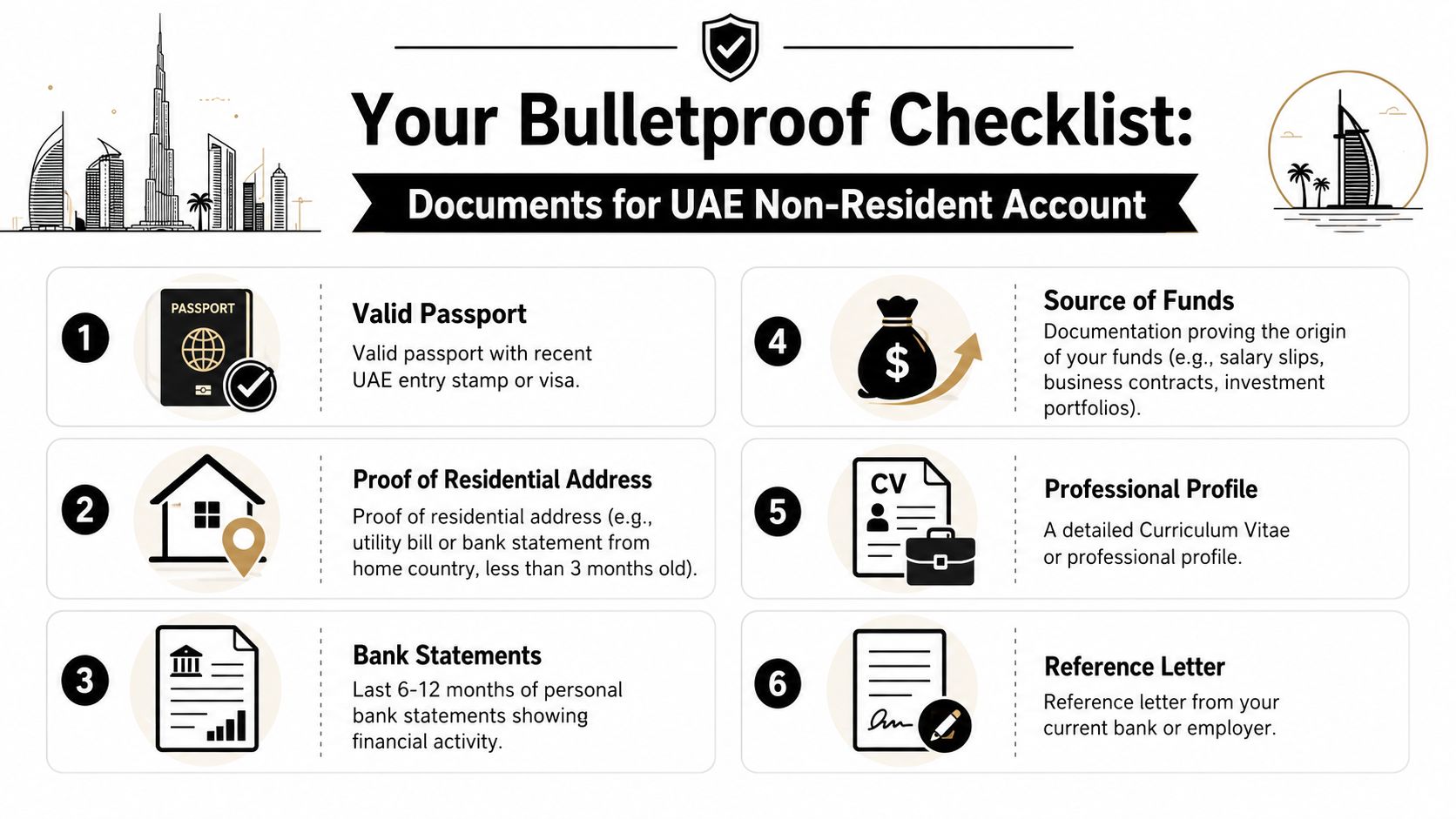

The core compliance pack

Use this as your working checklist.

Valid passport with travel evidence

A passport confirms identity. An entry stamp or visa copy helps establish that you have a real connection to the UAE process and aren't applying in the abstract.Proof of residential address

Banks want to tie you to a stable jurisdiction. A utility bill or bank correspondence is useful because it links your identity to a live address.Recent personal bank statements

These are not a formality. They show transaction behaviour, income consistency, and whether your declared profile matches what your money reflects.Bank reference letter

This gives comfort that another institution already knows you as a customer. It won't rescue a weak file, but it strengthens a coherent one.Source-of-funds evidence

Many applications falter at this requirement. Salary slips, business contracts, dividend records, investment statements, or sale documents should support the story you tell.Professional background or profile summary

A short CV, business profile, or shareholder summary helps the bank understand how your wealth was built and why the UAE connection is logical.

The unwritten rule on statements

Statements are read for pattern, not just balance. A large balance helps, but clarity matters more. If the credits are irregular, unexplained, or coming from mixed sources with no narrative, the compliance team will hesitate.

If you need to organise statement files before submission, tools built for bank statement data extraction can help you clean up and review transaction history so the final pack is easier for both you and the bank to understand.

Banks are not impressed by volume alone. They're reassured by traceability.

How to write a source-of-funds note that works

Keep it short. Keep it factual. Match it to the documents.

A good note explains:

- Primary income source such as employment, consulting, dividends, or business ownership

- How funds accumulated over time

- Why funds may be transferred to the UAE

- What type of account activity is expected

Bad versions are vague. “I am a businessman with multiple interests” tells compliance nothing. “Funds derive from salary and retained dividends from a consultancy I own, supported by statements and company records” is stronger because it can be checked.

Small errors that create big delays

Applicants often lose time on avoidable issues:

- Mismatched names across passport, statements, and reference letters

- Unreadable scans or cropped pages

- No explanation for large inbound transfers

- Old address documents

- A file that looks assembled in a rush rather than prepared deliberately

The best pack doesn't overwhelm the bank. It answers the obvious questions before they need to be asked.

Choosing the Right Bank for Your Needs

A weak bank choice can waste weeks even if your documents are perfect. Non-resident banking in the UAE is a formal market segment, but it isn't a uniform one.

The clearest signal from the market is that major institutions do accept non-resident clients through defined pathways. Emirates NBD publicly lists a non-resident route and asks for a valid passport, visa page, proof of address, and reference documentation, while RAKBANK also offers a dedicated non-resident bank account. At the same time, market guidance reports minimum deposit expectations for personal non-resident accounts ranging from AED 25,000 to AED 500,000, and physical presence is often needed to complete onboarding, as reflected in RAKBANK's non-resident account information.

That tells you two things immediately. First, this is a real banking category. Second, banks treat it as a premium and compliance-heavy service.

Local banks

Large UAE banks usually give the strongest domestic infrastructure. Branch networks are broader, local transfers are straightforward, and relationship managers understand UAE-linked use cases well.

But local banks also tend to be strict on file quality. If your profile is thin, your UAE rationale is weak, or your balances don't fit the bank's appetite, the file may never move far.

Best fit: investors, established professionals, founders with clear UAE plans, and applicants who can present a polished compliance pack.

International banks with UAE presence

These banks can make sense if your financial life is already international. If you hold relationships across multiple jurisdictions, an international bank may better understand the cross-border logic behind the account.

The trade-off is that global policy can be just as restrictive as local caution. Some applicants assume a foreign profile automatically plays better with an international brand. Sometimes it does. Sometimes it just means more layers of review.

Digital-first and newer banking channels

These options can be attractive for convenience, but non-residents should be realistic. Digital interfaces don't remove underlying compliance duties. They may simplify contact and submission, but the hard questions still exist.

Where they help is speed of communication and a cleaner onboarding experience when the profile already fits. Where they don't help is rescuing a weak file.

A practical shortlist method

Before applying anywhere, screen banks against these points:

Product fit

Are they offering a true non-resident pathway, or are you trying to force a resident-style product?Balance comfort

Can you comfortably meet the likely relationship expectations without stretching?Profile fit

Does your background match the bank's usual client profile? Entrepreneur, salaried professional, investor, or high-net-worth individual?Service expectation

Do you need basic holding and transfers, or a more active banking relationship?

If you want a broad view of institutions to research, this overview of the top bank in UAE is a useful starting point for comparing the market before you narrow your list.

The best bank isn't the biggest name. It's the institution where your profile makes immediate sense.

What usually works and what doesn't

Works well: coherent background, legitimate reason for UAE banking, established financial history, and willingness to attend in person.

Works poorly: speculative applications, unclear business stories, inconsistent statements, and trying to pitch the same file to every bank as if they all assess risk the same way.

Bank selection is not a branding exercise. It's risk matching.

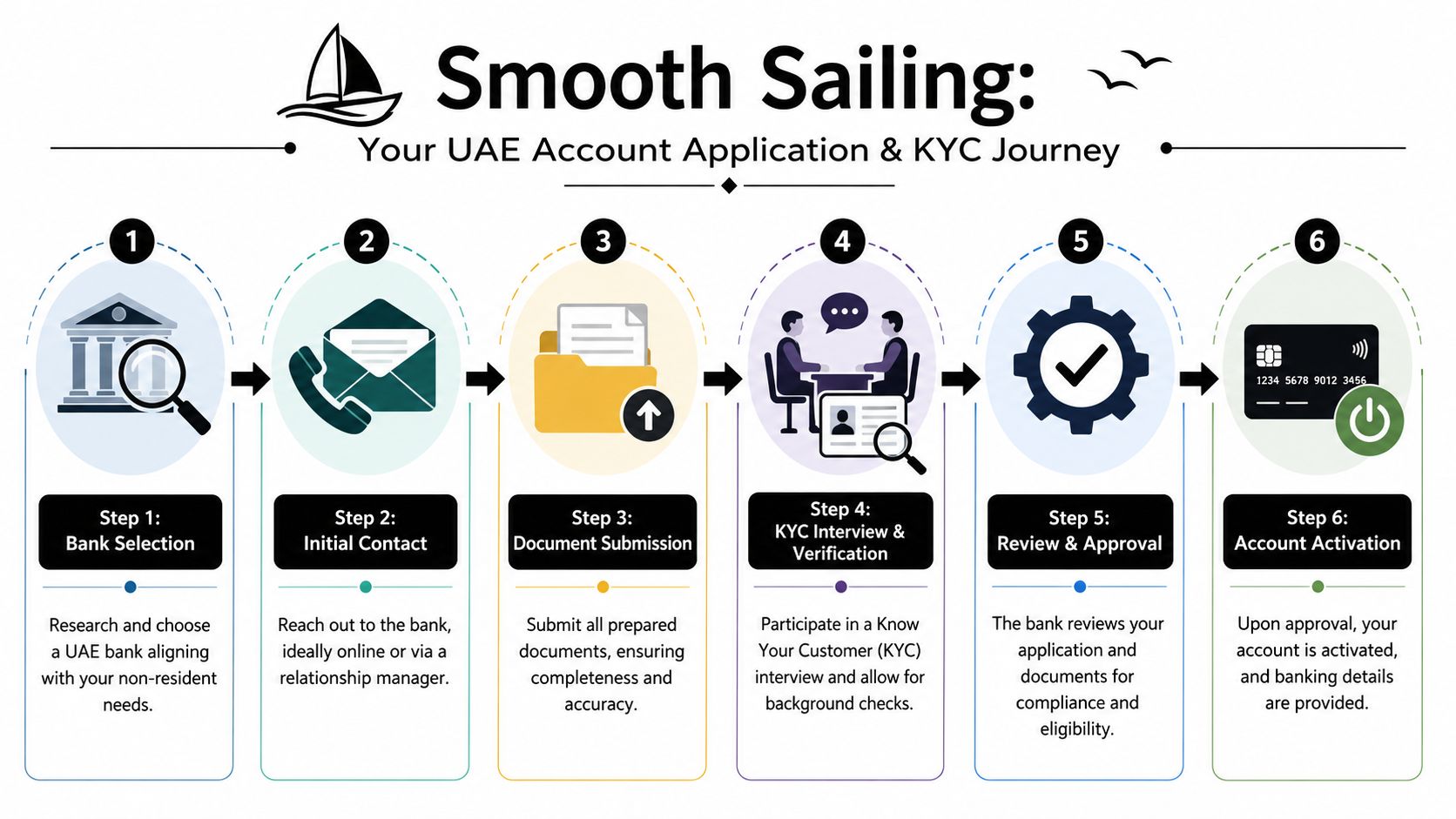

Navigating the Application and KYC Process

Once you've chosen the bank, the process becomes much more human. Forms matter, but conversations matter more. The bank wants to hear that your spoken explanation matches the paperwork in front of them.

The practical workflow in UAE market guidance is consistent: pre-screen the bank's non-resident policy, prepare a compliance pack, complete KYC and AML verification in person, and expect additional suitability checks if you have no local income or residence status. The same guidance notes that approvals for accepted non-resident personal files commonly take about 1 to 2 weeks once a full file is in, although extra document requests can extend that timeline, according to this UAE non-resident application guide.

How the journey usually unfolds

The first exchange is often informal. You speak to a relationship manager, submit preliminary documents, and get a sense of whether the bank sees your file as viable.

If the early reaction is positive, the bank asks for the full pack. That's the point where many applicants think approval is near. It usually isn't. It means the file has entered review.

Then comes the KYC stage. At this point, the unwritten rules become visible.

Questions you should expect

Banks often probe these areas during review or interview:

- Why do you want a UAE account as a non-resident

- What is the source of the funds

- What transactions do you expect to make

- Do you have UAE business, property, or investment ties

- Are you planning to relocate or remain overseas

- Who will send money to the account and why

The right answer is never the most impressive one. It's the most verifiable one.

If your answer sounds polished but can't be backed by documents, compliance will treat it as weak.

A common failure pattern

An applicant says the funds are from “business income”. The statements show mixed credits from individuals, platforms, and unrelated entities. There's no note explaining the pattern. Compliance can't map the story, so the file stalls.

Another applicant gives a narrower explanation. Salary from one employer, dividends from one company, and planned UAE transfers for investment holding. The documents line up. The file feels easier to defend internally.

That's why vague source-of-funds descriptions are dangerous. The problem isn't that the bank wants more paperwork for sport. The problem is that AML review depends on traceability.

Practical preparation before the meeting

These steps help more than people expect:

Rehearse your account purpose

Say it in two sentences. If it takes ten, it's still unclear.Align your numbers and story

Large incoming transfers on your statements should be explainable from memory and from documents.Bring backup documents physically

Even if you uploaded them already, branch staff often move faster when you can show them immediately.Prepare for local contact issues

Banks may send OTPs or verification messages during onboarding. If you need a stopgap option while travelling, services that let you get a temporary phone number can be useful for general account setup logistics, though you should always make sure your contact method complies with the bank's requirements.

If you're looking at the broader setup journey around banking, company formation, and account readiness, this guide to opening a bank account in Dubai adds useful context on how banking fits into the wider market entry process.

What to do if the bank asks for more

Don't argue. Clarify.

A request for more documents doesn't automatically mean rejection. It often means the file is active but unresolved. Respond with a neat, indexed reply. Answer each question directly. Attach only the documents that address that specific concern.

Messy follow-up is one of the fastest ways to turn an open file into a dormant one.

Exploring Alternatives and Next Steps

Sometimes a traditional bank account doesn't open on your preferred timeline. That doesn't mean the UAE plan stops. It means you need a staged approach.

For some founders and foreign investors, a fintech or payment platform can bridge the gap while the full banking relationship is still being built. These options can help with collections, transfers, and operational continuity when a conventional bank is still reviewing a case. They won't replace every banking function, but they can keep a business moving.

When an alternative makes sense

An alternative route is worth considering if:

- You need to start transacting quickly

- Your traditional application is delayed

- You are still building UAE substance

- You want a temporary operating layer while pursuing a full bank account

That's especially relevant for new market entrants who are still assembling lease documents, staffing plans, licences, or a transaction history the bank wants to see.

Don't confuse access with permanence

A workaround should support your banking strategy, not become a permanent substitute by accident. The long-term objective is still a structure that matches your actual activity, whether that is personal wealth management, a UAE operating company, or an investment vehicle.

If your structure is offshore-led or you are assessing how cross-border ownership affects banking options, reviewing the practical issues around an offshore bank account in Dubai can help you think more clearly about what banks will expect from ownership, activity, and documentation.

The account opening is not the finish line. The real test starts after activation, when your transactions need to match the story you told during onboarding.

Once the account is live, use it carefully. Keep transaction behaviour clean. Don't introduce unexplained counterparties early. Don't mix personal and business activity. Keep records ready. The banks that approve non-residents are usually willing to maintain those relationships, but only when the customer remains easy to understand.

If you want experienced help with the banking side of UAE market entry, Smart Classic Business Hub can support the wider process around company formation, compliance preparation, and practical structuring so your application reaches the bank in a stronger, more bankable form.