You’re probably in one of two situations right now. Either you run an international business and want a cleaner structure for cross-border payments, asset holding, or group ownership, or you’re comparing UAE options and feeling that “offshore” sounds useful but also slightly opaque.

That confusion is normal. A uae offshore company is one of the most misunderstood business structures in the region because the benefits are real, but so are the limits. Many guides stop at the registration stage and make it sound like once the certificate is issued, the hard part is done. In practice, registration is only the opening move. Banking, tax position, and ongoing compliance are where good planning matters.

An Introduction to Your Global Business Structure

For the right investor, a uae offshore company works like a carefully designed legal platform. It lets you hold assets, organise international ownership, and manage non-UAE business activity from a jurisdiction known for stability, global connectivity, and business-friendly administration.

That doesn’t mean it’s a shortcut. It means it’s a structure with a specific job.

A useful way to think about it is this. If a mainland company is built for trading inside the UAE, and a free zone company often sits somewhere between local presence and international reach, an offshore company is built for activity beyond the UAE. That difference shapes everything, from tax treatment to banking expectations.

Many investors already understand this principle in other markets. If you're comparing structures across jurisdictions, Mayo Law on U.S. business entities offers a helpful parallel on why entity choice should follow business reality, not marketing language.

Practical rule: The best structure isn’t the one with the lowest setup fee. It’s the one that fits how your money moves, where your customers are, and what regulators will expect to see later.

The UAE has developed offshore options that appeal to founders, family offices, international traders, and holding structures. But the structure only works well when you understand what it is designed to do, and just as equally, what it is not designed to do.

What Is a UAE Offshore Company Really

A founder in London, Mumbai, or Singapore often reaches the same point. You do not need a shopfront in Dubai or a local sales team. You need a clean holding structure, a credible jurisdiction, and a company that can sit above assets, contracts, or investments spread across several countries. In that situation, a uae offshore company can make sense, but only if you understand what it is built to do after the registration certificate is issued.

A uae offshore company is a UAE-registered legal entity primarily used for international business activity, not direct business inside the UAE domestic market. That single point causes most of the confusion. Investors see "UAE company" and assume they are buying local market access, visa eligibility, and straightforward banking. Offshore does not deliver that package.

A better comparison is to treat it as a legal container. The container can hold shares in another business, intellectual property, overseas investments, and certain approved property interests. It can also sit in the middle of cross-border contracts where the counterparties and revenue are outside the UAE. What it does not do is replace a mainland or free zone operating company if your real commercial activity happens inside the country.

Under Regulation 14.1 of the JAFZA Offshore Companies Regulations 2018, offshore entities are set up for international operations and are restricted from carrying on business with persons resident in the UAE, except where the regulations allow it. For an investor, the practical meaning is simple. Your tax position, compliance profile, and bankability all depend on keeping the actual activity aligned with that offshore purpose.

That alignment matters more in 2026 than many setup guides admit.

Banks now ask a harder question than "Do you have a company?" They ask, "What does this company do, where does the money come from, and why is offshore the right fit?" The same issue appears later if you hope to qualify for a TRC. A company used only as a paper wrapper, with no supporting substance, records, or business rationale, can struggle long after incorporation. If banking is part of your plan, it helps to review the practical issues around a RAK offshore business account setup before choosing the structure.

What it can do well

Used properly, an offshore company is usually suited to:

- Holding shares or assets such as ownership in foreign companies, intellectual property, or family investment vehicles

- Centralising ownership where several businesses or investments need one clean parent entity

- Supporting international contracts where customers, suppliers, and income are outside the UAE

- Separating risk by placing valuable assets in a distinct legal entity rather than inside an operating business

This is why experienced investors often use offshore companies as ownership and control vehicles, not as the main engine of day-to-day trade.

Where new investors get it wrong

The usual mistake is trying to make an offshore company behave like a low-cost local company. That is where problems start. A bank may question the model. A counterparty may ask for proof of substance. A tax adviser may tell you the structure does not support the residency outcome you expected.

This quick test helps:

| Question | If the answer is yes | Offshore fit |

|---|---|---|

| Do you need to sell directly to UAE customers? | You need local market access | Poor fit |

| Do you want UAE residence visas from the company? | You need immigration functionality | Poor fit |

| Do you want a holding entity for overseas assets? | You need a legal ownership vehicle | Strong fit |

| Do you invoice non-UAE clients only? | Your revenue is international | Strong fit |

A good offshore structure follows commercial reality. If your staff, customers, and operations are in Dubai, an offshore company usually creates friction rather than saving cost. If your goal is international ownership, asset holding, or non-UAE revenue, it can be a clean and efficient tool. The key is understanding the post-registration reality early, especially banking and tax residency, because those are the points where a good structure proves itself.

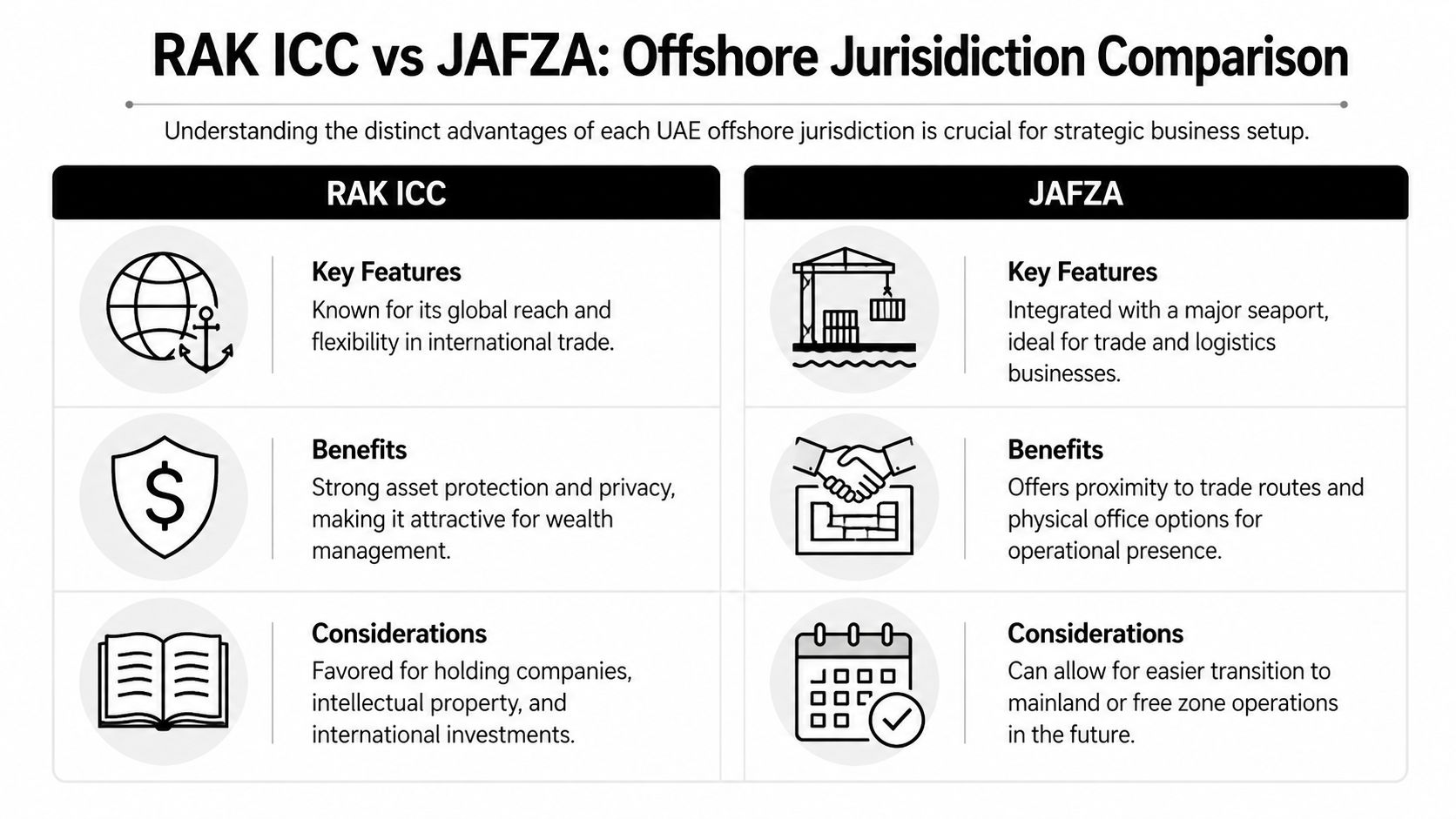

Choosing Your Jurisdiction RAK ICC vs JAFZA

You register the company. The certificate arrives. A week later, critical questions start. Will the bank accept this jurisdiction and business model? Will the structure support your later TRC plan if that becomes part of your tax strategy in 2026? That is why the RAK ICC versus JAFZA decision is not only about registration cost. It shapes what happens after incorporation.

Both jurisdictions can work for a uae offshore company. The better choice depends on what the company is meant to do in real life. If it will hold Dubai property, one answer usually stands out. If it will hold shares, own IP, or sit above foreign operating companies, the other often gives a cleaner setup with less friction.

JAFZA for Dubai property and a stronger Dubai link

JAFZA tends to attract investors who want the company tied closely to Dubai, especially where real estate is part of the plan. Trident Trust’s JAFZA offshore overview notes JAFZA’s long-established role in the emirate and highlights the features that make it a common choice for offshore structuring in Dubai, according to Trident Trust’s JAFZA offshore overview.

The practical attraction is straightforward. If legal ownership of Dubai real estate sits at the center of the structure, JAFZA is often the first jurisdiction advisers examine. For some investors, that point alone settles the decision.

Other practical points commonly associated with JAFZA include:

- 100% foreign ownership without a local partner

- A tax-neutral setup, subject to the applicable UAE tax rules and thresholds

- Incorporation often taking around 10 to 12 working days

- Company names ending in “Limited”

JAFZA can also carry more weight in conversations with counterparties who are familiar with Dubai but not with the wider UAE registry map. That does not guarantee easier banking. It can, however, make the structure easier to explain.

RAK ICC for lower cost and cleaner holding structures

RAK ICC usually appeals to investors who want an efficient ownership vehicle rather than a Dubai-linked profile. The GWS guide to Dubai and RAK offshore structures describes it as a widely used option for offshore holding and international structuring, according to the GWS guide to Dubai and RAK offshore structures.

In practice, RAK ICC is often chosen for shareholding, family asset holding, cross-border investment structures, and intellectual property ownership. It works like a holding shelf. You place ownership interests there, keep the structure legally separate, and avoid building extra UAE operating features you do not need.

Common reasons investors prefer RAK ICC include:

- 100% foreign ownership

- No physical office requirement for the offshore vehicle

- Lower entry cost in many standard cases

- A setup process that is often simpler than Dubai-based alternatives

That simplicity matters later. If your bank application already needs a clear source of funds story, group chart, contracts, and business rationale, a straightforward legal structure is easier to defend than one with extra moving parts.

Side by side decision table

| Factor | RAK ICC | JAFZA |

|---|---|---|

| Typical appeal | Cost efficiency and simpler holding structures | Dubai profile and property-led use cases |

| Starting setup cost | USD 1,950 to 2,870 (per GWS guide cited above) | USD 1,950 to 6,000+ (per Trident Trust cited above) |

| Real estate angle | Better for general holding structures | Common choice where legal ownership of Dubai real estate is a priority |

| Office requirement | No physical office required | Offshore model, registered office through approved channels |

| Investor profile | Holding companies, investment vehicles, IP owners | Property investors and owners who want a stronger Dubai link |

How to choose without making the wrong trade-off

A useful way to decide is to match the jurisdiction to the pressure points you are likely to face after registration.

If the company must own Dubai real estate, start with JAFZA.

If the company is mainly a holding vehicle for overseas assets, RAK ICC is often the cleaner answer.

If you expect a bank to ask detailed questions about commercial purpose, group structure, and supporting documents, either jurisdiction can work, but the simpler fact pattern usually performs better. Banks review the whole story, not only the incorporation certificate. A bank officer wants to see why the company exists, how money will flow, and whether the structure matches the shareholder’s profile. That is one reason many investors review practical RAK business account support options before they finalize the jurisdiction.

One more point often missed by first-time investors. Jurisdiction choice does not automatically solve TRC goals. In 2026, a Tax Residency Certificate depends on meeting the actual conditions applied to the entity and its substance profile, not on choosing a registry with a stronger brand name. If TRC planning may matter later, choose the jurisdiction that supports a defensible operating story, board control record, and compliance file.

A good rule is simple. Choose JAFZA when the Dubai connection is the point. Choose RAK ICC when efficiency and a clean holding structure are the point.

Key Benefits and Practical Limitations

The appeal of a uae offshore company is real. So is the need for restraint. This is a structure that rewards clarity and punishes wishful thinking.

Where the value sits

The strongest benefit is usually separation. You separate assets from operating risk, ownership from day-to-day business, and international income from jurisdictions that may be less stable or less efficient for holding purposes.

Investors also value privacy and control. Offshore structures are often used where owners want a formal legal vehicle without building a full operating base in the UAE. For family investors, that can support succession planning. For founders, it can tidy up cap tables and shareholding arrangements.

Another advantage is tax treatment, but this must be understood correctly. The benefit is not “pay no tax anywhere”. The benefit is that an offshore company, when used properly for non-UAE activity, can sit in a tax-neutral framework for qualifying foreign-sourced income. That’s useful, but only if the structure matches reality.

Where people overestimate it

Here is the practical scorecard many first-time investors need:

- Strong for holding. Shares, investments, and approved asset ownership fit well.

- Useful for international invoicing. This works when customers and operations sit outside the UAE.

- Weak for local trade. If you want to invoice UAE clients directly, the structure fights you.

- Weak for relocation plans. Offshore companies generally don’t solve visa and on-the-ground staffing needs.

A good fit and a bad fit

A good fit looks like this. A founder based abroad wants one company to hold shares in several non-UAE ventures and receive overseas income.

A bad fit looks like this. A consultant in Dubai wants to serve local UAE clients, rent office space, and sponsor staff visas through an offshore entity.

Key takeaway: Offshore is a specialist tool. It performs well when used for international structuring and poorly when forced into local operations.

If you need market access, residency, or a physical operating base, you’re usually looking at a different UAE structure.

The Step-by-Step Formation Process

A first-time investor often expects the hard part to be getting the certificate. In practice, the stronger question is whether the file you build on day one will still make sense to a bank, a tax adviser, and a compliance officer six months later.

Phase one, define the structure before you file anything

Start with the commercial story. An offshore company works like a legal container. If the container is labelled vaguely, every later reviewer has to guess what belongs inside.

That is why the first stage is less about forms and more about alignment. Your company name, activity wording, shareholder setup, and jurisdiction should all point to the same business purpose. If you say the company will hold investments, your documents should read like a holding structure. If it will manage overseas trading relationships, your profile should show where counterparties, income, and decision-making sit.

At this stage, you usually confirm:

- Company name that fits the registrar’s naming rules

- Shareholder and director details

- Activity description, such as holding assets, investment, or non-UAE trade

- Jurisdiction choice, usually RAK ICC or JAFZA

- Registered agent support, because offshore entities are typically incorporated through approved agents

For a practical view of what local execution usually involves, offshore company formation in Dubai gives a useful overview of the steps, documents, and agent role.

Phase two, build a file that can survive scrutiny

This is the part many short guides rush through. The registrar is checking identity and purpose. Later, the bank will examine the same file with a different question in mind. Can this company be trusted as a real, explainable business?

A weak KYC pack slows everything down. A clear one saves time twice. First at incorporation, then again when you apply for banking or need to support a future Tax Residency Certificate strategy.

Typical documents include:

- Passport copies for shareholders and directors

- Proof of residential address, such as a recent utility bill or bank statement

- Business profile or short business plan explaining what the company will do

- Corporate documents for any corporate shareholder

- Source of funds and source of wealth explanation if requested

- Group structure chart where ownership is layered across several entities

The practical test is simple. Could an independent reviewer understand who owns the company, what money will flow through it, and why the structure exists?

Bookkeeping preparation belongs here too, not after incorporation. Even a pure holding company should decide early how it will store invoices, resolutions, and transaction records. For founders who want a lightweight system from the start, Senki's recommended bookkeeping tools can help you compare options for basic recordkeeping discipline.

Phase three, submit, review, and answer follow-up questions

Once the file is lodged through the registered agent, the authority reviews the application and may ask for clarification. That is normal. It does not always signal a problem. It often means the reviewer wants sharper wording on the activity, clearer ownership evidence, or cleaner address documents.

This stage moves faster when the structure is coherent. It slows down when one part of the file contradicts another, such as a trading activity paired with no explanation of markets, counterparties, or transaction flow.

Investors often underestimate how much later outcomes depend on these early answers. Banks and tax advisers tend to revisit the same themes: beneficial ownership, business rationale, expected turnover, and proof that the company is being used as described.

Phase four, receive the company documents and organise the post-setup file

After approval, the authority issues the incorporation documents. These usually include:

- Certificate of incorporation

- Memorandum and Articles

- Register details

- Share certificates

- Registered office confirmation

Treat this pack as the foundation, not the finish line.

You will use these documents repeatedly for bank applications, compliance reviews, contract onboarding, and any later attempt to show substance or management evidence for tax purposes in 2026. The companies that handle this well keep one organised file with signed resolutions, ownership records, business descriptions, and transaction support ready from the start. That preparation is what separates a company that merely exists on paper from one that can function in practice.

Navigating Compliance and Legal Requirements

A uae offshore company is not a set-and-forget structure. Once incorporated, it enters a compliance environment that is much stricter and more internationally aligned than many investors assume.

The compliance checklist that matters

The first layer is ownership transparency. Offshore companies need accurate beneficial ownership records and must keep corporate records organised and current.

The second layer is tax compliance. Under the UAE tax framework, VAT registration is only mandatory if taxable supplies within the UAE exceed AED 375,000, which is rare for offshore companies because local trade is restricted. ESR compliance is now integrated into the corporate tax return, and larger entities must maintain Transfer Pricing documentation if related-party transactions exceed AED 40 million, according to Links International’s guide to UAE tax compliance.

What that means in practice

The authorities want evidence, not assumptions. If your offshore company claims foreign-sourced income and no UAE economic nexus, your records should support that position.

That usually means keeping:

- Accounting records and supporting invoices

- Contracts showing where counterparties are located

- Board records and ownership registers

- KYC files for shareholders and relevant counterparties where needed

Good bookkeeping is not cosmetic here. It’s defensive infrastructure. If you’re choosing systems for a lean finance stack, Senki's recommended bookkeeping tools are a helpful starting point for understanding what organised record-keeping should look like in a modern business.

The companies that stay comfortable in offshore structures are usually the ones with boringly good records.

The risk of weak compliance

Weak documentation creates two problems. First, regulators may question whether the company still qualifies for its intended tax treatment. Second, banks may see the same weaknesses and decide the client profile is too difficult.

That’s why offshore compliance isn’t just about filing deadlines. It’s about building a paper trail that makes the company intelligible to authorities, auditors, banks, and foreign counterparties.

Beyond Registration Banking and Tax Residency Realities

Many glossy offshore guides prove unhelpful. They describe incorporation accurately, then skip the two issues that often decide whether the structure is usable. Banking and Tax Residency Certificates.

Banking is possible, but it isn’t automatic

Many founders assume that once the offshore company exists, a bank account is just an admin task. It isn’t.

Regional consultancy reporting cited by RSN Finance notes that UAE banks now reject an estimated 40% to 60% of offshore company applications because of heightened AML scrutiny. The same source says that professional introductions can reduce delays from 4 to 6 weeks down to 1 to 2 weeks and improve approval chances when the file is properly prepared, according to RSN Finance on offshore company registration in Dubai.

Banks usually focus on questions like these:

- What does the company do?

- Where does the money come from?

- Who are the ultimate owners?

- Why was an offshore structure chosen?

- Can the client show contracts, invoices, or a credible business plan?

A weak answer to any one of those can stall the account.

If banking is part of your decision from day one, it helps to evaluate setup and account strategy together through resources on opening an offshore company and bank account, because the bank file should influence how the company is presented from the start.

TRC expectations need realism

The second reality is the Tax Residency Certificate, or TRC. Many investors want one because they hope it will support treaty claims or strengthen their home-country tax position.

This area is often oversimplified. The guidance in your brief is clear that offshore entities may be able to apply under updated rules, but outcomes are limited without real UAE substance. In practical terms, investors shouldn’t assume an offshore company will automatically deliver treaty benefits just because it is registered in the UAE.

That’s especially important for internationally mobile investors buying foreign assets from Dubai. For example, someone structuring overseas holdings should also understand the tax rules in the destination country, not just the UAE side. If Australian real estate is part of your plan, this expat guide to Australian property investment is useful because it highlights how cross-border ownership decisions can trigger obligations outside the UAE.

A registered company and a tax-resident company are not always the same thing.

What sensible founders do differently

They don’t ask, “How fast can I register?”

They ask, “Will this company bank cleanly, and will the structure stand up when another tax authority looks at it?”

That question produces better decisions.

Common Use Cases and How Smart Classic Can Help

The most effective offshore structures are usually the simplest in purpose.

Three common use cases

Holding investments is one of the strongest examples. An investor may want one UAE-based legal entity to hold shares in several foreign businesses, creating cleaner ownership and easier transfer planning.

Asset protection is another. A separate legal company can hold specific assets so they are not mixed with an operating business that signs contracts, hires staff, or takes commercial risk.

International trading or invoicing can also work when the commercial relationships sit outside the UAE and the documentation supports that fact.

Where advisory support matters

What trips people up isn’t usually the legal concept. It’s the handoff points. Jurisdiction choice, KYC quality, banking presentation, tax analysis, and annual records all affect one another.

In that context, Smart Classic Business Hub is one practical option for handling offshore registration, related PRO support, VAT-compliant accounting, and TRC-related services within a broader UAE setup process. For many founders, the value of that kind of consultancy is not that it “forms a company”. It’s that it helps keep the structure coherent after formation.

A good advisor should help you answer questions like:

- Is offshore even the right structure for your commercial reality?

- Should you use RAK ICC or JAFZA for your actual objective?

- What documents will your bank want to see before you apply?

- What accounting trail should exist from day one?

Those are the questions that keep an offshore company usable.

If your goal is to get a certificate quickly, many providers can do that. If your goal is to build a structure that survives compliance checks, works with banking, and fits cross-border tax reality, you need more disciplined planning.

If you're evaluating whether a uae offshore company fits your business, investment, or holding strategy, Smart Classic Business Hub can assist with offshore registration, compliance support, banking preparation, accounting, and related UAE business services so the structure is assessed in practical terms, not just sold as a template.